Energising Britain

We believe investing in our people goes hand-in-hand with enabling the green energy transformation and positive future growth.

Information about our business, partnerships and campaigns, as well as photos, graphics and multimedia assets for journalists, and educational materials for schools.

Information about our business, partnerships and campaigns, as well as photos, graphics and multimedia assets for journalists, and educational materials for schools.

We’re committed to enabling a zero carbon, lower cost energy future through engineering, technology and innovation.

We’re building for a sustainable future in how we source our biomass, generate energy, remove carbon dioxide and function as a business.

Read our carbon capture, sustainable bioenergy and power generation stories, as well as thinking from Drax’s leaders and business updates.

RNS Number : 1079F

Drax Group PLC

Andy Skelton

Andy has been CFO at Fidessa Group plc, a UK listed global software and services business, since October 2015. He was previously Deputy CFO at CSR plc, before its acquisition in 2015 by Qualcomm Incorporated. Prior to joining CSR Andy held senior finance positions at Ericsson and Marconi, including two years as CFO of Ericsson Nikola Tesla. He has a BA in Accounting and Finance from Heriot Watt University and qualified as a chartered accountant in 1994.

Den Jones will remain with the Company until June 2019 to support the acquisition and integration of Scottish Power’s portfolio of pumped storage, hydro and gas-fired generation from Iberdrola. The acquisition is conditional upon the approval by Drax’s shareholders and clearance by UK Competition and Markets Authority.

“The Directors are delighted to welcome Andy to the Board of Drax. He brings a wealth of experience and skills, and will be a strong addition to the Drax team. I also extend the directors’ thanks to Den Jones who has done an excellent job as Interim CFO.”

There are no further matters which are required to be disclosed under Rule 9.6.13R of the Listing Rules of the Financial Services Authority.

Drax Investor Relations: Mark Strafford

Drax External Communications: Matt Willey

Website: www.drax.com/uk

Mr Skelton’s remuneration will be in accordance with the Company’s remuneration policy and at an annual base salary of £355,000. No payments in respect of compensation for benefits lost on resignation from his previous employment will be made.

On 3 August 2018, an offer from ION Capital UK for the entire share capital of Fidessa was declared unconditional in all respects.

END

Will Gardiner, CEO, Drax Group

“I am excited by the opportunity to acquire this unique and complementary portfolio of flexible, low-carbon and renewable generation assets. It’s a critical time in the UK power sector. As the system transitions towards renewable technologies, the demand for flexible, secure energy sources is set to grow. We believe there is a compelling logic in our move to add further flexible sources of power to our offering, accelerating our strategic vision to deliver a lower-carbon, lower-cost energy future for the UK.

“This acquisition makes great financial and strategic sense, delivering material value to our shareholders through long-term earnings and attractive returns.

“We are combining our existing operational expertise with the specialist technical skills of our new colleagues and I am looking forward to what we can achieve together.”

The Portfolio consists of Cruachan pumped storage hydro (440MW), run-of-river hydro locations at Galloway and Lanark (126MW), four CCGT(2) stations: Damhead Creek (805MW), Rye House (715MW), Shoreham (420MW) and Blackburn Mill (60MW), and a biomass-from-waste facility (Daldowie).

The Portfolio is expected, based on recent power and commodity prices, to generate EBITDA in a range of £90-110 million, from gross profits of £155 million to £175 million, of which around two thirds is expected to come from non-commodity market sources, including system support services, capacity payments, Daldowie and ROCs(3). Pumped storage and hydro activities represent a significant proportion of the earnings associated with the portfolio. Further information is set out in Appendix 2 of this Announcement.

Capital expenditure in 2019 is expected to be in the region of £30-35 million.

For the year ended 31 December 2017, the Portfolio generated EBITDA of £36 million(4). EBITDA in 2019 is expected to be higher due to incremental contracted capacity payments (c.£42 million), no availability restrictions (Cruachan’s access to the UK grid during 2017 was limited by network transformer works) (c.£8 million), a lower level of corporate cost charged to the portfolio (c.£9 million) and revenues from system support services and current power prices. Gross assets as at 31 December 2017 were £419 million(5).

The Acquisition represents an attractive opportunity to create significant value for shareholders and is expected to deliver returns significantly in excess of the Group’s WACC and to be highly accretive to underlying earnings in 2019.

The Acquisition strengthens the Group’s ability to pay a growing and sustainable dividend. Drax remains committed to its capital allocation policy and to its current £50 million share buy-back programme, with £32 million of shares purchased to date.

Drax has entered into a fully underwritten £725 million secured acquisition bridge facility agreement to finance the Acquisition. Assuming performance in line with current expectations, net debt to EBITDA is expected to fall to Drax’s long-term target of around 2x by the end of 2019.

Drax expects its credit rating agencies to view the Acquisition as contributing to a reduced risk profile for the Group and to reaffirm their ratings.

The Acquisition is expected to complete on 31 December 2018 and is conditional upon the approval of the Acquisition by Drax’s shareholders and clearance by UK Competition and Markets Authority (the “CMA”). A summary of the terms of the Acquisition agreement (the “Acquisition Agreement”) is set out in Appendix 1 to this announcement.

Since publishing its half year results on 24 July 2018 Drax has commenced operation of a fourth biomass unit at Drax Power Station, which is performing in line with plan, and availability across biomass units has been good.

Biomass storage domes at Drax Power Station

Taking these factors into account, alongside a strong 2018 hedged position and assuming good operational availability for the remainder of the year, Drax’s EBITDA expectations for the full year remain unchanged, with net debt to EBITDA now expected to be around 1.5x for the full year, excluding the impact of the Acquisition.

Biomass generation is now fully contracted for 2019.

| 2018 | 2019 | 2020 | |

|---|---|---|---|

| Power sales (TWh) comprising: | 18.6 | 11.5 | 5.7 |

| TWh including expected CfD sales | 18.6 | 15.6 | 11.2 |

| – Fixed price power sales (TWh) | 18.6 | 11.0 | 5.1 |

| At an average achieved price (per MWh) | at £46.8 | at £50.4 | at £48.3 |

| – Gas hedges (TWh) | - | 0.5 | 0.6 |

| At an achieved price per therm | - | 43.5p | 47.4p |

Drax intends to hedge up to 1TWh of the commodity exposures in the Portfolio ahead of completion in line with the Group’s existing hedging strategy.

In light of the Acquisition and the expected timing of the general meeting to approve it, Drax will postpone the planned Capital Markets Day on 13 November 2018.

Drax expects to announce its full year results for the year ending 31 December 2018 on 26 February 2019.

Enquiries:

Drax Investor Relations: Mark Strafford

+44 (0) 1757 612 491

+44 (0) 7730 763949

Media:

Drax External Communications:

Matt Willey

+44 (0) 7711 376087

Ali Lewis

+44 (0) 77126 70888

J.P. Morgan Cazenove (Financial Adviser and Joint Corporate Broker):

+44 (0) 207 742 6000

Robert Constant

Jeanette Smits van Oyen

Carsten Woehrn

Royal Bank of Canada (Joint Corporate Broker):

+44 (0) 20 7653 4000

James Agnew

Jonathan Hardy

Management will host a presentation for analysts and media at 9:00am (UK Time), Tuesday 16 October 2018, at FTI Consulting, 200 Aldersgate, Aldersgate Street, London EC1A 4HD.

Would anyone wishing to attend please confirm by e-mailing [email protected] or calling Christopher Laing at FTI Consulting on +44 (0) 20 3727 1355 / 07809 234 126.

The meeting can also be accessed remotely via a live webcast, as detailed below. After the meeting, the webcast will be made available and access details of this recording are also set out below.

A copy of the presentation will be made available from 9am (UK time) on Tuesday 16 October 2018 for download at: www.drax.com/uk>>investors>>results-reports-agm>> #investor-relations-presentations or use the link below.

| Event Title: | Drax Group plc: Acquisition of flexible, low-carbon and renewable UK power generation from Iberdrola |

| Event Date: | Tuesday 16 October 2018 |

| Event Time | 9:00am (UK time) |

| Webcast Live Event Link | https://www.drax.com/uk/investors/16-oct-2018-webcast |

| 020 3059 5868 (UK) | |

| +44 20 3059 5868 (from all other locations) | |

| Start Date: | Tuesday 16 October 2018 |

| Delete Date: | Monday 14 October 2019 |

| Archive Link: | https://www.drax.com/uk/investors/16-oct-2018-webcast |

For further information please contact Christopher Laing on +44 (0) 20 3727 1355 / 07809 234 126.

Website: www.drax.com/uk

Drax Smart Generation Holdco Limited (“Drax Smart Generation”), a wholly owned subsidiary of Drax, has entered into the Acquisition Agreement with Scottish Power Generation Holdings Limited (the “Seller”), a wholly-owned subsidiary of Iberdrola S.A., for the acquisition of ScottishPower Generation Limited (“SPGEN”), for £702 million in cash.

The Portfolio principally consists of 2.6GW of assets which are highly complementary to Drax’s existing generation portfolio and play an important role in the UK energy system. The assets include:

440MW of large-scale storage and flexible low-carbon generation situated in Argyll and Bute, Scotland.

Cruachan provides a wide range of system support services to the UK energy market, in addition to providing merchant power generation. Cruachan has £35 million of contracted capacity payments for the period 2019 to 2022.

Cruachan, which provides over 35% of the UK’s pumped storage by volume, can provide long-duration storage with the ability to achieve full load in 30 seconds, which it can maintain for over 16 hours, making it a strategically important asset remunerated by a broad range of non-commodity based revenues.

126MW of stable and reliable renewable generation situated in South-west Scotland.

Both locations benefit from index-linked ROC revenues extending to 2027 and Galloway, in addition to renewable power generation, operates a reservoir and dam system providing storage capabilities and opportunities for peaking generation and system support services. It also has £4 million of contracted capacity payments for the period 2019 to 2022.

1,940MW of capacity at Damhead Creek (805MW), Rye House (715MW) and Shoreham (420MW) all strategically located in South-east England.

These assets provide baseload and/or peak power generation in addition to other system support services and benefit from attractive grid access income associated with their location. The three plants have contracted capacity payments of £127 million for the period 2019 to 2022.

Damhead Creek also benefits from an attractive option for the development of a second CCGT asset, Damhead Creek II, which provides additional gas generation optionality alongside Drax’s existing coal-to-gas repowering and OCGT(6) projects. All options could be developed subject to an appropriate level of support. Damhead Creek II is eligible for the 2019 capacity market auction along with two of Drax’s existing OCGT projects.

The portfolio also includes a small CCGT in Blackburn (60MW) and a 50K tonne biomass-from-waste facility in Daldowie, which benefits from a firm offtake contract agreement with Scottish Water until 2026.

The UK has a target to reduce carbon emissions by 80% by 2050. The transition to a low-carbon economy requires decarbonisation of heating, transport and generation. This will in turn require additional low-carbon sources of generation to be developed in the UK. As much as 85%(7) of future generation could come from renewables – predominantly wind and solar. This will lead, at times, to high levels of power price volatility and increasing demand for system support services. Managing an energy system with these characteristics will only be possible if it is supported by the right mix of flexible assets to manage volatility, balance the system and provide crucial non-generation services which a stable energy system requires.

The Acquisition is closely aligned with this structural need and the operation of Drax’s existing biomass and gas options which provide the flexibility required to enable higher levels of intermittent renewable generation.

The Acquisition is in line with these system needs and when combined with Drax’s existing flexible, biomass generation and gas options offers the Group increased exposure to the growing need for system support and power price volatility.

The Acquisition is closely aligned with this structural need and the operation of Drax’s existing biomass and gas options which provide the flexibility required to enable higher levels of intermittent renewable generation.

The Acquisition is in line with these system needs and when combined with Drax’s existing flexible, biomass generation and gas options offers the Group increased exposure to the growing need for system support and power price volatility.

Two thirds of the gross profits of the Portfolio is expected to come from non-commodity market sources, including system support services, capacity payments, Daldowie and ROCs, in addition to power generation activities. Due to the expected growing demand for these assets and the contract-based nature of many of these services Drax expects to improve long-term earnings visibility through structured non-commodity earnings streams, whilst retaining significant opportunity to benefit from power price volatility.

When combined with renewable earnings and system support from existing biomass generation, the Acquisition is expected to lead to an increase in the quality of earnings.

Wood pellet storage domes at Drax Power Station, Selby, North Yorkshire

The Acquisition accelerates Drax’s development from a single-site generation business into a multi-site, multi-technology operator.

With the acquisition of this portfolio, a fall in gas prices could be mitigated by an increase in gas-fired generation reflecting the relative dispatch economics of the different technologies.

Drax expects to benefit from the management of generation across a broader asset base, leveraging the Group’s expertise in the operation, trading and optimisation of large rotating mass generation.

Drax believes that the team operating the Portfolio has a strong engineering culture which is closely aligned with the Drax model and will enhance the Group’s strong capabilities across engineering disciplines.

Around 260 operational roles will transfer to Drax as part of the Acquisition, complementing and reinforcing Drax’s existing engineering and operational capabilities.

Drax has entered into a fully underwritten £725 million secured acquisition bridge facility to finance the Acquisition, with a term of 12 months from the first date of utilisation of the facility (with a seven-month extension option) and interest payable at a rate of LIBOR plus the applicable margin (the “Acquisition Facility Agreement”). The facility is competitively priced and below Drax’s current cost of debt.

Drax will consider its options for its long-term financing strategy in 2019.

Assuming performance in line with current expectations, net debt to EBITDA is expected to return to Drax’s long-term target of around 2x by the end of 2019.

Drax expects credit rating agencies to view the Acquisition as supportive of the rating and contributing to a reduced risk profile for the Group.

Drax is progressing a detailed integration plan to combine the Acquisition as part of the existing Power Generation business.

The transaction is subject to shareholder approval. A combined Shareholder Circular and notice of General Meeting will be posted as soon as practicable.

The transaction is expected to complete on 31 December 2018.

(1) EBITDA is defined as earnings before interest, tax, depreciation, amortisation and material one-off items that do not reflect the underlying trading performance of the business. 2019 EBITDA is stated before any allocation of Group overheads.

(2) Combined Cycle Gas Turbine.

(3) Renewable Obligation Certificates.

(4) 2017 EBITDA is unaudited and based on the audited financial statements of Scottish Power Generation Limited and SMW Limited, adjusted to exclude results of assets that do not form part of the Portfolio and restated in accordance with Drax accounting policies.

(5) On an unaudited historic cost basis, inclusive of an historic write down and other changes arising from the application of Drax’s accounting policies, and incorporating intercompany debtors which will be replaced by Drax going forward.

(6) Open Cycle Gas Turbines.

(7) Intergovernmental Panel on Climate Change. In a 1.5c pathway renewables are projected to be 70-85% of global electricity in 2050.

The contents of this announcement have been prepared by and are the sole responsibility of Drax Group plc (the “Company”).

J.P. Morgan Limited (which conducts its UK investment banking business as J.P. Morgan Cazenove) (“J.P. Morgan Cazenove”) and RBC Europe Limited (“RBC”), which are both authorised by the Prudential Regulation Authority (the “PRA”) and regulated in the United Kingdom by the FCA and the PRA, are each acting exclusively for the Company and for no one else in connection with the Acquisition, the content of this announcement and other matters described in this announcement and will not regard any other person as their respective clients in relation to the Acquisition, the content of this announcement and other matters described in this announcement and will not be responsible to anyone other than the Company for providing the protections afforded to their respective clients nor for providing advice to any other person in relation to the Acquisition, the content of this announcement or any other matters referred to in this announcement.

J.P. Morgan Cazenove, RBC and their respective affiliates do not accept any responsibility or liability whatsoever and make no representations or warranties, express or implied, in relation to the contents of this announcement, including its accuracy, fairness, sufficient, completeness or verification or for any other statement made or purported to be made by it, or on its behalf, in connection with the Acquisition and nothing in this announcement is, or shall be relied upon as, a promise or representation in this respect, whether as to the past or the future. Each of J.P. Morgan Cazenove, RBC and their respective affiliates accordingly disclaims to the fullest extent permitted by law all and any responsibility and liability whether arising in tort, contract or otherwise which it might otherwise be found to have in respect of this announcement or any such statement.

Certain statements in this announcement may be forward-looking. Any forward-looking statements reflect the Company’s current view with respect to future events and are subject to risks relating to future events and other risks, uncertainties and assumptions relating to the Company and its group’s, the Portfolio’s and/or, following completion, the enlarged group’s business, results of operations, financial position, liquidity, prospects, growth, strategies, integration of the business organisations and achievement of anticipated combination benefits in a timely manner. Forward-looking statements speak only as of the date they are made. Although the Company believes that the expectations reflected in these forward looking statements are reasonable, it can give no assurance or guarantee that these expectations will prove to have been correct. Because these statements involve risks and uncertainties, actual results may differ materially from those expressed or implied by these forward looking statements.

Each of the Company, J.P. Morgan Cazenove, RBC and their respective affiliates expressly disclaim any obligation or undertaking to supplement, amend, update, review or revise any of the forward looking statements made herein, except as required by law.

You are advised to read this announcement and any circular (if and when published) in their entirety for a further discussion of the factors that could affect the Company and its group, the Portfolio and/or, following completion, the enlarged group’s future performance. In light of these risks, uncertainties and assumptions, the events described in the forward-looking statements in this announcement may not occur.

Neither the content of the Company’s website (or any other website) nor any website accessible by hyperlinks on the Company’s website (or any other website) is incorporated in, or forms part of, this announcement.

The following is a summary of the principal terms of the Acquisition Agreement.

The Acquisition Agreement was entered into on 16 October 2018 between Drax Smart Generation and the Seller. Pursuant to the Acquisition Agreement, the Seller has agreed to sell, and Drax Smart Generation has agreed to acquire, the whole of the issued share capital of SPGEN for £702 million, subject to certain customary adjustments in respect of cash, debt and working capital.

Drax Group Holdings Limited has agreed to guarantee the payment obligations of Drax Smart Generation under the Acquisition Agreement. Scottish Power UK plc has agreed to guarantee the payment obligations of the Seller under the Acquisition Agreement.

The Acquisition is conditional on:

Completion is currently expected to occur on 31 December 2018 assuming that the conditions are satisfied by that date.

Drax Smart Generation has the right to terminate the Acquisition Agreement upon the occurrence of a material reduction in available generation capacity at any of the Cruachan, Galloway and Lanark or Damhead Creek facilities which subsists, or is reasonably likely to subsist, for a continuous period of three months. The right of Drax Smart Generation to terminate in these circumstances is subject to the Seller’s right to defer Completion if the relevant material reduction in available generation capacity can be resolved by end of the month following the anticipated date of Completion.

A break fee of £14.6 million (equal to 1% of Drax’s market capitalisation at close of business on the day before announcement) is payable if the Shareholder Approval Condition is not met, save where this is as a result of a material reduction in available generation capacity as described above.

The Seller has given certain customary covenants in relation to the period between signing of the Acquisition Agreement and completion, including to carry on the SPGEN business in the ordinary and usual course. The Seller will carry out certain reorganisation steps prior to completion.

Drax Smart Generation has agreed to assume the accrued defined benefit pension liabilities associated with the employees of the SPGEN group as at the date of signing the Acquisition Agreement. Following Completion, the SPGEN group will continue to participate in the Seller’s group defined benefit pension scheme, known as the ScottishPower Pension Scheme (“SPPS”) for an interim period of 12 months unless agreed otherwise (the “Interim Period”) while a new pension scheme is set up by the SPGEN group for the benefit of its employees (the “New Scheme”).

At the end of the Interim Period, the SPPS trustees will be requested to transfer from the SPPS to the New Scheme an amount of liabilities (and corresponding share of assets) agreed between the Seller and Drax Smart Generation (or failing agreement, an amount determined by an independent actuary) in respect of the past service liabilities relating to the SPGEN group employees. If the amount of assets transferred to the New Scheme does not match the amount agreed (or independently determined), there will be a true-up between the Seller and Drax Smart Generation.

If the SPPS trustees do not make any transfer to the New Scheme within the period of 18 months following the Interim Period (unless this was caused by a breach of the Acquisition Agreement by the Seller), Drax Smart Generation has agreed to pay £16 million (plus base rate interest) to the Seller as compensation for the SPPS liabilities not taken on by the New Scheme.

The Seller has provided customary warranties in the Acquisition Agreement. The Seller also has provided Drax Smart Generation with indemnities in respect of certain specific matters, including for any losses associated with the reorganisation referred to above. A customary tax covenant is also provided in the Acquisition Agreement.

The Seller and SPGEN will enter into a transitional services agreement effective at Completion. The specific nature, terms and charges relating to the services to be provided will be agreed between the Seller and SPGEN prior to Completion. The Seller will also provide assistance in relation to the extraction and separation of the SPGEN group from the systems of the Seller and integration of the SPGEN group onto the systems of the Drax Group.

The Portfolio is expected, based on recent power and commodity prices, to generate EBITDA in a range of £90-110 million (“Profit Forecast”), and gross profits of £155 million to £175 million, of which around two thirds is expected to come from non-commodity market sources, including system support services, capacity payments, Daldowie and ROCs. Pumped storage and hydro activities represent a significant proportion of the earnings associated with the portfolio.

For the purpose of the Profit Forecast, EBITDA is stated before any allocation of Group overheads (as these will be an allocation of the existing Drax Group cost base which is not expected to increase as a result of the acquisition of the Portfolio).

The Profit Forecast has been compiled on the basis of the assumptions stated below, and on the basis of the accounting policies of the Drax Group adopted in its financial statements for the year ended 31 December 2017. Subsequent accounting policy changes include the application of IFRS15 and IFRS9 which are not initially expected to change the EBITDA results of the Portfolio. It also does not reflect the impact of IFRS16 which would apply in respect of the 2019 Annual Report and Accounts.

The Profit Forecast has been prepared with reference to:

The Profit Forecast is a best estimate of the EBITDA that the Portfolio will generate for a future period of a year in respect of assets and operations that are not yet under the control of Drax. Accordingly the degree of uncertainty relating to the assumptions underpinning the Profit Forecast is inherently greater than would be the case for a profit forecast based on assets and operation under the control of Drax and/or which covered a shorter future period. The Profit Forecast has been prepared as at today and will be updated in the shareholder circular.

The forecast cost base reflects the expectations of the Drax Directors of the operating regime of the Portfolio under Drax’s ownership and the central support it will require.

The Profit Forecast has been prepared on the basis of the following principal assumptions:

END

17 September 2018

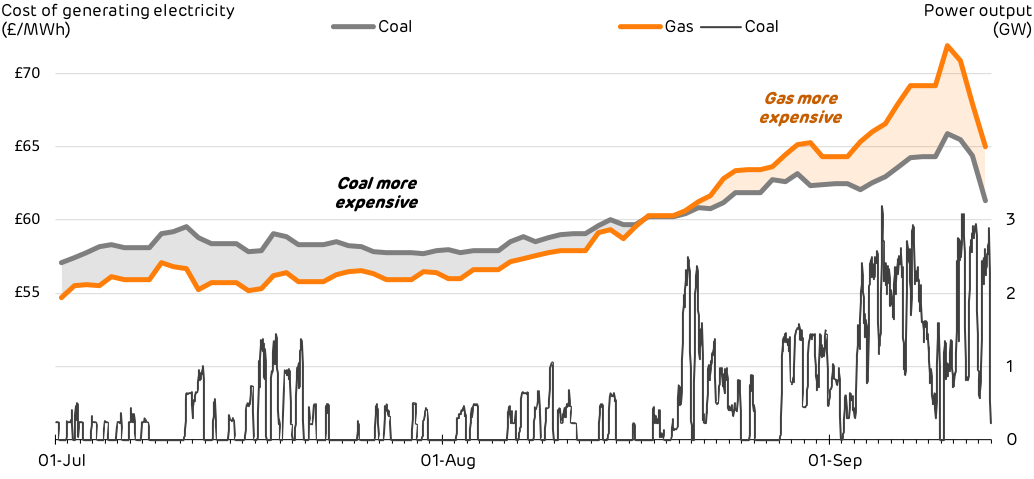

10-year high gas prices1 have prompted a resurgence in coal-fired power across Britain – and with it a 15% increase in carbon emissions from electricity generation.

If coal-fired electricity remains cheaper than gas-fired (as analysts predict), we could see the first year-on-year rise in carbon emissions from Britain’s power sector in six years. This highlights the importance of retaining a strong carbon price if we are to ensure the successful decarbonisation of the power system is not reversed.

After dropping to a historic low of just 0.2 GW during June and July, Britain’s coal power generation doubled in August, and has shot up to 2 GW during the first week of September. The last time coal output was this high was during the Beast from the East, when temperatures plummeted in March.

With these coal power stations running instead of more efficient gas plants, Britain is producing an extra 1,000 tonnes of carbon dioxide (CO2) every hour.2 Carbon emissions from electricity generation are up 15% as a result. These coal plants are not running solely because they are needed to meet peak demand, but because gas prices have risen sharply and carbon prices have not kept up, making coal power stations more economic to run than gas-fired ones.

It became cheaper to generate power from coal than from gas (see thick lines, chart below) in late August. Even though carbon prices now double the cost of generating electricity from coal,3 coal plants are consistently “in the money” at the moment, meaning they can generate power profitably all day and night.

Estimated cost of generating electricity from coal and gas in Quarter 3 (thick lines), and the output from coal power stations in Britain (thin line)

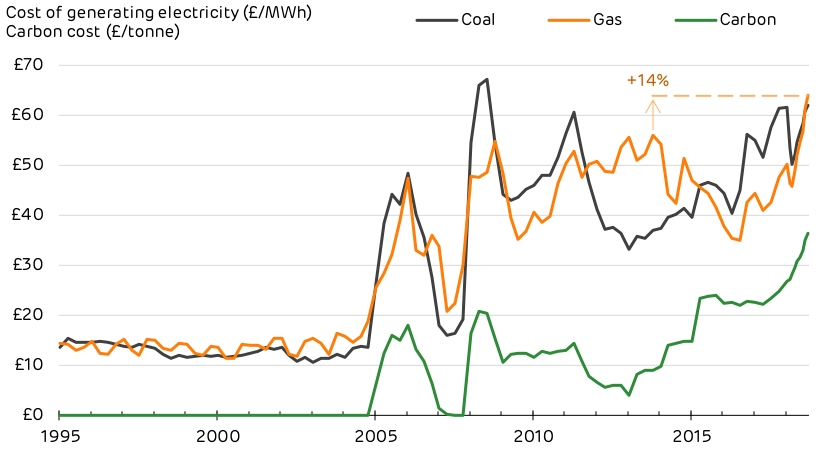

The cost of emitting CO2 has increased sharply, up 45% so far this year due to the ongoing rally in European Emissions Trading Scheme (EU ETS) prices. Rising carbon prices should make gas more economical to burn as it emits less than half the CO2 of coal.

However, wholesale gas prices have also risen 40% since the start of the year, as supplies and storage are squeezed in the run up to winter. Gas prices are at a ten-year high, currently 14% above their previous quarterly-average peak back in 2013 (see chart below). These rising costs are feeding through into wholesale power prices, which have risen by a third over the past year to hit £60/MWh.

The estimated cost of generating electricity from fossil fuels over the last 20 years, along with the cost of emitting CO2.

Britain’s carbon price strengthened dramatically through 2014–15 due to the government implementing a Carbon Price Support scheme. This caused gas to become competitive against coal for power generation, leading to carbon emissions from the power sector halving. Unless Britain’s carbon price can once again make up the gap between coal and gas prices, we risk rolling back some of the world-leading gains made on cleaning up our electricity system.

The Committee on Climate Change has made it clear that power is the only sector that is pulling its weight when it comes to decarbonising the UK. Clean electricity could power low-carbon vehicles and heating, but this opportunity will be wasted if the electricity comes from high-carbon coal.

So what can be done? The sharp rise in gas prices hints at a lack of flexibility in the energy system. Britain came uncomfortably close to gas shortages in March, in part due to the closure of the country’s largest gas storage site. With nearly half of the electricity generated in Britain coming from gas, plus five-sixths of household heat, diversifying into other – cleaner – energy sources would help insulate consumers and businesses from price spikes.

No one country has the power to determine international fuel prices. Several factors have come together to push up gas prices, including a lack of transmission capacity, depleted stores of gas after the long hot summer and a lack of wind power increased output from gas-fired stations. Suppliers which don’t wish to be caught short after the Beast from the East, are also stocking up on gas.

Any knee-jerk reaction to try and lower the cost of electricity (for example, slashing the cost of carbon emissions) may only have a short-term impact, and could easily lead to longer-term damage (such as the resurgence of coal) which would require further interventions in the future.

Britain does have control over its carbon price. Its power stations and industry currently pay the Emissions Trading System price (determined on the Europe-wide market) which has fluctuated wildly over the past week between €25 (£22) and €19 (£17) per tonne, plus £18 per tonne in Carbon Price Support which goes to the Treasury. This needs to be maintained or strengthened further to save the power system from backsliding, and to show strong climate leadership on the international stage.

[1] The three-month average cost of generating electricity from gas exceeded £60/MWh for the first time since 2009. Short-term price spikes have been higher than this, such as the first week of March during the Beast from the East.↩

[2] Extra generation from coal reduces the output from gas plants, which are their main competitors, as nuclear, wind and solar already run as much as possible. Calculation based on 1934 MW of coal generation (the average during the first week of September) emitting 937 gCO2 per kWh (1812 tonnes per hour) instead of gas generation which would have emitted 394 gCO2 per kWh (762 tonnes per hour).↩

[3] The coal that must be burnt to produce 1 MWh of electricity now costs around £31, and the CO2 pollution costs an extra £31 on top. For comparison, producing 1 MWh of electricity from gas costs £50 for the fuel and £15 for the CO2.↩

In 2003, the UK’s biggest coal power station took its first steps away from the fossil fuel which defined electricity generation for more than a century. It was in that year that Drax Power Station began co-firing biomass as a renewable alternative to coal.

It symbolised the beginnings of the power station’s ambitious transformation from fossil-fuel stalwart to the country’s largest single-site renewable electricity generator. This plan presented a massive engineering challenge for Drax, with significant amounts of new knowledge quickly needed.

Fifteen years later, three of its generating units now run entirely on compressed wood pellets, a form of biomass, while coal has been relegated to stepping in only to cover spikes in demand and improve system stability.

Now Drax has converted a fourth unit from coal to biomass. This development represents the passing of a two thirds marker for the power station’s coal-free ambitions and adds 600-plus megawatts (MW) of renewable electricity to Great Britain’s national transmission system.

Drax first converted a coal unit to biomass in 2013, with two more following in 2014 and 2016. This put Drax in an interesting position going into a new conversion: on one hand, it is one of the most experienced generators in the world when it comes to dealing with and upgrading to biomass. On the other, it’s still relatively new to the low carbon fuel compared with its dealings with coal.

Adam Nicholson

“We’ve decades of understanding of how to use coal, but we’ve only been operating with biomass since we started the full conversion trials in 2011,” says Adam Nicholson, Section Head for Process Performance at Drax Power. “We’ve got few running hours under our belts with the new fuel versus the hundreds of man years of coal knowledge and operation all around the country.”

When converting a generating unit, the steam turbine and generator itself remain the same. The difference is all in the material being delivered, stored, crushed and blown into the boiler and burned to heat up water and create steam. And because biomass can be a volatile substance – much more so than coal – this process must be a careful one.

Drax could build on the learnings and equipment it had already developed for biomass such as specially built trains and pulverising mills, but storage proved a bigger issue. The giant biomass domes at Drax that make up the EcoStore are advanced technological structures carefully attuned to storing biomass, but for Unit 4, they were off limits.

Instead Drax engineers had to come up with another solution.

Normally wood pellets are brought into Drax by train, unloaded and stored in the biomass domes before travelling through the power station to the mills and then boilers. Unit 4, however, sits in the second half of the station – built 12 years after the first. This slight change in location presented a problem.

“There’s no link from the eco store to Unit 4 at all,” explains Nicholson. “You can’t use the storage domes and that whole infrastructure to get anything to Unit 4.”

Drax engineers set about designing a new conveyor system that could connect the domes to the mills and boiler that powers Unit 4. After weeks of design, the team had a theoretical plan to connect the two locations with one problem: it was entirely uneconomical.

Rail unloading building 1 and storage silos

“If we were building a new plant it would be relatively easy, because you could plan properly and wouldn’t have existing equipment in the way,” says Nicholson.

“We had to plan around it and make use of the pre-existing plant.”

Within that pre-existing plant though were vital pieces of equipment, some of which had laid dormant since Drax stopped fuelling its boilers with a mixture of coal and biomass and opted instead for full unit conversions.

Drax began cofiring across all six units in 2003, using two different materials – a mix of around 5% biomass and 95% coal. A direct injection facility was added in 2005. It involved blowing crushed wood pellets into coal fuel lines from two of the power station’s 60 mills.

Then, the amount of renewable power Drax was able to generate roughly doubled in the summer of 2010 when a 400 MW co-firing facility became operational.

Back to the present day, it’s fortunate for the Unit 4 conversion that the co-firing facility includes its own rail unloading building (RUB 1) and storage silos. They are located much closer to the unit than the bigger RUB 2 and the massive biomass domes.

This solved the problem of storage but moving the required volumes of biomass through the plant without significant transport construction still posed a challenge.

Rail unloading building 1 and storage silos for Unit 4 [left], EcoStore biomass domes for units 1-3 [right]

Andy Koss

For now, Drax’s fifth and sixth generating unit remain coal-powered, but are called upon less frequently. With Great Britain set to go completely coal-free by 2025, there are plans to convert these too, but as part of a system of combined cycle gas turbines and giant batteries rather than biomass powered units.

It’s an opportunity for Drax to again leverage its pre-existing plant and provide the grid with a fast acting-source of lower-carbon electricity. As with converting to biomass, it will pose a complex new engineering challenge – one that will prepare Drax to meet the future needs of grid as it continues to change and demand greater flexibility from generators.

“The speed at which the Unit 4 project has been delivered is testament to the engineering expertise, skill and ingenuity we continue to see at Drax. We’re nimble and innovative enough to meet future challenges,” says Andy Koss, Chief Executive, Drax Power.

“We may look very different in 10 or 20 years’ time, but the ethos of that innovation and agility is something that will persist.”

Repowering the remaining coal plant with gas and up to 200 MW of batteries will sit alongside research into areas such as carbon capture, use and storage (CCuS) that is all geared towards expanding Drax Power beyond a single site generator into a portfolio of flexible power production facilities.

Unit 4’s conversion is more than just a step beyond halfway for the power station’s decarbonisation, but a significant step towards becoming entirely coal-free.

Every summer Great Britain uses less and less coal. This June the fossil fuel’s share of the electricity mix dipped below 1% for the first time ever – for 12 days it dropped all the way to zero.

Spurred on by the beginnings of an uncharacteristically dry, hot summer and a jump in solar generation, the possibility of the country going entirely coal-free for a full summer now looks more achievable than ever in modern times.

This is one of the key findings from Electric Insights, a quarterly report commissioned by Drax and written, independently, by researchers from Imperial College London. It found that across Q2 2018, there were as many coal-free hours as in the whole of 2016 and 2017 combined.

And while the report’s findings are hugely positive, they also hint at where development is still needed. What else does the performance of this quarter tell us about what we can expect in the power sector – in Great Britain and around the world?

Great Britain has reduced its coal-fired power generation by four-fifths over the last five years. Last quarter the country’s coal fleet ran at just 3% of its 12.9 gigawatt (GW) capacity. Coal capacity is now lower than the capacity of solar PV panels (13.1 GW) installed nationwide, with the most recent decline resulting from Drax’s conversion of a fourth unit from coal to biomass.

When coal generation was running, it primarily provided system balancing services overnight in May and June rather than baseload electricity. However, this positive trend is not seen around the world.

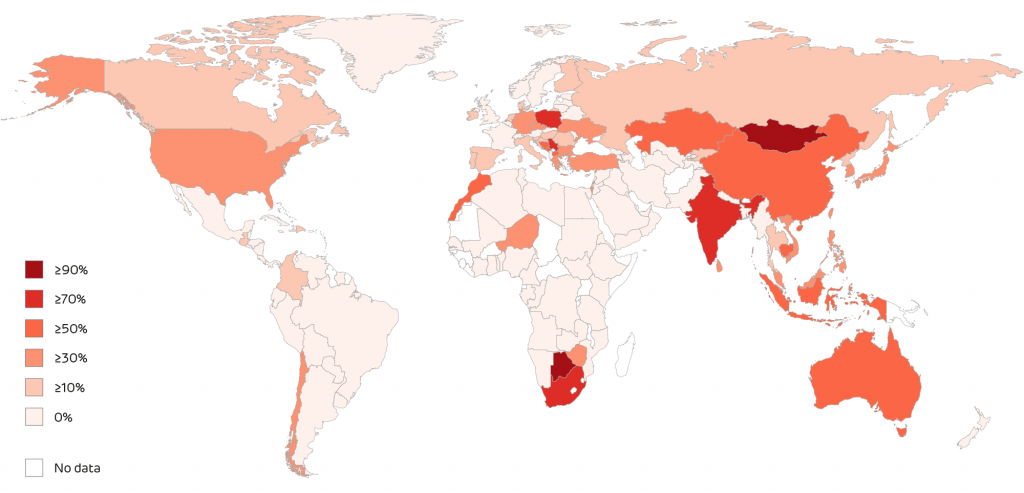

The share of coal in national power systems during 2017

Globally, coal still provides 38% of the world’s electricity – the same amount it did 30 years ago. This comes despite efforts in Europe and North America to move away from coal, and growing investment into renewable generation and technologies.

Overall, Europe’s coal generation dropped from 39% to 22% over the last 30 years, despite some countries – such as Poland and Serbia – still drawing significant generation from the fossil fuel. The US has also reduced its coal generation from 57% to 31% over the past 30 years, as natural gas proves more economical, even in an era of pro-coal policies.

However, in the Middle East and Africa (which draw significant generation from their oil and gas reserves) and South America (where coal accounts for less than 3% of generation), total coal generation is growing. In fact, globally, only seven countries use less coal today than 30 years ago: Germany, Poland, Spain, Ukraine, the US, Great Britain and Canada.

Electric Insights attributes part of this global growth to the continued increase in demand for electricity, particularly in Asia. China, South Korea and Indonesia collectively burn 10 times more coal than they did 30 years ago. India’s coal habit has also increased over the past decade to account for 76% of its electricity generation, while Japan’s usage has grown from 15% to 34% in the same period.

As well as the stresses created by growing demand, this highlights a global disparity in the approach to decarbonising electricity systems, and a need for longer-term, environmentally and socially-conscious market-based initiatives that encourage meaningful movement to lower-carbon electricity sources, such as the UK and Canada’s Powering Past Coal Alliance.

Read the full articles here:

(Lack of) progress in global electricity generation

Britain edges closer to zero coal

Solar farm in South Wales

Great Britain’s decline in coal use has rapidly accelerated its decarbonisation efforts. Annual coal power station emissions have shrunk over the past five years from 129 to 19 million tonnes of CO2 and helped reduce the average carbon intensity of electricity generation to a record low of 195 g/kWh last quarter.

However, this rapid pace of decarbonisation is unlikely to be sustained as growth in renewables faces a plateau, the country’s current nuclear capacity reaches retirement and the target of moving beyond coal by 2025 is completed.

Renewable sources now account for a steady 25% of annual electricity generation. These sources largely came onto the system through policies such as the government’s Renewables Obligation, which is now closed to entrants; Contracts for Differences, the future of which is uncertain for mature technologies like onshore wind and solar; and Feed-in Tariffs for roof-top solar installations which will close in April 2019. The end of these initiative paints a hazy picture of how future renewable capacity will be brought into the system.

Nuclear capacity also looks unlikely to expand at the rate needed to plug gaps in demand, with half of the country’s fleet expected to close for safety reasons by 2025. The Hinkley Point C nuclear power station, meanwhile, is only expected to come online at the end of that year.

Read the full article here:

Has Britain’s power sector decarbonisation stalled?

Ramsgate, Kent during summer 2018 heatwave

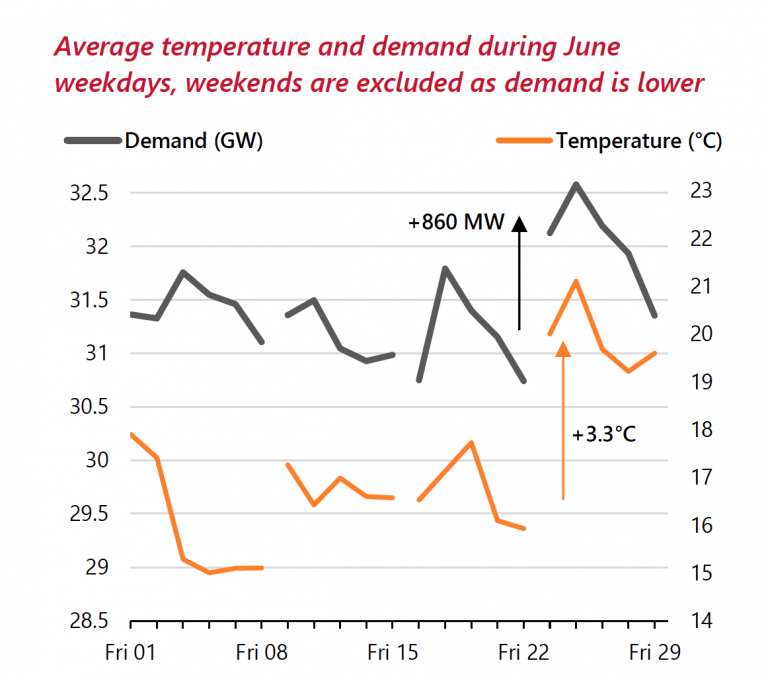

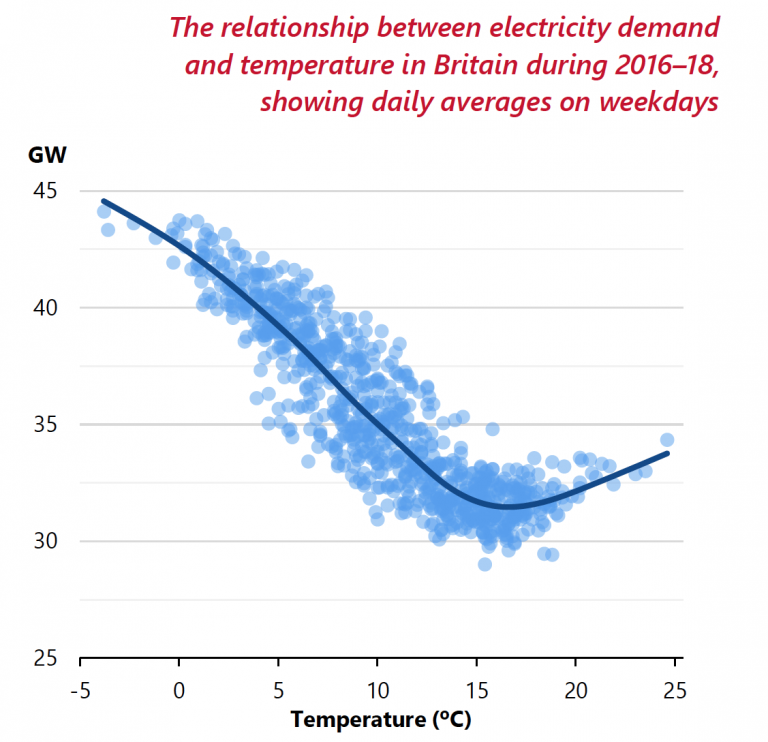

If the first quarter of 2018 was defined by low temperatures and heavy snowfall, the second quarter saw the impact of the opposite in weather conditions. From 23 June a heatwave set in around the country that saw temperatures increase by 3.3oC in a week, driving demand to jump 860 MW – the equivalent of an extra 2.5 million households, or an area the size of Scotland.

The increase in demand isn’t as drastic as when cold fronts hit, but if summers continue to get hotter this could change. Today, winter-time demand increases by 750 MW for every degree it drops below 14oC as electric heaters are plugged in to aid largely gas-based central-heating systems. When the mercury rises, however, demand increases by 350 MW for every degree rise over 20oC as businesses turn on air conditioning and the country’s refrigerators work harder.

These heatwave spikes are, at the moment, more easily dealt with than winter storms. While the Beast from the East saw demand reaching a peak of 53.3 GW, June’s topped out at 32.5 GW. The clear skies and long days of June also meant solar PV generation soared, making up for the ‘wind drought’ caused by the high-pressure weather. Wind output floated between 0.3 GW and 4.3 GW in June, far below its quarter peak to 13 GW. However, solar made up for this by peaking past 8 GW for 13 days in June and setting a new record of 9.39 GW at lunchtime on 27 June.

Read the full articles:

How the heat wave affects electricity demand

The summer wind drought and smashing solar

Explore the data in detail by visiting ElectricInsights.co.uk. Read the full report.

Commissioned by Drax, Electric Insights is produced, independently, by a team of academics from Imperial College London, led by Dr Iain Staffell and facilitated by the College’s consultancy company – Imperial Consultants.

27 July 2018

16.5 degrees is the Goldilocks temperature for the Brits – not hot enough for air-con, not too cold to put the heating on. In March we saw how the Beast from the East caused a surge in demand, now the long summer heatwave is doing the same.

June 23rd marked the start of the heatwave, with daytime temperatures surpassing 30°C in Scotland and Wales. The last week of June was 3.3°C warmer than the previous week, and demand was 860 MW higher (see chart below). This rise is equivalent to power demand from an extra 2.5 million households.

This reflects the growing role of air conditioning and refrigeration in shops, and cooling for data centres. Global electricity demand from cooling is rising dramatically, and is seen as a ‘blind spot’ in the global energy system. This will become more important as global temperatures, and more importantly, global incomes rise. However, it is easier to deal with than cold spells during winter because demand is low and solar PV output is high.

Below 14°C, demand increases by 750 MW for every degree it gets colder as buildings need more heating. Around a tenth of British homes have electric heating, as do half of commercial and public buildings. And while the UK is not synonymous with air conditioners, demand rises by 350 MW for each degree that temperature rises above 20°C.

This effect may well grow stronger in the coming years. National Grid expect that the peak load from air conditioners will triple in the coming decade. Perhaps events such as the current prolonged heatwave may spur more households to invest in air conditioning.

| Six months ended 30 June | H1 2018 | H1 2017 |

|---|---|---|

| Key financial performance measures | ||

| EBITDA (£ million)(1) | 102 | 121 |

| Underlying earnings (£ million)(2) | 7 | 9 |

| Underlying earnings per share (pence)(2) | 1.6 | 2.2 |

| Interim dividends (pence per share) | 5.6 | 4.9 |

| Net cash from operating activities (£ million) | 112 | 197 |

| Net debt (£ million)(3) | 366 | 372 |

| Statutory accounting measures | ||

| Operating profit/(loss) (£ million) | 12 | (61) |

| Loss before tax (£ million) | (11) | (104) |

| Reported basic loss per share (pence) | (1) | (21) |

“Drax continues to be at the heart of decarbonising UK energy, securing government support to convert a fourth unit to biomass and piloting a Bioenergy Carbon Capture and Storage project, supporting the UK Government’s carbon capture and storage ambitions.

“Drax continues to be at the heart of decarbonising UK energy, securing government support to convert a fourth unit to biomass and piloting a Bioenergy Carbon Capture and Storage project, supporting the UK Government’s carbon capture and storage ambitions.

“Full year EBITDA expectations remain unchanged. However, first half EBITDA was lower, principally due to two specific generation outages. We made excellent progress with our Pellet Production business, driving down costs while producing at record levels and our B2B Energy Supply business continues to increase customer numbers. We also remain on track with our investment projects: the conversion of a fourth unit to biomass, and the development of our OCGT and coal-to-gas repowering options.

“We remain focused on safe and efficient operations and returns to shareholders and expect to declare a full year dividend of £56 million for 2018.”