Capture For Growth

We believe investing in our people goes hand-in-hand with enabling the green energy transformation and positive future growth.

Information about our business, partnerships and campaigns, as well as photos, graphics and multimedia assets for journalists, and educational materials for schools.

Information about our business, partnerships and campaigns, as well as photos, graphics and multimedia assets for journalists, and educational materials for schools.

We’re committed to enabling a zero carbon, lower cost energy future through engineering, technology and innovation.

We’re building for a sustainable future in how we source our biomass, generate energy, remove carbon dioxide and function as a business.

Read our carbon capture, sustainable bioenergy and power generation stories, as well as thinking from Drax’s leaders and business updates.

Drax Group’s ambition is to become a carbon negative business by 2030, through innovative greenhouse gas removal technology.

Rt Hon Sajid Javid MP

Chancellor of the Exchequer

HM Treasury

1 Horse Guards Road London SW1A 2HQ

29 October 2019

Dear Chancellor,

We are writing to you to urge you to maintain the UK’s robust approach on carbon pricing. The prolonged uncertainty regarding the UK’s carbon pricing future as it exits the EU reiterates the need for the upcoming Budget – at whatever final date is chosen – to provide some much-needed certainty in a potentially turbulent period for businesses across the UK.

With its approach to carbon pricing, the Powering Past Coal Alliance and its Net Zero commitment, the UK has been a leader in global efforts to meet the ambition of the Paris Agreement by phasing out coal, as well as incentivising low carbon energy development and helping drive cost reductions. This leadership should continue at the first ‘Net Zero Budget’.

As outlined by the Committee on Climate Change in its recent advice to the UK Government on its carbon pricing future1, reaching net zero “will require a strong and rising carbon price, in order to induce changes to both short-term behaviour and longer-term investment decisions”. Importantly, in the run up to COP26 in Glasgow in November 2020, it is important that the UK continues its global leadership and is not perceived to waver on its commitment to tackling climate change.

Given the uncertainty over the UK’s exit from the EU there is little clarity on what the carbon pricing mechanism will be in the near term and this is already impacting on the forward pricing of carbon in electricity markets. Therefore, providing certainty and stability is crucial when the Government sets the Carbon Price Support (CPS) rate for April 2021 and beyond. Any reduction in CPS rates made in isolation of wider clarity on the UK’s carbon pricing arrangements post EU exit risks sending a negative signal to low carbon investors and undermining the continuing need for a strong and rising carbon price.

In addition to the considerations on the CPS, the Carbon Emissions Tax (CET) – that will replace the EU ETS in the event that the UK leaves the EU without a deal – will need to be set out for 2020 as soon as possible. To minimise the potential divergence between the CET and the EU ETS over 2020 it is vital that the CET is set a level for 2020 that is comparable with recent EU ETS pricing.

We look forward to measures to help the UK meet its leading ambitions at the first ‘Net Zero Budget’, including certainty and stability on the CPS. Further clarity on the UK’s carbon pricing future following a successful linking agreement between a UK ETS and the EU ETS to be in place for 2021 should be provided as soon as is practicable.

Signed,

Simon Clarke MP, Exchequer Secretary to the Treasury

Rt Hon Andrea Leadsom MP, Secretary of State for Business, Energy and Industrial Strategy

Rt Hon Kwasi Kwarteng MP, Minister of State for Business, Energy and Industrial Strategy

Lord Ian Duncan, Parliamentary Under Secretary of State for Business, Energy and Industrial Strategy

Rt Hon Claire Perry O’Neill MP, UNFCCC COP26 President

Following formal confirmation from the UK Government, Drax expects the Capacity Market to be re-instated shortly, with full retrospective payments made for the capacity provided. Capacity payments due to Drax for 2019 and since the suspension of the Capacity Market in 2018 are £75 million. Drax expects these to be included in 2019 EBITDA.

Drax expects the decision will allow future Capacity Market auctions to take place in early 2020. Drax retains options for new gas generation, which could be developed subject to appropriate clearing prices in future Capacity Market auctions.

A link to the European Commission’s decision is provided below.

https://europa.eu/rapid/press-release_IP-19-6152_en.htm

“This is great news for the UK energy system. The capacity market helps to ensure Britain has the flexible and reliable power generating capacity needed to support the economy as it continues to decarbonise, keeping the lights on at the lowest cost for millions of homes and businesses.

“We will be prequalifying a number of Drax’s flexible and reliable power stations, as well as some of our development projects, later this year with a view to participating in the capacity markets auctions in 2020.”

Drax Investor Relations: Mark Strafford

+44 (0) 1757 612 491

Drax External Communications: Matt Willey

+44 (0) 203 943 4306

Website: www.drax.com/uk

END

RNS Number : 0491R

The future of electric cars and electric vans holds great potential – not just for the transport industry’s overall carbon footprint, but for the populations of heavily congested, polluted cities and even individual drivers looking for more efficient fuel costs.

That future is approaching fast. By 2040 or even as soon as 2035 no new cars or vans sold in the UK can be solely powered by diesel or petrol. While this is a positive step, it brings with it a shift in the way drivers will need to manage the way they plan journeys and, more importantly, refuel.

For years drivers have relied on a quick and plentiful supply of fuel at petrol stations. But an EV doesn’t charge as quickly as a conventional car, nor are fast charging points widespread – at least not right now.

The change will be considerable, but it won’t necessarily take shape in a single form. Here we look at four things that will become increasingly influential in how drivers recharge their EVs over the coming years.

Electricity costs more to produce and supply at certain times of the day. This wholesale price depends on the demand for power, weather conditions and the costs of different generation technologies and fuels.

For example, electricity is often more expensive in the evenings when people are coming home from work and turning on lights, TVs, ovens and plugging in devices. Just a few hours later it rapidly drops in price as homes and offices turn off lights and appliances. But the power system is changing.

The price of electricity is increasingly driven by less predictable factors such as the weather. On windy and sunny days, wind and solar generation can drive down the cost of producing power. On calm and cloudy days, the costs of electricity can increase.

While this, in theory, makes it sensible to wait for a cheap period of time to plug in and charge an electric vehicle (EV), in practice people are unlikely to spend the time sit refreshing websites which display the price of electricity in real time to get the best value. Instead, the use of ‘smart charging technology’ can play a big role to capitalise on fluctuations in prices.

Smart charging technology will be able to monitor things like electricity prices and even electricity usage across an entire site (for example across a business where many devices are using electricity) and automate the charging process to make use of the best prices and limit overall electricity use.

Rather than needing someone to recharge EVs at one o’clock in the morning, this means people or businesses can plug in at times convenient to them and set their vehicles to charge at the cheapest times and have an appropriate amount of charge to carry out tasks when they need to.

“By shifting power usage into cheaper periods you’re saving money and you can be more sympathetic to supply and demand limits on a company,” explains Adam Hall, who leads Drax’s EV proposition. “If I know my battery will be fully charged by nine in the morning, do I care if it charges immediately or delays it and saves me a few pounds?” For business fleet owners who manage large numbers of electric vehicles the difference this can make is even larger, he adds.

Each EV has a battery in it that powers the vehicle’s motor. But what if the electricity stored in that battery could also be harnessed to deliver electricity back to grid? And what if that concept could be used to collect a small portion of power from every idle EV in the country and use it to plug gaps in the electricity system?

“There are over 30 million cars on UK roads. National Grid predicts by 2050, 99% of those vehicles will be powered by electricity,” explains Hall. “The majority of cars remain idle for 95% of any day. That’s a huge amount of storage potential that could be used to balance the grid at key times. It’s a battery network that assets around the country will be able to use.”

This concept is what’s called vehicle to grid technology (V2G), and while it holds great potential, it’s still some way from becoming a mainstream source of reserve power. Right now the technology is costly and limited – only ‘CHAdeMO’ charging systems, as found on Japanese models, actually support bi-directional charging. Nevertheless, Hall remains optimistic of its future role in the energy system, particularly as this technology will be hugely important in managing future grid constraints

“The cost of bi-directional hardware is coming down all the time,” he says. “At the moment there aren’t enough vehicles, we don’t have the scale to do it, but I fully believe it will change quite dramatically.”

For domestic users the benefit will be less immediate than it will be for entire countries. For business fleet managers, allowing the grid to take some power from their idle vehicles could lead to financial compensation or other advantages for offering grid support.

More suited for businesses managing whole fleets of vehicles, employing a third party to manage the charging of vehicles allows for the delegation of a potentially costly and time-consuming task.

Adam Hall, Drax EV proposition lead, with Drax’s electric vehicle fleet service.

“Effectively the customer knows they’ll get the vehicles with the amount of charge they want when they need it,” says Hall. “That might be for the cheapest price or as fast as possible. It means the customer doesn’t have to think, they just get their charged vehicle in the optimum way for their needs.”

Third party providers could also open up new charging businesses models, such as flat monthly rates for unlimited vehicle charging or all-renewable services. By taking the technical aspects of running a fleet out of businesses hands, third parties could even serve to lower the barrier to EV adoption.

It’s difficult to accurately know how much demand electric vehicles will place on the electricity system– some estimates see demand growing in Great Britain as much as 22% by 2050 as a result of EVs.

While the constant development of battery and charging technology will likely mean this prediction will come down, there are some theories as to how the country will need to deal with this rapid growth. One of these is to actually turn down the electricity surging through charging points at certain points to prevent widespread blackouts.

While the constant development of battery and charging technology will likely mean this prediction will come down, there are some theories as to how the country will need to deal with this rapid growth. One of these is to actually turn down the electricity surging through charging points at certain points to prevent widespread blackouts.

“The idea is there to protect the grid,” explains Hall. “When local distribution networks have a lot of demand they may need to turn charge points down.” He adds there will likely be exemptions for emergency services, however.

Hall is sceptical mandatory managed charging would ever really come into play, for the damage it would do to consumer attitudes to EVs. The idea also taps into wider scaremongering around EVs and quite how much they will push up electricity demand.

Instead what will really need to shift for a future of efficiently charged vehicles is a mindset shift. “There’s a psychological element to it,” he suggests. “Everyone goes through some range anxiety at first but soon realises the technology is sound.”

As battery technology continues to improve, vehicles evolve to go further on a single charge, and networks of super-fast charge points expand, transitioning to electric vehicles will become easier and more economical for businesses than continuing to depend on fossil fuel.

“I personally believe once electric vehicles are doing 300 miles on a single charge, the requirement for on-route charging will be pretty low,” says Hall. “Not many people drive 300 miles, need to recharge at a service station and then drive anther 300 in one fell swoop. It’s much more important to have good charging installations at work and at home.”

There are many ways in which EVs will change the way the world drives, from how we charge them to how and where we travel. We can be certain this will mean a shift in mindsets and our approach to transport. What remains uncertain is just how quickly and widespread that shift will be.

28 July 2019

Climate change is the biggest challenge of our time and Drax has a crucial role in tackling it.

All countries around the world need to reduce carbon emissions while at the same time growing their economies. Creating enough clean, secure energy for industry, transport and people’s daily lives has never been more important.

Drax is at the heart of the UK energy system. Recently the UK government committed to delivering a net-zero carbon emissions by 2050 and Drax is equally committed to helping make that possible.

We’ve recently had some questions about what we’re doing and I’d like to set the record straight.

At Drax we’re committed to a zero-carbon, lower-cost energy future.

And we’ve accelerated our efforts to help the UK get off coal by converting our power station to using sustainable biomass. And now we’re the largest decarbonisation project in Europe.

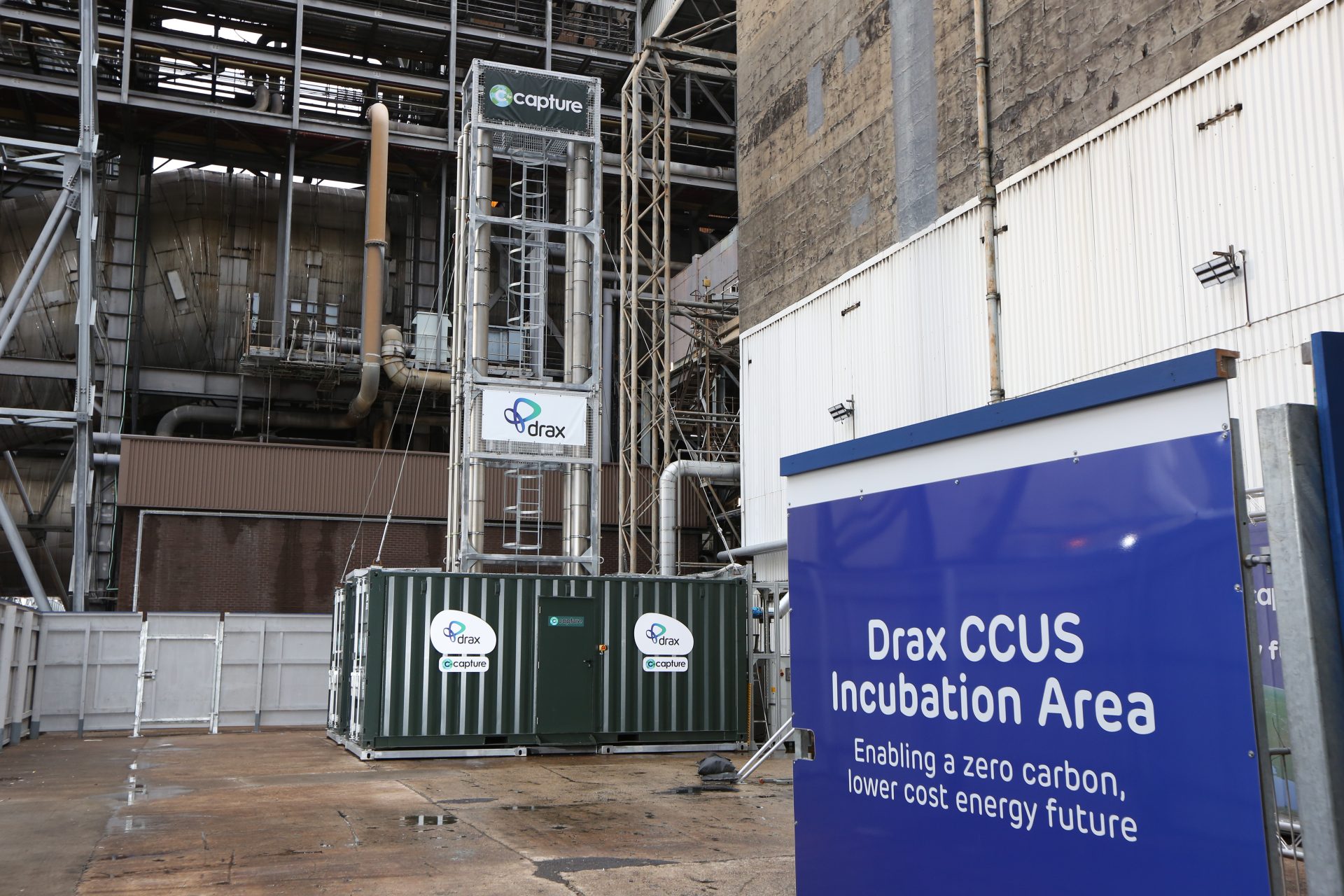

We’re exploring how Drax Power Station can become the anchor to enable revolutionary technologies to capture carbon in the North of England.

And we’re creating more energy stability, so that more wind and solar power can come onto the grid.

And finally, we’re helping our customers take control of their energy – so they can use it more efficiently and spend less.

No. Since 2012 we’ve reduced our CO2 emissions by 84%. In that time, we moved from being western Europe’s largest polluter to being the home of the largest decarbonisation project in Europe.

And we want to do more.

We’ve expanded our operations to include hydro power, storage and natural gas and we’ve continued to bring coal off the system.

By the mid 2020s, our ambition is to create a power station that both generates electricity and removes carbon from the atmosphere at the same time.

Our energy system is changing rapidly as we move to use more wind and solar power.

At the same time, we need new technologies that can operate when the wind is not blowing and the sun is not shining.

A new, more efficient gas plant can fill that gap and help make it possible for the UK to come off coal before the government’s deadline of 2025.

Importantly, if we put new gas in place we need to make sure that there’s a route through for making that zero-carbon over time by being able to capture the CO2 or by converting those power plants into hydrogen.

No.

Sustainable biomass from healthy managed forests is helping decarbonise the UK’s energy system as well as helping to promote healthy forest growth.

Biomass has been a critical element in the UK’s decarbonisation journey. Helping us get off coal much faster than anyone thought possible.

The biomass that we use comes from sustainably managed forests that supply industries like construction. We use residues, like sawdust and waste wood, that other parts of industry don’t use.

We support healthy forests and biodiversity. The biomass that we use is renewable because the forests are growing and continue to capture more carbon than we emit from the power station.

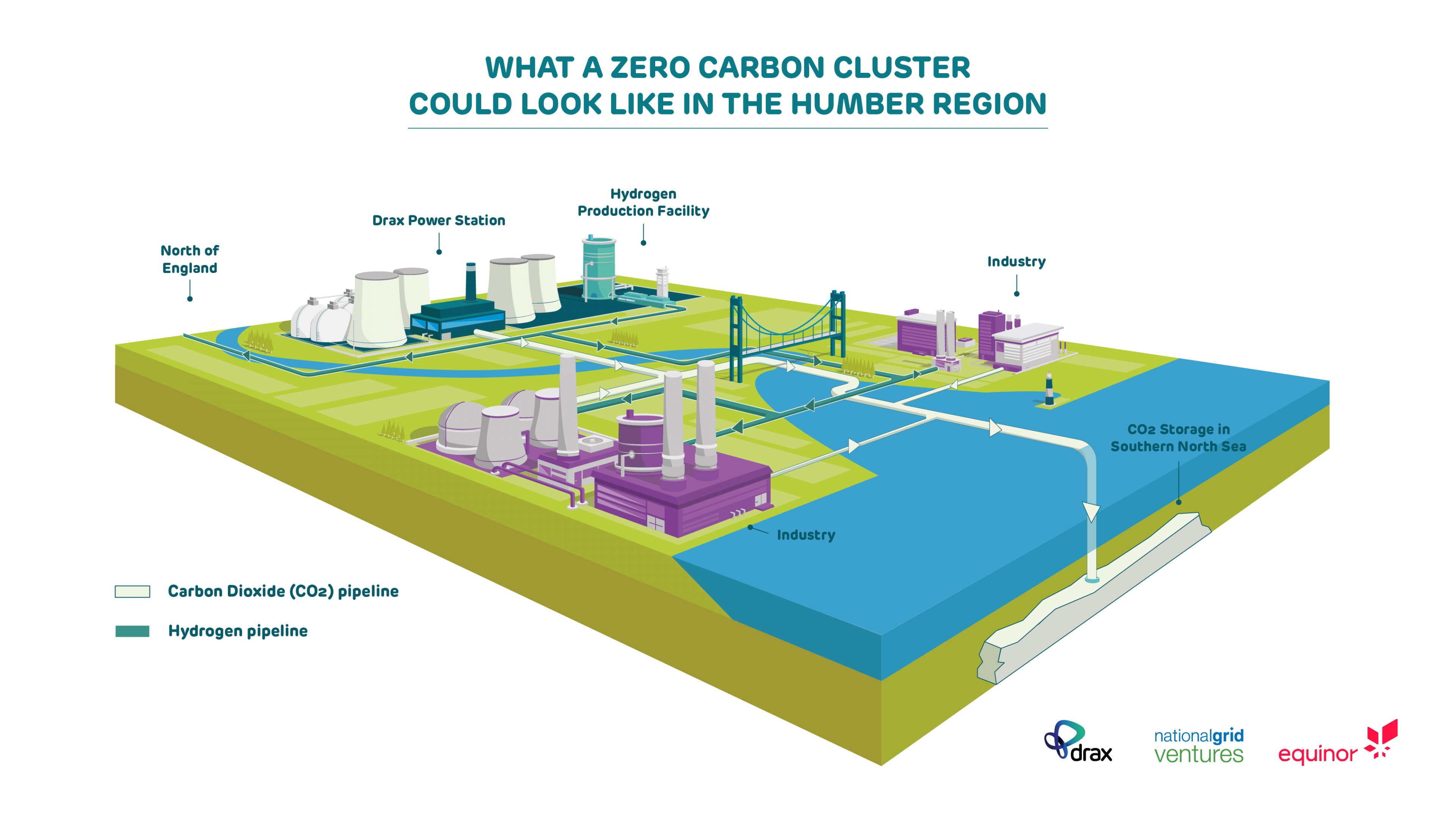

What’s exciting is that this technology enables us to do more. We are piloting carbon capture with bioenergy at the power station. Which could enable us to become the first carbon-negative power station in the world and also the anchor for new zero-carbon cluster across the Humber and the North.

I took this job because Drax has already done a tremendous amount to help fight climate change in the UK. But I also believe passionately that there is more that we can do.

I want to use all of our capabilities to continue fighting climate change.

I also want to make sure that we listen to what everyone else has to say to ensure that we continue to do the right thing.

17 July 2019

The starting gun has fired and the challenge is underway. The government has officially set 2050 as the target year in which the UK will achieve carbon neutrality.

There’s no denying this economy-wide transformation will need a great deal of investment. Reaching net zero carbon emissions will require an evolutionary overhaul of not just Great Britain’s electricity system but the UK economy as a whole. And indeed, the way we live our lives and go about our business.

But that doesn’t mean it’s out of reach. Instead it will fall to technologies such as carbon capture usage and storage (CCUS), as well as bioenergy with carbon capture and storage (BECCS), to make it economical and possible.

The UK’s Committee on Climate Change (CCC) estimates the price of decarbonisation will cost as little as 1% of forecast GDP per annum in 2050.

However, the Business, Energy and Industrial Strategy (BEIS) Select Committee inquiry found that failure to deploy CCUS and BECCS technology could double the cost to 2%. There are a number of reasons for this, such as the cost to jobs, productivity and living standards of shutting down industrial emitters. CCUS’s ability to contribute to a hydrogen economy can help avoid this.

Moreover, the CCC claims even with industries striving to decarbonise rapidly, as much as 100 megatonnes of hard-to-abate carbon dioxide (CO2) is expected to remain in the UK economy by 2050.

This makes carbon negative techniques and technologies, such as BECCS – which uses woody biomass that has absorbed carbon in its lifetime as forests – alongside direct air capture (DAC), the boosting of ocean plant productivity, much greater tree planting and better sequestration of carbon in soil, essential if the UK is to attain true carbon neutrality.

The importance of BECCS and CCUS in the zero carbon future is clear. Now is the time for rapid development. Not in 2030, not in 2040, but today in 2019 and into the 2020s.

But doing this requires the government to move beyond its historic policies that have failed to support the technology in the past. Progress needs long-term frameworks that provide private sector investors with the certainty they need to kick-start the commercial-scale deployment of CCUS technologies.

For carbon capture to become an integrated part of the energy system it must deliver value well beyond the energy sector. Establishing markets for products developed from captured carbon will play a role here, but to set the wheels in motion, financial frameworks are needed that can allow BECCS and CCUS to thrive.

One device that can allow the market to develop CCUS is the creation of contracts for difference (CfDs) for carbon capture. These currently exist in the low-carbon generation space, between generators and the government-owned Low Carbon Contracts Company (LCCC). Through these contracts, power generators are paid the difference between their cost of generating low carbon electricity (known as a strike price) and the price of electricity in Great Britain’s wholesale power market. If the power price in the market is higher than the strike price generators pay the difference back to the LCCC, meaning consumers are protected from price spikes too.

It means that the generator is protected from market volatility or big drops in the wholesale price of power, offering the security to invest in new technology. More than this, CfDs last many years meaning they transcend political cycles and the cost per megawatt can be reduced with a longer contract. Creating a market for carbon capture or negative emissions generation could offer the same security to generators to invest in the technology.

A CfD for BECCS should not only incentivise the building of infrastructure to capture carbon, but we must also recognise the valuable role that negative emissions can play. By compensating BECCS producers for their negative emissions, it should provide a lower cost alternative to reducing all other CO2 emissions to zero, while still ensuring that the UK can get to net zero.

Beyond installing carbon capture at existing generation sites, one of the major financial barriers to the wider deployment of CCUS and BECCS is the cost and liability associated with transporting and storing captured carbon.

A Regulated Asset Base (RAB) funding model, would encourage investment by gradually recovering the costs of transport and storage via a regulated return. This approach is currently under consideration as a means of financing other major infrastructure projects.

A RAB allows businesses, including investment and pension funds, to invest in projects under the oversight of a government regulator. In exchange for their commitment, investors can collect a fee through regular consumer and non-domestic bills.

Ultimately, the current carbon trading system is based around charging polluters. But as we approach a post-coal UK and in order to achieve net zero, it’s necessary for this to evolve – from economically disincentivising emissions to incentivising carbon-negative power generation.

However, with the cost of carbon capture and negative emissions differing between types of industries and technologies, there’s a requirement to consider differentiated carbon prices to guide industry through long-term strategy. But the need for carbon capture development is too pressing for us as an industry to wait.

At Drax Power Station our BECCS pilot is just the beginning of our wider ambitions to become the first negative emissions power station. Our use of biomass already makes Drax Power Station the largest generator of renewable electricity in Great Britain. The responsibly-managed working forests our suppliers source from absorbed carbon from the atmosphere as they grew so adding carbon capture at scale to this supply chain can turn our operation from low carbon, to carbon-neutral and eventually carbon negative.

And we have bigger plans still to create a net zero carbon industrial cluster in the Humber region, in partnership with Equinor and National Grid. The cluster would deliver carbon capture at the scale needed to not just decarbonise the most carbon-intensive industrial region in the UK, but to put the country at the forefront of the decarbonisation of industry and manufacturing.

Government action is needed to make CCUS and BECCS economically sustainable at scale as an integrated part of our energy system. However, the onus is on us, the energy industry to lead development and act as trusted partners that can deliver the decarbonisation needed to reach net zero carbon by 2050.

Demand for electricity might have been 6% lower in the first three months of 2019 than in last year’s first quarter but the demand for lower carbon power is only growing and there’s more pressure than ever for global industries to decarbonise more rapidly.

Aided by a significantly milder winter than last year, Great Britain’s electricity sector continued to make further progress in reducing carbon emissions in the first quarter (Q1) of 2019.

The carbon intensity of Great Britain’s electricity was almost 20% lower in Q1 2019 than in the same period last year. This was driven by a significant decrease in coal usage, with 581 coal-free hours in total over the period – eight times more than in Q1 2018. This trend has only increased, with May seeing the country’s first coal-free week in modern times.

The findings come from Electric Insights, a report commissioned by Drax and written independently by researchers from Imperial College London, that analyses Great Britain’s electricity consumption and looks at what the future might hold.

As public, commercial and political demand for lower carbon emissions mounts, the question for the power system is: can it truly reach zero-emissions?

Quarter after quarter, the carbon intensity of Great Britain’s electricity system has declined. From 545 grams of carbon dioxide (CO2) per kilowatt hour (g/kWh) in Q1 2012, to just over 200 g/kWh last quarter. For a single hour, carbon emissions have fallen as low as just 56 g/kWh. But how soon can that figure reach all the way down to net-zero carbon emissions?

Quarter after quarter, the carbon intensity of Great Britain’s electricity system has declined. From 545 grams of carbon dioxide (CO2) per kilowatt hour (g/kWh) in Q1 2012, to just over 200 g/kWh last quarter. For a single hour, carbon emissions have fallen as low as just 56 g/kWh. But how soon can that figure reach all the way down to net-zero carbon emissions?

The National Grid’s Electricity System Operator (ESO), believes it could be as soon as 2025. But some serious changes are needed to make it possible for the system to operate safely and efficiently, when you have fewer sources offering balancing services like reserve power, inertia, frequency response and voltage control.

The National Grid ESO believes an approach that establishes a marketplace for trading services holds the solution. The hope is that competition will breed new innovation and bring new technologies such as grid-scale storage and AI into the commercial energy markets, offering reserve power and more accurate forecasting for solar and wind power.

For the meantime, weather-dependent technologies are a key source of renewable electricity in Great Britain, with wind making up more than 20% of all generation in Q1 2019. However, with wind capacity only expected to increase, how should the system react when it’s not an option?

Read the full article, co-authored by Julian Leslie, Head of National Control, National Grid ESO: How low can we go?

Today there are around 20 gigawatts (GW) of wind capacity installed around Great Britain, and this is forecast to double to 40 GW in the next seven years. However, average wind output can fluctuate between 2 GW one day and 12 GW the next – as happened twice in January. It highlights the ongoing needs for flexibility and diversity of sources in the electricity system even as it decarbonises.

There are a number of ways to make up for shortfalls in wind generation. The most obvious of which is through other existing sources. There is more solar installed around the county than any source of generation (except gas), at 12.9 GW and sun power helped meet demand during a wind drought last summer. Solar averaged 1.3 GW over the last 12 months, this is more than coal which accounted for 1.1 GW.

However, storage will also be important in delivering low or zero-carbon sources of electricity when there is neither wind nor sufficient sunlight. At present this includes pumped storage and some battery technologies, but in future will include greater use of grid-scale lithium-ion batteries, as well as vehicle-to-grid systems that can take advantage of power stored in idle electric cars.

New fuels, particularly hydrogen, also have the potential to meet demand and help create a wider lower-carbon economy for heating, as well as vehicle fuel, with water as the only emission.

Hydrogen can be produced from natural gas or using excess electricity from renewable sources, or through carbon capture from industrial emissions. It can then be stored for a long time and at scale, before being used to generate electricity rapidly when needed.

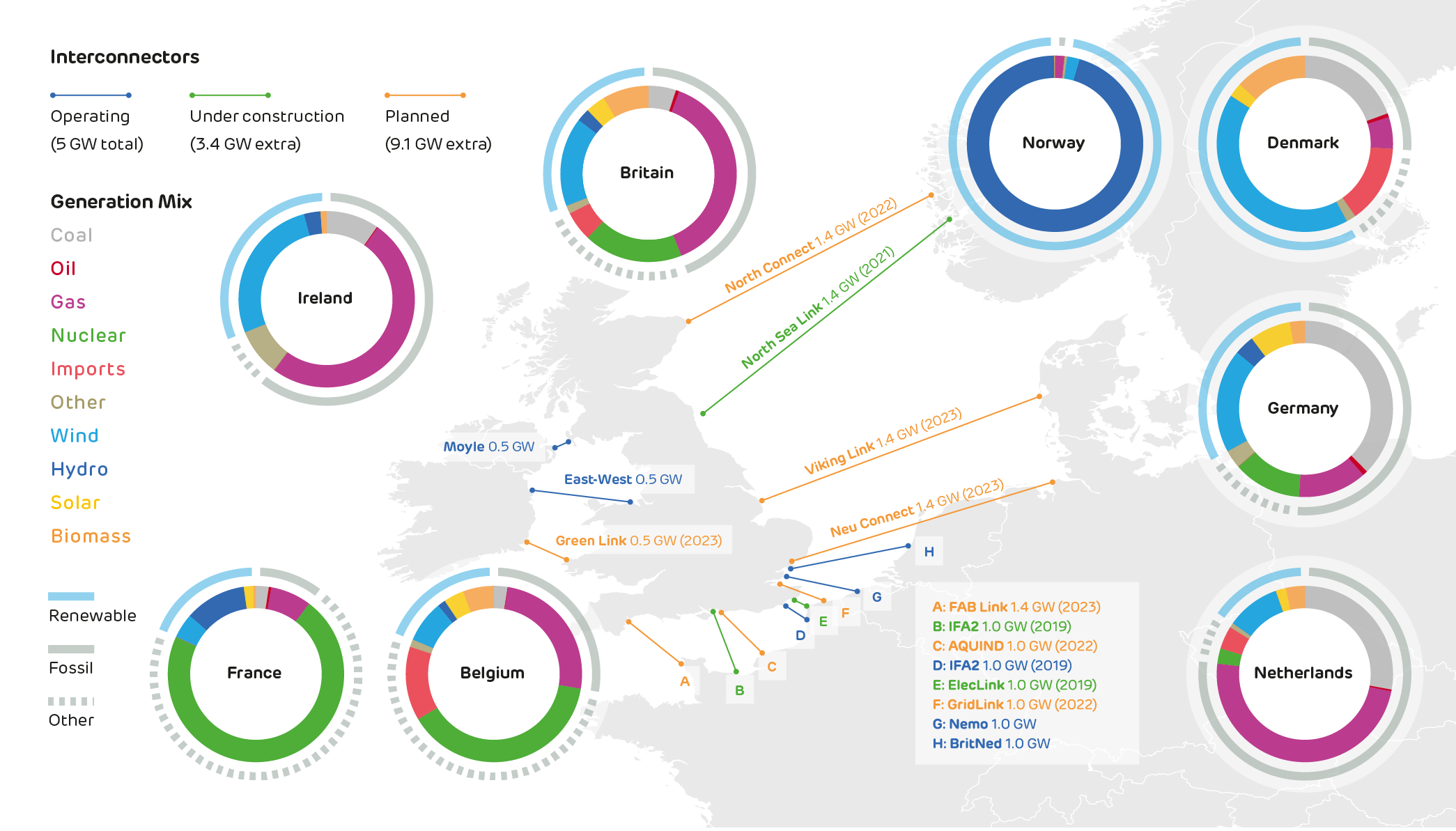

Another increasingly important source of Great Britain’s electricity is interconnectors. However, they are not yet being used in a way that can support gaps in the electricity system, with Northern European countries normally all experiencing the same weather – and wind levels – at the same time.

Read the full article: What to do when the wind doesn’t blow?

Great Britain added a new power source to its electricity system in Q1 2019, in the form of Belgium. The opening of the £600 million NEMO link between Kent and Zeebrugge added another 1 GW of interconnection capacity.

Great Britain added a new power source to its electricity system in Q1 2019, in the form of Belgium. The opening of the £600 million NEMO link between Kent and Zeebrugge added another 1 GW of interconnection capacity.

It joins connections to France, the Netherlands, Northern Ireland and the Republic of Ireland to bring Great Britain’s total interconnection capacity to 5 GW. These links accounted for 7.9% of the 78 terawatt hours (TWh) of electricity consumed over the quarter.

Electricity from imports also set new records for a daily average of 4.3 GW on 24 February, accounting for 12.9% of total consumption, and a monthly average in March when it made up 10.6% of consumption. These records represent the first time Great Britain fell below 90% for electricity self-sufficiency.

With 3.4 GW of new interconnectors under construction coming online by 2022 and 9.1 GW more planned to be completed over the next five years, Great Britain’s neighbours are set to play a growing role in the country’s electricity mix.

However, while interconnectors offer an often cost-effective way for Great Britain to ensure electricity supply meets demand, the carbon intensity of neighbouring countries’ electricity should also be considered.

Read the full article: 10% of electricity now generated abroad

The new link to Belgium has imported, rather than exported, electricity every day since it began operations, as Belgium has the lowest natural gas prices in Europe and its power stations pay £16 per tonne less for carbon emissions than their British counterparts. This makes it cheaper to import, and less carbon intense, than electricity from the more coal-dependant Netherlands and Ireland.

Planned links to Germany and Denmark could allow Great Britain to import more renewable power. However, if there is a wind drought across Northern Europe these countries often turn to their emissions-heavy coal or even dirtier lignite sources.

France is currently Great Britain’s cleanest source of imports, mostly using nuclear and renewable generation. However, when the North Sea Link opens in 2021, it will give Great Britain access to Norway’s abundance of hydro-power to plug gaps in renewable generation.

Considering the carbon intensity of Great Britain’s imports is important because the decarbonisation needed to address the global climate change emergency can’t be solved by one country alone. For electricity emissions to go as low as they can it takes collaboration that goes across borders.

Read the full article: Where do Britain’s imports come from?

How low carbon can Britain’s electricity go? As low as zero carbon still seems a long way off but every year records continue to be broken for all types of renewable electricity. 2018 was no different.

Over the full 12-month period, 53% of all Britain’s electricity was produced from low carbon sources, which includes both renewable and nuclear generation, up from 50% in 2017. The increase in low carbon shoved fossil fuel generation down to just 47% of the country’s overall mix.

The findings come from Electric Insights, a quarterly report commissioned by Drax and written by researchers from Imperial College London.

The report found electricity’s average carbon intensity fell 8% to 217 grams of carbon dioxide per kilowatt-hour of electricity generated (g/kWh), and while this continues an ongoing decline that keeps the country on track to meet the Committee on Climate Change’s target of 100 g/kWh by 2030, it was, however, the slowest rate of decline since 2013.

It also highlights that while Britain can continue to decarbonise in 2019, the challenges of the years ahead will make it tougher to continue to break the records it has over the past few years.

Last year, every type of renewable record that could be broken, was broken. Wind, solar and biomass all set new 10-year highs for respective annual, monthly and daily generation, as well as records for instantaneous output (generation over a half-hour period) and share of the electricity mix. The result was a new instantaneous generation high of 21 gigawatts (GW) for renewables, 58% of total output.

Wind had a particularly good year of renewable record-setting. It broke the 15 GW barrier for instantaneous output for the first time and accounted for 48% of total generation during a half hour period at 5am on 18 December.

Overall low carbon generation, which takes into account renewables and nuclear (both that generated in Britain and imported from French reactors), had an equally record-breaking year with an average of almost 18 GW across the full year and a new record for instantaneous output of 30 GW at 1pm on 14 June – nearly 90% of total generation over the half hour period.

While low carbon and individual renewable electricity sources hit record highs, there were also some milestone lows. Coal accounted for an average of just 5% of electricity output over the year, hitting a record low in June, when it made up just 1% of that month’s total generation. Fossil fuel output overall had a similarly significant decline, hitting a decade-low of 15 GW on average for 2018 – 44% of total generation over the year.

One fossil fuel that bucked the trend, however, was gas, which hit an all-time output of 27 GW for instantaneous generation on the night of 26 January. There was low wind on that day last year, plus much of the nuclear fleet was out of action for reactor maintenance. In one case, with seaweed clogging a cooling system.

This was all aided by an ongoing decline in overall demand as ever smarter and more efficient devices helped the country reach the decade’s lowest annual average demand of 33.5 GW. More impressive when considering how much the country’s electricity system has changed over the last decade, however, is the record low demand net of wind and solar. Only 9.9 GW was needed from other energy technologies at 4am on 14 June.

The most remarkable change in Britain’s electricity mix has been how far out of favour coal has fallen. From its position as the primary source from 2012 to 2014, in the space of four years it has crashed down to sixth in the mix with nuclear, wind, imports, biomass and gas all playing bigger roles in the system.

This sudden decline in 2015 was the result of the carbon price nearly doubling from £9.54 to £18.08 per tonne of carbon dioxide (CO2) in April, making profitable coal power stations loss-making overnight. With coal continuing to crash out of the mix, biomass has become the most-used solid fuel in Britain’s electricity system.

Interconnectors are also playing a more significant part in Britain’s electricity mix since their introduction to the capacity market in 2015. Thanks to increased interconnection to Europe, Britain is now a net importer of electricity, with 22 TWh brought in from Europe in 2018 – nine times more than it exported.

While more of Britain’s electricity comes from underwater power lines, less of it is being generated by water itself. Hydro’s decline from the fifth largest source of electricity to the eighth is the most noticeable shift outside coal’s slide. New large-scale hydro installations are expensive and a secondary focus for the government compared with cheaper renewables.

Hydro’s role in the electricity mix is also affected by drier, hotter summers, which means lower water levels. For solar, by contrast, the warmer weather will see it play a bigger role and it’s expected to overtake coal in either 2019 or 2020.

What is unlikely to change in the near-future, however, is the position at the top. In 2018 gas generated 115 TWh – more than nuclear and wind combined. But this is just one constant in a future of multiple moving and uncertain parts.

Britain is on course to leave the EU on 29 March. The effects this will have on the electricity system are still unknown, but one influential factor could be Britain’s exit from the Emissions Trading Scheme (ETS), the EU-wide market which sets prices of carbon emitted by generators. This may mean that rather than paying a carbon price on top of the ETS, as is currently the case, Britain’s generators will only have to pay the new, fixed carbon tax of £16 per tonne the UK government says will come into play in April, topped up by the carbon price support (CPS) of £18/tonne.

Lower prices for carbon relative to the fluctuating ETS + CPS, could make coal suddenly economically viable again. The black stuff could potentially become cheaper than other power sources. This about-turn could cause the carbon intensity of electricity generation to bounce up again in one or more years between 2019 and 2025, the date all coal power units will have been decommissioned.

The knock-on effect of lower carbon prices, combined with fluctuations in the Pound against the Euro, could see a reverse from imports to exports as Britain pumps its cheap, potentially coal-generated, electricity over to its European neighbours. That’s if the interconnectors can continue to function as efficiently as they do at present, which some parties believe won’t be the case if human traders have to replace the automatic trading systems currently in place.

Sizewell B Nuclear Power Station

A reversal of importing to exporting could also reduce the amount of nuclear electricity coming into the country from France. Future nuclear generation in Britain also looks in doubt with Toshiba and Hitachi’s decisions to shelve their respective plans for new nuclear reactors, which could leave a 9 GW hole in the low-carbon base capacity that nuclear normally provides.

Renewables have the potential to fill the gap and become an even bigger part of the electricity system, but this will require a push for new installations. 2018 saw a 60% drop in new wind and solar installations and less than 2 GW of new renewable capacity came onto the system, making it the slowest year for renewable growth since 2010.

Britain’s electricity has seen significant change over the last decade and 2018 once again saw the country take significant strides towards a low carbon future, but challenges lie ahead. Records might be harder to break, but it is important the momentum continues to move towards renewable, sustainable electricity.

1 February 2019

Think of the phrase ‘3D’ and may people instantly think of video games, television or cinema, along with the special glasses you needed to watch it.

But another form of 3D is, I believe, going to be at the heart of the energy revolution which is rapidly gathering place.

The three Ds in this case are Data, Diversification and Decarbonisation. Together, they will transform the way businesses buy, use and sell their energy, help companies take control of their energy use and save money and also play a key part in our journey towards a zero carbon, lower cost energy future.

We’re already seeing some real innovations in the energy sector. Our trial of a storage battery with a customer of Opus Energy is an example, offering a farming business in Northampton the chance to sell stored energy generated by solar panels back to the grid at times of peak demand – a potential new revenue stream.

But other innovations and advances will maintain the pace of change and data will be at the core of this now the new generation of smart meters are being installed in businesses, revolutionising customer relationships with their energy suppliers.

The data from the new meters will finally give customers insight into where and when they use energy. Suppliers will have to work much more closely with customers to help them access new opportunities for cost savings, access to new markets and even new revenue streams.

An example would be a restaurant. With the data smart meters will provide, the restaurant’s supplier will be able to tell the owners how their energy use compares to the local competition and where improvements can be made.

The detail could go as far as identifying whether the restaurant’s equipment is older and less efficient, whether rivals have installed newer kit or whether other businesses are switching off their equipment earlier or using it at different, cheaper times.

Using energy during the peak weekday morning and early evening hours is often the most expensive time to do so. Data will give businesses the insight into how they can use energy more efficiently and when they use it, offering them the chance to avoid buying at peak times whenever possible and driving efficiencies.

This is why Haven Power’s trading team is now working closely with GridBeyond. The partnership allows our customers to trade the power they produce as well as optimise their operations to help balance the grid at times of peak demand. The really smart thing is that in doing so, customers are reducing their energy costs and making their operations more sustainable.

Trading desks at Haven Power’s Ipswich HQ

The way demand changes and is managed by businesses and consumers on a diversified power system will also be key. The business energy sector is already diversifying as many customers are able to generate and store their own power but the next step is for more customers to be paid to reduce their usage at peak times.

Think of a busy time for the National Grid – half time in the FA Cup Final or after the results in Strictly Come Dancing. Previously, the grid would have to pay a power station to ramp up generation to meet demand but these days, customers are paid to reduce demand for 30 minutes or so – in effect becoming a huge virtual power station.

This has happened for some time of course with larger, industrial customers but now, smaller companies can benefit from this too, thanks to the data and insight they will have from their smart meters. This empowers customers and puts them, not the energy companies, in control of the key decisions about their energy.

A close, advisory relationship between energy suppliers and their customers will become ever more important to make sure business can choose to avoid the high demand periods, and maximises use during the lower, cheaper times. In fact, I can see a time when customers will end up paying more for insight and advice than they do for the power they buy – and they’ll save money overall in doing so.

And if we get all this right, it will help drive one of the most important of the three Ds – decarbonisation.

Sustainability is increasingly becoming a primary focus for businesses and demand for renewable energy is growing because it is now cost-effective. That will help us in our drive towards a zero carbon future as more and more renewable energy comes onstream, though the UK will continue to need power generated from more flexible assets as well.

So there are huge opportunities out there to transform our energy landscape but they have to be viewed positively. The smart metering programme can be viewed as a regulatory burden or it can be seen as an opportunity. We take the positive view.

Likewise, batteries were once the preserve of massive companies only but now, as technology develops, they are becoming available for smaller firms too. The more we can innovative on a larger scale, the more the technology will work its way into smaller markets too, adding momentum to the energy revolution.

The opportunities are huge. If we get it right, so too will be the benefits to one of the biggest priorities of all – the work to decarbonise the UK and create the lower carbon future we all want.