Capture For Growth

Chapter 1:

Foreword, Executive Summary & The Industrial Challenge of Climate Change

Foreword

The UK is a leader in the global effort to tackle climate change. It has shown the rest of the world that protecting the environment and creating economic growth can go hand in hand.

The evidence is visible across the UK economy. As businesses have stepped up to the challenge, UK emissions have fallen by over 40% since 1990, while GDP has grown by two thirds. Clean growth is at the heart of this success story. Almost £100bn has been invested in renewables in the UK over the past decade, creating and sustaining hundreds of thousands of jobs.

Now the UK is the first major economy to establish in law that we will achieve net zero carbon emissions by 2050. This creates a significant opportunity to put the UK at the leading edge of innovation to meet its climate change commitments.

The Humber and the surrounding region is uniquely placed to lead this transition. The region is home to Britain’s biggest industrial economy employing 55,000 people. It has a rich heritage of industry, skills and trade. With the right support, the Humber can re-take its place on the world stage as a major global centre of industry and innovation.

This can only happen if we act now. Other regions around the world are planning and investing in low carbon infrastructure. By creating the conditions to become global leaders in clean industry they are seeking to win global investment and preserve and create new jobs. If nothing changes, the Humber – and UK as a whole – will lose more major industries putting jobs, skills and opportunities at risk, today and for future generations.

In 2019, the Zero Carbon Humber partnership was established by a group of leading energy businesses and organisations committed to transforming the region into the UK’s first ‘net zero’ carbon industrial cluster by 2040. This report sets out a roadmap for achieving this through the use of carbon capture and storage technology and hydrogen.

These ground-breaking technologies would enable industry to grow in the Humber while helping to meet the UK’s ambitious climate targets. It would also enable us to produce low carbon hydrogen at the scale needed to decarbonise industry, power, heat, transport and maritime across the North of England.

We can help Britain maintain its status as a world leader in low carbon technologies and achieve clean growth – creating new jobs and rebalancing the economy in the process.

Several businesses, industry groups and representatives from civil society are already behind this vision to decarbonise the Humber. The case is clear – we need to act now.

“The Humber can become the first zero carbon industrial cluster in the world. It can thrive again as a British industrial powerhouse”

Zero Carbon Humber Partnership

![]()

Will Gardiner

Chief Executive Officer, Drax Group

![]() Irene Rummelhoff,

Irene Rummelhoff,

Executive Vice President, Equinor

![]() Jon Butterworth,

Jon Butterworth,

Chief Operating Officer, National Grid Ventures

Lord Haskins of Selby,

Lord Haskins of Selby,

Chair, Humber Local Enterprise Partnership

![]()

David Talbot,

Chief Executive Officer, CATCH

Executive Summary

This report considers how the UK can decarbonise its major industrial hubs and explains why the Humber is the natural place for this to start.

It acknowledges the challenges many heavy industries face linked to climate change and highlights the technologies that will be needed to decarbonise.

It then examines how the Zero Carbon Humber partnership will work with others to harness these technologies to decarbonise the UK’s largest industrial cluster and act as a catalyst for other regions across the North of England to thrive into the future.

Click image to view/download the PDF report including references.

The roadmap to the Humber becoming carbon neutral would include:

- Developing a hydrogen demonstrator and test facility in the Humber;

- Installing carbon capture technology at Drax Power Station to create the world’s first carbon negative power station;

- Building a carbon dioxide (CO2) transport and storage system across the region that industry can connect to;

- Safely storing CO2 deep under the seabed in the Southern North Sea;

- Unlocking a cutting-edge hydrogen economy – providing a low carbon fuel to decarbonise industry, power, heat, transport and maritime across the North of England;

- Creating the conditions for new industries which use the CCUS pipeline or low carbon hydrogen to develop in the region – creating new jobs and opportunities locally and across the country.

Chapter One sets out the industrial challenge of climate change.

- The UK’s heavy industries have been in decline for decades. The journey to a net zero carbon economy represents both a challenge and an opportunity.

- The Humber contributes £18bn a year to Gross Value Added (GVA). It is home to the UK’s largest industrial cluster. It is also the UK’s most carbon intensive region.

- If businesses across the Humber fail to decarbonise, based on central HM Treasury forecasts they could face carbon taxes of up to £2.9bn a year by 2040 – putting their future at risk.

- Transitioning away from high carbon emissions to a more sustainable economy would allow the Humber to make a significant contribution to the UK meeting its climate goals.

Chapter Two highlights the technologies that will decarbonise industry.

- There is a broad consensus that CCUS and hydrogen will play a key role in ensuring the UK meets its climate goals. The Committee on Climate Change (CCC) says that CCUS is a necessity, not an option, for reaching net zero emissions.

- Bioenergy with carbon capture and storage (BECCS) can remove carbon dioxide from the atmosphere. The CCC has advised government it will play a crucial role in offsetting emissions from hard-to-decarbonise sectors in the future.

- Hydrogen will have a crucial role to play in decarbonising industry, power, heat and transport. Carbon capture technology would allow hydrogen to be produced at scale from natural gas with a low carbon footprint.

Chapter Three outlines the global race to help industries decarbonise.

- While the UK has been ranked in the top five countries for readiness to deploy CCUS, other countries are moving ahead with ambitious decarbonisation projects and are investing in clean infrastructure.

- Norway’s Northern Lights project is aiming to develop the world’s first storage facility that can receive CO2 from other countries.

- The PORTHOS initiative in the Port of Rotterdam would see the establishment of a CCUS industrial hub with CO2 stored in depleted gas fields offshore. The Netherlands is also developing the world’s first facility to generate 100% carbon free power using hydrogen as fuel.

- North America dominates the CCUS market and has the biggest number of large-scale CCUS facilities in the world – the majority of which are used to support Enhanced Oil Recovery.

Chapter Four outlines the Zero Carbon Humber project and the benefits it will deliver which include:

- Delivering the UK’s first low carbon cluster and the world’s first net zero carbon industrial cluster by 2040

- Accelerating progress to tackle climate change by capturing up to 53MtCO2 a year – that’s almost a third of the carbon savings which CCS needs to deliver for the UK to reach net zero by 2050.

- Helping protect 55,000 jobs, saving industrial businesses across the Humber £27.5bn in carbon taxes by 2040 and helping the region compete for investment and export opportunities around the world.

- Extending lives by improving air quality, saving £148mn in avoided public health costs between 2040 and 2050 by reducing industrial emissions across the Humber.

- Acting as a catalyst to accelerate the decarbonisation of other parts of the North of England.

Chapter 1

The industrial challenge of climate change

The UK has set an ambitious target to reduce greenhouse gas emissions by at least 100% by 2050. In doing so, it has led the world to take action to combat catastrophic climate change.

The challenge of meeting this target has been acknowledged by government and businesses, but the opportunities have not been fully explored.

The collective response to climate change cannot be one that makes us poorer and more divided. Achieving net zero should not be seen as a challenge to the way our country runs, but as an opportunity to build a more prosperous country supported by strong industries that sustain highly skilled and well-paid jobs.

For the UK’s industrial heartlands, the journey to net zero represents both an opportunity and a threat. Regions that have a long-term strategy to decarbonise stand to benefit from new jobs and investment. Those who do not risk missing out on the benefits of clean growth and seeing businesses offshore to low carbon hubs overseas.

This report focuses on the opportunity. It considers the technologies that can unlock a cleaner future for our major industries and outlines an ambitious plan in the Humber which will transform the fortunes of the region, set the foundations for other industrial clusters to build on and make a major contribution to the UK’s 2050 net zero target.

This ambition already enjoys broad political support. Nearly 70% of the British public are overwhelmingly in support of urgent political action to tackle climate change. UK businesses also recognise that their success depends on how quickly they can transition to green technologies.

But other countries are also transitioning away from high carbon emissions and building more sustainable economies. The UK cannot be complacent and risk falling behind as other countries benefit from the technologies of the future.

We have an opportunity to act. There is consensus from the public, politicians and business that the status quo is unsustainable and that a failure to reduce our carbon emissions will have catastrophic effects for future generations.

On 12 June 2019, the UK Government laid the draft Climate Change Act 2008 (2050 Target Amendment) Order 2019 to amend the Climate Change Act 2008 by introducing a target for at least a 100% reduction of greenhouse gas emissions (compared to 1990 levels) in the UK by 2050.

This is otherwise known as ‘net zero’.

This ambition already enjoys broad political support. Nearly 70% of the British public are overwhelmingly in support of urgent political action to tackle climate change. UK businesses also recognise that their success depends on how quickly they can transition to green technologies.

But other countries are also transitioning away from high carbon emissions and building more sustainable economies. The UK cannot be complacent and risk falling behind as other countries benefit from the technologies of the future.

We have an opportunity to act. There is consensus from the public, politicians and business that the status quo is unsustainable and that a failure to reduce our carbon emissions will have catastrophic effects for future generations.

“We need to refocus the lens through which we see net zero. Rather than treating it as a trial, we need to see it as an opportunity. We should seize the chance to carve out a niche for Britain and exploit our existing advantages to become a world leader in cutting-edge environmental technology.”

Sir John Armitt, Chair of the National Infrastructure Commission, July 2019

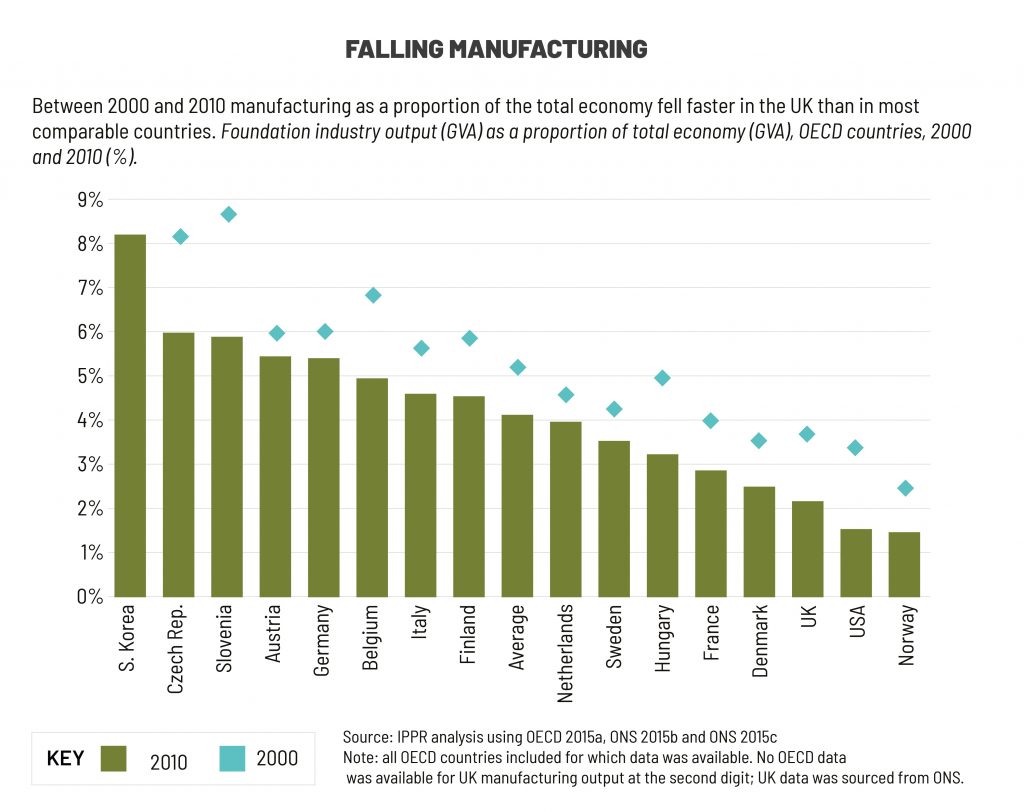

1.1 UK industry is in decline

The UK’s manufacturing industry is still the ninth largest in the world, despite the decline since the 1970s when the sector contributed 25% of GDP. Today it employs 2.7 million people, produces 10% of national economic output and delivers 45% of UK exports totalling £273bn.

Manufacturing remains central to the success of the UK economy. For every £1mn that the manufacturing sector contributes to UK GDP itself, a further £1.5mn is supported across the wider economy through indirect and induced macroeconomic effects.

However, UK manufacturing faces several challenges, not least increasing international competition. Since 2000, manufacturing has fallen faster as a proportion of the total UK economy than it has in any other developed economy.

“The UK has one of the smallest foundation industry sectors relative to GDP in the Organisation for Economic Co-operation and Development (OECD). Since 2000 its share of GDP has shrunk by 43%, compared to an average decline across the OECD of 21%.”

Institute for Public Policy Research, Strong Foundation Industries, 2016

Energy intensive industries in particular have faced many pressures since the 2008 financial crisis. In steel production, the fragility of the industry has been brought into focus by the situation facing British Steel in Scunthorpe, which is increasingly facing stiff international competition. Ambitious climate targets also mean that, without any investment in decarbonisation technology, regions that are reliant on heavy industry risk being hit the hardest.

“This is not a time to be too cautious, as UK steelmakers face an uncertain business environment. The Government needs to move swiftly to secure a bright future for the sector while addressing the elements which undermine our competitiveness.”

Gareth Stace, UK Steel Director General, 2019

This decline of heavy industry matters. Without a diverse range of sectors in the economy, the UK is at risk of overexposure to downturns in certain industries.

The level of exports – measured in volume or value terms – is an indicator of a country’s ability to remain globally competitive.

In the period between May 2018 and May 2019, exports of goods produced by the manufacturing sector in the UK totalled £273bn, accounting for 44% of total UK exports. It is clear that industry remains of critical importance to UK exports. The UK’s global competitiveness and standing as one of the world’s largest economies is ultimately at risk if the decline continues.

A continued decline in UK industry will have significant implications for highly skilled, well paid and secure employment, directly through manufacturing companies and indirectly through their supply chains. Many jobs in heavy industry command higher than average salaries and more secure terms and conditions, which are increasingly rare as the proportion of those in self-employment and/or insecure work increases.

“Trade unions stand ready to do our part. Workers who are at the forefront of dealing with the challenges of climate change must have a central voice in plans. A quick and successful transition will need agreements with unions to retrain people with jobs at risk for new work in low carbon industry with good pay and conditions.”

Frances O’ Grady, General Secretary, TUC

Any decline in manufacturing also risks deepening inequality between the North and South of England. The concentration of manufacturing industries in the North, opposed to service sector industries in the South, means that the North is at the mercy of lower levels of growth in manufacturing. For example, while the manufacturing industries were only expected to grow by 1% between 2017 and 2020, the communications and professional services sector was expected to grow by over 3%. A lack of investment in manufacturing in the North and a decline in the sector would exacerbate regional inequality.

1.2 The Humber – The UK’s largest industrial region

Energy intensive industries make a significant contribution to the UK economy. Together these industries and their supply chains are worth £52bn, support 600,000 jobs and account for 4% of the UK’s GVA. They produce products that are essential to the UK’s low carbon economy; from steel and lightweight composites for wind turbines and electric cars, to glass, ceramics and advanced insulating materials for low-energy housing.

The Humber has a rich industrial heritage, hosting the steel industry, oil refineries, cement manufacturers, petrochemical producers and chemical manufacturers. It contributes £18bn each year to UK GVA – a quarter of which is related to manufacturing – and heavy industry provides the mainstay of employment in the region with 55,000 working in the manufacturing sector alone.

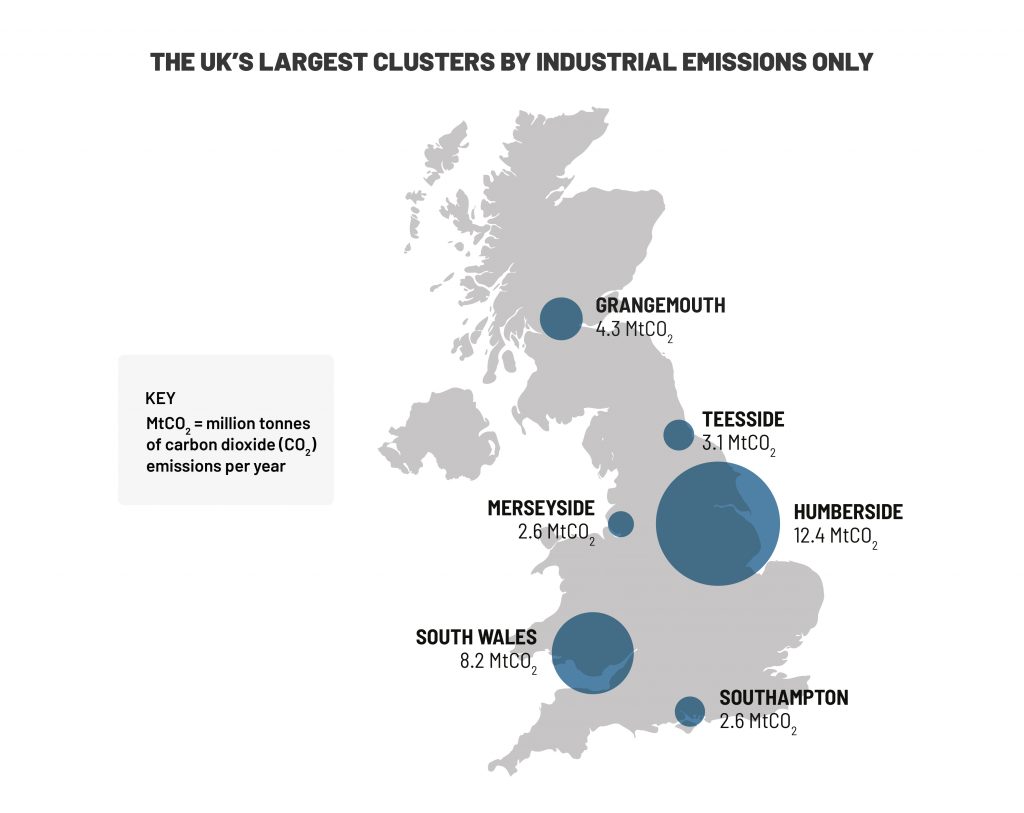

But UK industry also accounts for around 25% of all greenhouse gas emissions in the UK. Two thirds of these emissions come from energy intensive industries which are often located next to each other in clusters.

In the Humber, the high concentration of heavy industry means that 6% of England’s industrial and commercial energy use is by businesses in the region. The Humber’s industrial cluster currently emits more CO2 than any other UK cluster (30% more than South Wales, the next largest),xviii and is the most energy intensive region in the UK.

1.3 The cost of failing to decarbonise

Carbon pricing is designed to encourage businesses to reduce carbon emissions and fund decarbonisation programmes by taxing fossil fuels. It is regarded as one of most effective ways for countries to reduce their emissions and has been instrumental in phasing Britain’s coal- fired power stations off the system. The UK government expects carbon pricing to increase significantly over the coming decades. Based on current forecasts, industrial businesses across the Humber could face a carbon tax bill of between £1.4bn and £4.3bn in 2040, if they fail to decarbonise. This would inevitably place greater pressure on businesses in the Humber – putting jobs and supply chains at risk and eroding the region’s ability to attract new businesses and increasing the risk of carbon leakage, where carbon emissions are simply moved offshore rather than reduced.

As a result, there is increasing urgency for action from both industry and government to safeguard these clusters. With the right regulatory framework, energy intensive industries could start to harness new technologies to ensure they have a sustainable and prosperous future, help fight climate change and enable them to compete on the world stage. Carbon capture usage and storage and hydrogen are two technologies that will play a crucial role in this transition.

Chapter 2:

Carbon capture usage and storage (CCUS) and hydrogen can decarbonise industry

2.1 CCUS is a critical part of protecting the future for UK industry

The Intergovernmental Panel on Climate Change (IPCC) has highlighted that achieving the ambitions of the Paris Agreement to limit future temperature increases to 1.5 degrees will require more than just increased efforts to reduce emissions; it will also require the deployment of technologies to actually remove carbon from the atmosphere.

CCUS is the process of capturing carbon dioxide emissions created by energy and industry, which are then either permanently stored or used in industry. It prevents CO2 from entering the atmosphere and contributing to global warming. Possible storage sites include saline aquifers or depleted oil and gas reservoirs, putting carbon emissions back in the ground.

Deploying CCUS is essential for decarbonising existing energy and industrial processes. New industries are also expected to emerge which will be able to use the captured carbon, creating other options to keep it out of the atmosphere.

No single technology alone can manage the adverse effects of climate change. Yet there is broad international consensus that CCUS technologies will play a critical role in meeting the UK’s – and the world’s – energy and climate goals. The vital role of CCUS was reaffirmed by the Committee on Climate Change (CCC), Net Zero: The UK’s contribution to stopping global warming report.

“CCS is a necessity not an option for reaching net zero GHG (greenhouse gas) emissions”.

By helping to decarbonise industry, generate low carbon power and enable the production of hydrogen at scale, CCUS offers significant new opportunities for the UK – on a national and international scale. It will also help the UK become a global leader in tackling climate change.

CCUS can also deliver considerable socio- economic benefits by helping to create new jobs, improve quality of life, reduce energy costs for families and businesses, and support the economic viability of the UK’s most heavily industrial clusters.

For these reasons the momentum behind CCUS in the UK is building. In 2018, the Government committed to having the first CCUS facility up and running by the mid-2020s. The CCC and Business, Energy and Industrial Strategy Select Committee, a cross-party grouping of MPs, have argued we should be developing CCUS in multiple industrial clusters across the country.

2.2 Bioenergy with CCUS creates the opportunity to remove carbon from the atmosphere

There are different types of carbon capture technologies.

Bioenergy with carbon capture usage and storage (BECCS) is recognised as one of the most important because it doesn’t simply prevent carbon emissions being produced – it also removes carbon from the atmosphere.

The CCC’s Net Zero report identified BECCS, “as one of the required key near-term actions that are on a ‘critical path’ towards the UK achieving net zero emissions by 2050”.

The Government’s Clean Growth Strategy references BECCS as one of several greenhouse gas removal technologies that could remove emissions from the atmosphere and help achieve long term decarbonisation. A joint report by The Royal Academy of Engineering and Royal Society has estimated that BECCS could enable the UK to capture 50 million tonnes of CO2 per year by 2050 – removing almost half of the emissions predicted to remain in the economy.

2.3 Hydrogen can help decarbonise power, industry, homes, businesses and transport

While the power sector has enjoyed significant growth in renewables in recent years, decarbonising industry, transport and agriculture remains a challenge.

Hydrogen will be part of the solution. It can be burned to deliver heat in industrial processes, to heat buildings and to fuel heavy transport. It can also be used in power and can be stored like natural gas.

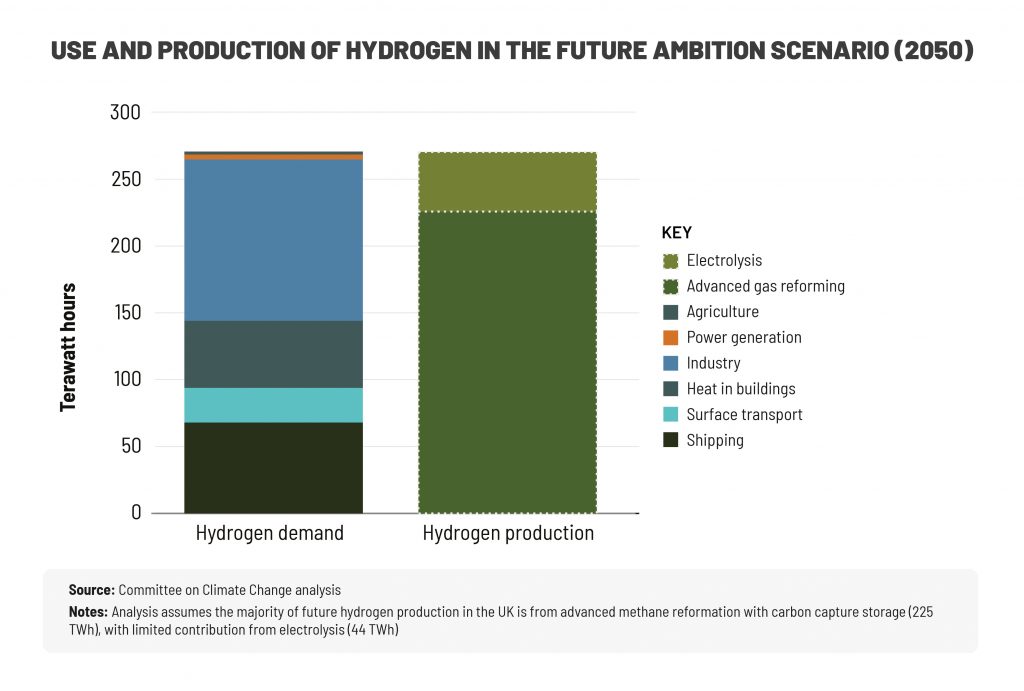

The CCC states that to reach net zero emissions by 2050, the UK will need new hydrogen production capacity that is comparable to the UK’s current fleet of gas-fired power stations.

However, creating hydrogen from natural gas generates carbon emissions. That is why large- scale production of hydrogen will need to be combined with CCUS technology in the future. When available, surplus renewable energy should also be harnessed to create ‘green’ hydrogen, via electrolysis of water, which can share the same infrastructure as hydrogen from natural gas.

CCUS has the potential to kick start new hydrogen technology and help create new industries, jobs, and the opportunity to decarbonise industry, power, heat, transport and maritime across the North of England.

Other countries are also looking at this technology. In the International Energy Agency (IEA) report, The Future of Hydrogen: Seizing Today’s Opportunities, launched at the G20 meeting in June 2019, energy and environment ministers offered several recommendations to help governments, companies and other stakeholders to scale up hydrogen projects around the world.

Its recommendations included four specific areas where immediate action could help lay the foundations for the growth of a global clean hydrogen industry:

- Make industrial ports the nerve centres for scaling up the use of clean hydrogen;

- Build on existing infrastructure, such as natural gas pipelines;

- Expand the use of hydrogen in transport by using it to power cars, trucks and buses that run on key routes;

- Launch the hydrogen trade’s first international shipping routes.

“Hydrogen is today enjoying unprecedented momentum, driven by governments that both import and export energy, as well as the renewables industry, electricity and gas utilities, automakers, oil and gas companies, major technology firms and big cities. The world should not miss this unique chance to make hydrogen an important part of our clean and secure energy future.”

Dr Faith Birol, Executive Director at the IEA

Chapter 3:

The UK is competing to be a global leader in industrial decarbonisation

Governments around the world are investing in clean infrastructure to attract businesses and allow them to operate without damaging the environment or people’s health – saving money and making their operations sustainable over the long-term. This includes efforts to prepare to deploy CCUS (carbon capture, usage and storage) and hydrogen infrastructure.

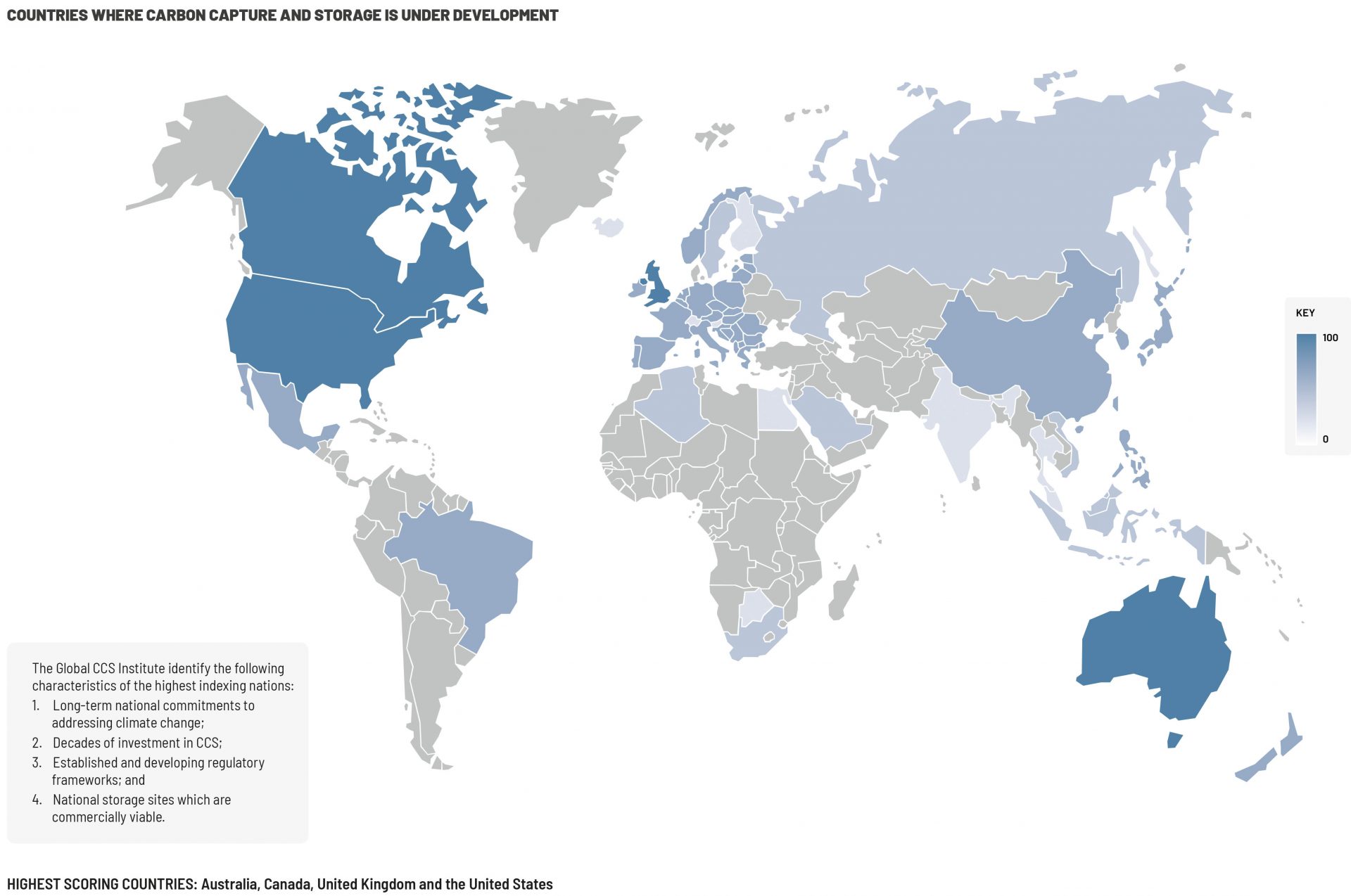

In a global assessment of countries which are leaders, “in the creation of an enabling environment for the commercial deployment of CCS”, the Global CCS Institute rated the UK as one of the five top scoring nations for “readiness” (alongside Australia, Canada, Norway and the United States). This is attributed to the supportive policy frameworks, comprehensive regulatory and legal frameworks, and detailed storage assessments.

Although the assessment is encouraging for the UK’s goal of reaching net zero emissions by 2050, the report found that no nation – including the top five – has established the necessary conditions to drive CCUS deployment at the rate required to meet current climate ambitions. The global competition for capitalising on investment for emissions reductions, jobs and the trickle-down economic benefits for regions and nations should not, and must not, be taken as a given for the UK.

While the foundations are strong for the UK to utilise its strategic comparative advantage in industry, other countries such as Norway, the Netherlands and the United States are also investing significant amounts in developing CCUS technology.

The next phase of CCUS calls for a strong commitment and action between government, industry and business. Other countries are preparing to deploy CCUS at scale and the UK must not be left behind.

3.1 Norway: Looking to the Northern Lights

In Norway, the Northern Lights, a CCUS project initiated by Equinor with partners Shell and Total, aims to develop the world’s first storage facility capable of receiving CO2 from various industrial sources.

The project consists of a CO2 receiving terminal, an offshore pipeline, injection and CO2 storage. The first phase of this CO2 project could reach a capacity of approximately 1.5 MtCO2 per year.

The project will be designed to accommodate additional CO2 volumes aiming to stimulate new commercial carbon capture projects in Norway, Europe and across the world. In this way, the project has the potential to be the first storage project site in the world receiving CO2 from industrial sources in several countries.

An investment decision for the Norwegian full- scale carbon capture and storage project is expected in 2020/2021.

“The idea is to capture CO2 from significant emission sources on land, transport it by ship to a terminal northwest of Bergen, transport it by pipeline out to the North Sea, and then inject it 3,000 metres beneath the seabed, where it will be stored… This is a solution for many

Sverre Overå, Project Director Northern Lights, Equinor

industries wanting to reduce emissions, but who have no way of storing their CO2 . This will truly be full-scale CCS.”

Rotterdam Netherlands city and harbour.

3.2 The Netherlands: CCUS & Hydrogen

Port of Rotterdam CCUS Backbone Initiative (‘PORTHOS’)

The Netherlands has set clear climate targets. By 2030, it plans to have reduced its greenhouse emissions by 49% compared to 1990 levels, and 95% by 2050. The focus for industrial decarbonisation centres on plans for CCUS from the Port of Rotterdam.

A consortium comprising of the Port of Rotterdam Authority, Nederlandse Gasunie (Gasunie) and Energie Beheer Nederland (EBN), is developing the business case for the deployment of CCUS infrastructure for the establishment of an industrial CCUS hub connecting industry, via the port, to offshore depleted gas fields in the North Sea.

A feasibility study on the large-scale deployment of CCUS in the Port of Rotterdam found that CO2 capture, transport and storage under the North Sea is technically feasible, and a cost-effective measure for radically reducing carbon emissions.

The concept is based on a collective pipeline of approximately 33km that runs through Rotterdam’s port area.

The pipeline will serve as a basic infrastructure for various industrial parties to connect to in order to dispose of CO2 captured at their facilities. The business partnership is working towards investment decisions in 2020. The ambition is to store 2 million tonnes of CO2 per year from 2020 to a capacity that will run up to 5 million tonnes per year by 2030.

Hydrogen Conversion at Nuon Magnum Power Plant, Eemshaven

A hydrogen conversion project (led by a consortium between Nuon, Gasunie and Equinor) is currently underway at Nuon Magnum power plant to convert one of its units to run on hydrogen by 2023. If successful, the plant would be the world’s first power station to use 100% hydrogen as a fuel. Equinor is responsible for hydrogen production by converting the Norwegian natural gas into hydrogen and CO2, while Gasunie is engaged in research for the transportation and storage of hydrogen at the power station.

The CO2 released during the hydrogen production process is planned to be stored in underground facilities off the Norwegian coast. Nuon’s long-term vision is to locally produce hydrogen through the electrolysis process by splitting water into oxygen and hydrogen. The electricity required for the electrolysis will be sourced from renewable sources.

3.3 The United States (1): Carbon Capture secures bi-partisan backing

According to the Global CCS Institute, the United States has and continues to dominate the CCUS market at the global level. Cross-party support secured federal legislation (‘the FUTURE Act, 2018’) that paved the way for tax credits for capture and storage of emissions.xliv At state level, California, Texas, North Dakota and Montana are all taking steps to secure a policy and regulatory environment that is conducive to securing investment.

The policy landscape goes some way to understanding how and why the United States hosts the highest number of large-scale CCUS facilities in the world. Of the 18 facilities operating worldwide, 10 are in the United States; where the cumulative carbon capture and storage for operational facilities equates to 150 million tonnes.

“It is fair to say that the US continues to dominate the CCS space. And over the past year, deployment and policy have picked up pace. Together, US facilities can capture about 25 million tonnes per annum – the equivalent of taking almost

The Global Status of CCS report, Global CCS Institute, 2018

5.4 million cars off the road for one year.”

3.4 The United States (2): CCUS driving tech innovation in Texas

Net Power, a US energy company, is behind a project to produce low-cost electricity from natural gas with zero emissions released into the atmosphere.

The company, partly-owned by Exelon Generation, has built a $150mn commercial- scale 50 MWth power plant and test facility in Texas. The plant uses an innovative technology called ‘The Allam Cycle’ to burn fossil fuels with oxygen instead of air to generate electricity without emitting any CO2. This process allows much of the CO2 released during combustion to be re-used.

If successful, the CO2 produced will create a ‘pipeline ready’ product which will be permanently sequestered or can be sold for use in other industrial purposes. NET Power’s aim is the global deployment of 300 MW e-class commercial-scale plants beginning as early as 2021.

Chapter 4:

Creating A Zero Carbon Humber

Our plan will:

- Help the UK achieve net zero by providing almost a third of the carbon savings that CCUS needs to deliver by 2050;

- Help protect 55,000 jobs by saving industrial businesses across the Humber £27.5bn in carbon taxes by 2040;

- Extend lives by improving air quality across the region, saving £148m in avoided public health costs between 2040 and 2050;

- Make the Humber region a world leader by attracting new investment, industries and jobs;

- Support the decarbonisation of West Yorkshire, Teesside and the wider North of England.

Our Mission

Established in summer 2019, the Zero Carbon Humber partnership shares the same objective: to deliver the UK’s first zero carbon industrial cluster by 2040.

To achieve this, we will work together to deliver a number of pioneering decarbonisation projects that will protect jobs, help the region compete for investment in clean technologies and accelerate progress towards the UK’s 2050 climate targets. It will also improve air quality and the local environment.

This plan has the backing of some of the world’s biggest industrial businesses and would safeguard the region’s role at the heart of the UK economy for decades to come.

“Demonstrating climate action and growing the economy go hand in hand in building momentum behind global action on carbon. The UK is a leader in both, cutting our emissions by more than 40% while growing our economy by two thirds, but to sustain this track record we need to tackle emissions from energy intensive sectors and bring clean growth to our great industrial centres.”

Claire Perry, COP26 President and former Energy and Clean Growth Minister. 2018

4.2 Our Plan

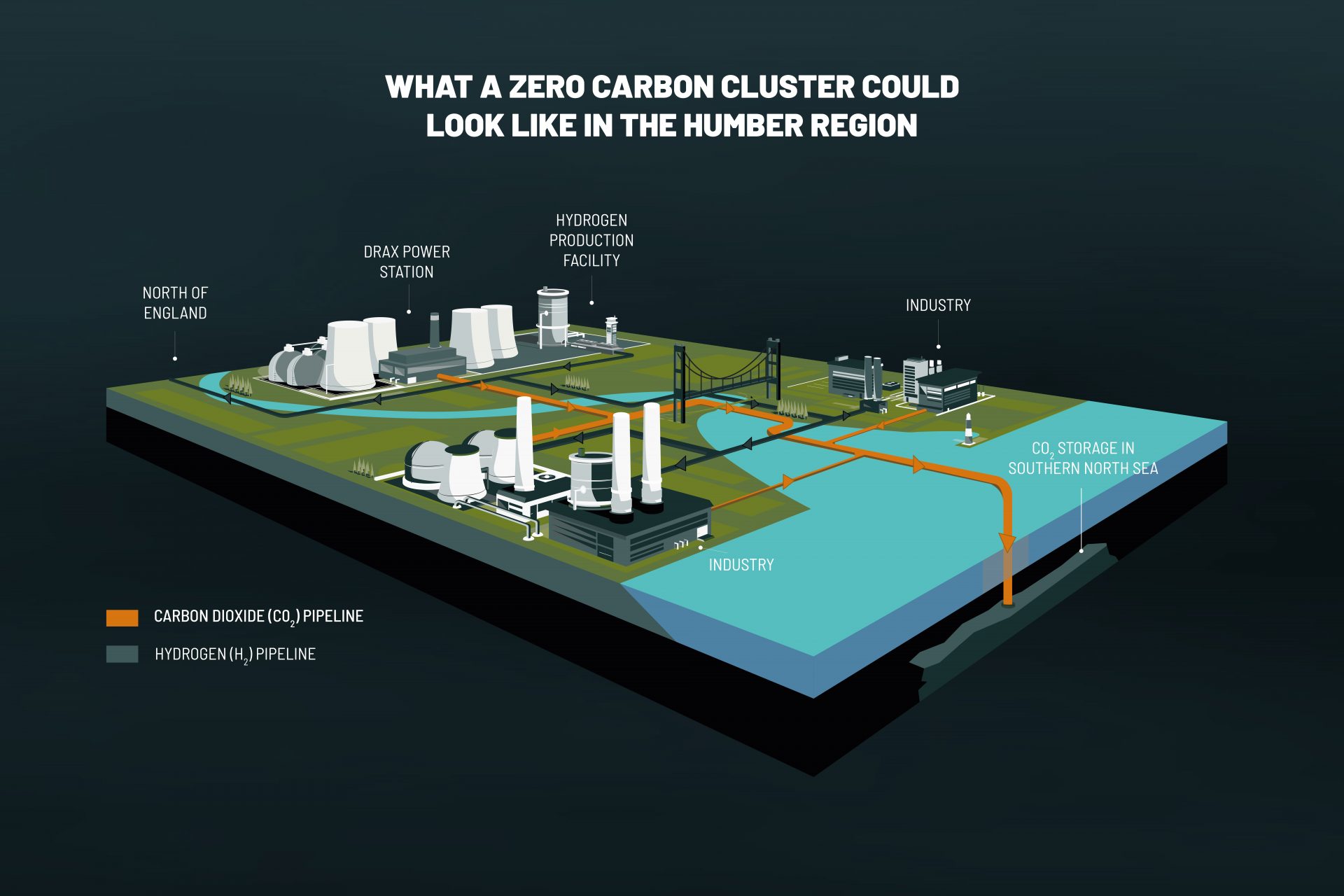

The partnership is based around three strategic pillars, which together will deliver the UK’s first net zero carbon industrial cluster.

- Unlocking a cutting-edge hydrogen

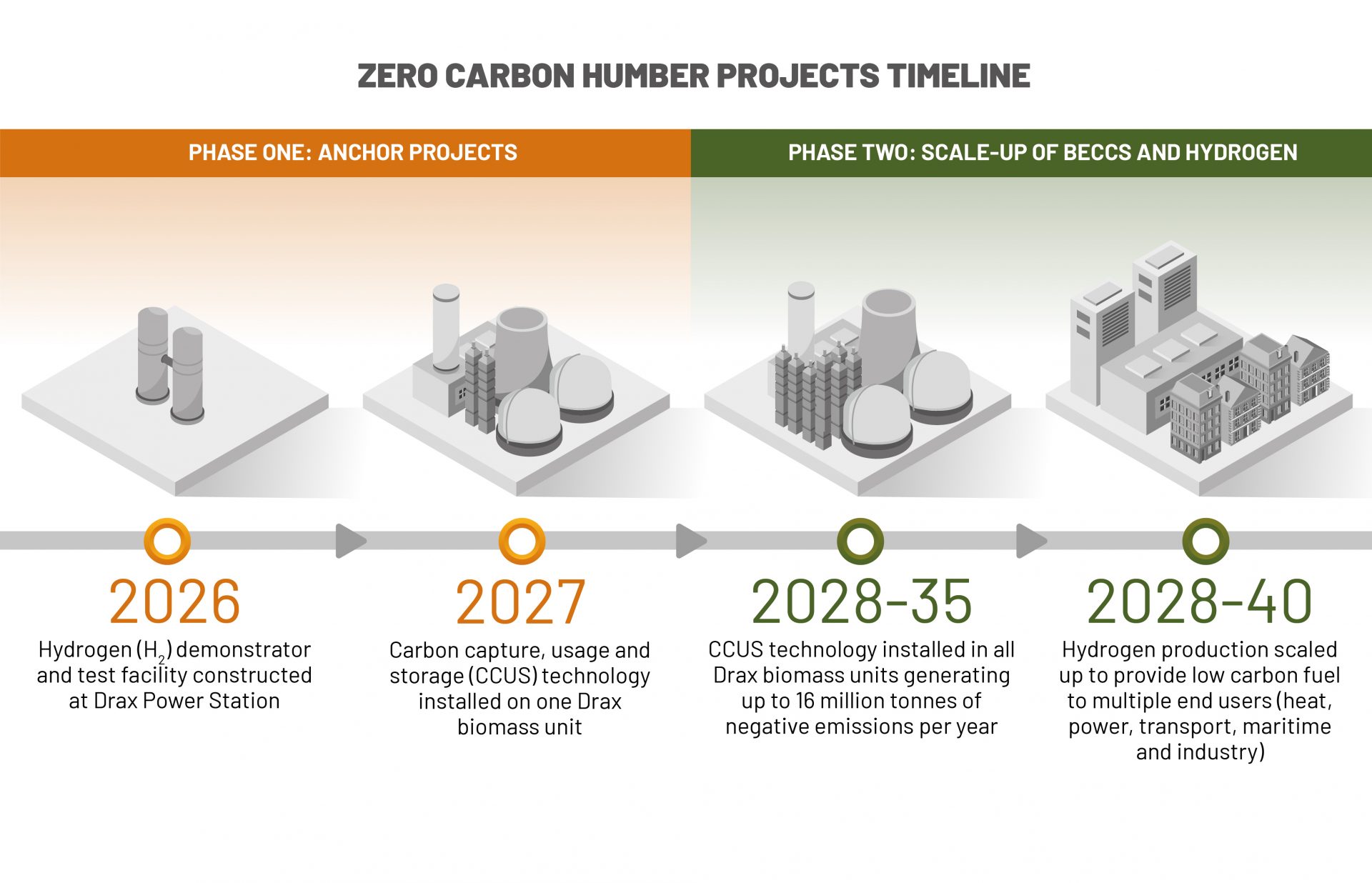

Building a hydrogen demonstrator and test facility in the Humber by the mid-2020s would create the foundation for unlocking a new hydrogen economy in the region.

Over time, this facility could be scaled up to produce a low carbon fuel that could be used to decarbonise industry, power, heat, transport and maritime across the North of England.

- Creating negative emissions at scale

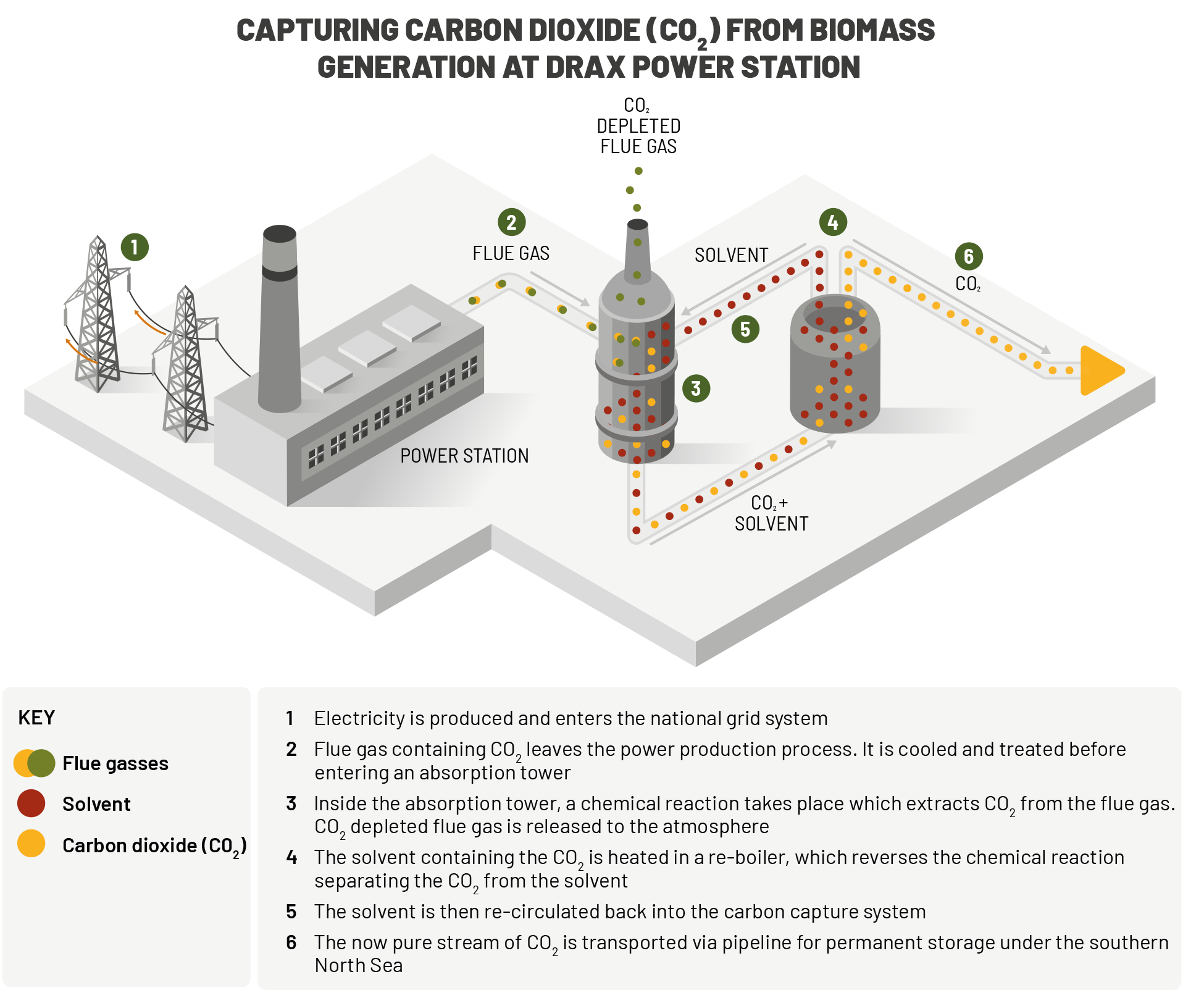

Installing carbon capture technology on Drax Power Station’s biomass units could turn it into the world’s first carbon negative power station by 2027, generating clean electricity and negative emissions at the same time.

Over time, Drax Power Station’s negative emissions could help to offset the emissions of other industries in the region who fail to decarbonise.

- Establishing a regional carbon dioxide transport and storage network

With the right infrastructure in place, businesses across the region could safely transport and store their emissions under the Southern North Sea instead of releasing them into the atmosphere.

This would help the battle against climate change and establish the Humber industrial cluster as a world leader, creating new jobs and investment opportunities in the region.

4.3 The Humber as a catalyst for wider decarbonisation

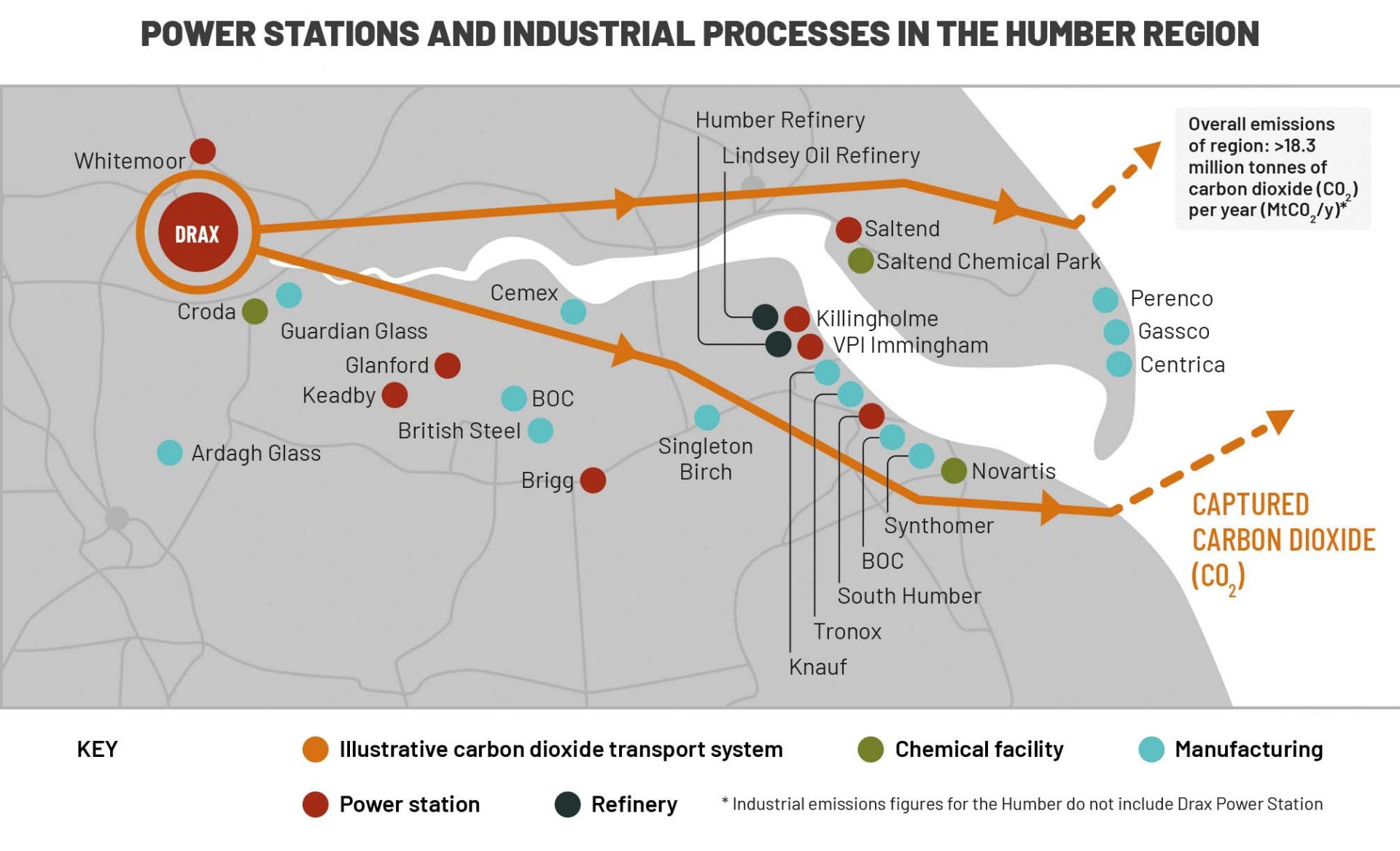

Power stations and industrial processes in the Humber region

The Humber is the natural place to deploy CCUS and hydrogen technology. It is one of the most important industrial economies in the country. It is also the most carbon intensive, which means that decarbonising the region will make a significant contribution to meeting the government’s climate targets.

The location of the Humber means it can also unlock other decarbonisation projects planned in the North of England.

Off the coast of the Humber is a number of large geological storage sites – either saline aquifers or depleted oil and gas fields – in the southern North Sea, that could be used to safely store CO2 under the ground for hundreds of years. For example, from 2011 to 2015 tens of millions of pounds of public and private money was spent exploring how carbon dioxide could be stored in a saline aquifer known as ‘Endurance’.

These storage sites could be used not only to store CO2 from the Humber, but also support other industrial clusters such as Teesside, which is also developing its own CCUS plans.

Having multiple clusters share the same offshore CO2 infrastructure would help accelerate construction, produce economies of scale and bring down costs for all users.

Meanwhile to the west of the Humber is a number of city regions such as York, Leeds and Bradford, represented by the West Yorkshire Combined Authority. A significant amount of work has already been undertaken by Northern Gas Networks, through the H21 North of England project, to explore how 3.7 million UK homes and businesses could switch from natural gas to low carbon hydrogen.

Developing hydrogen production capability in the Humber would not only enable the decarbonisation of power, heat, industry and transport in the Humber itself – it could also supply the hydrogen required to make the H21 project a reality.

Case Study: Making Saltend Chemicals Park CCUS-Ready

Industrial businesses across the Humber are already thinking about CCUS and hydrogen.

Saltend Chemicals Park is home to a cluster of world-class chemicals and energy businesses, including Air Products, BP, Ineos and Nippon Gohsei. The site was acquired in 2018 by px group, which have since invested several millions to develop and extend the park.

The businesses operating on the 370-acre site share infrastructure and a range of services including feedstocks and utilities. As a result, the park is an optimal location for the deployment of carbon capture, usage and storage technology.

“We have already had significant interest from prospective tenants in our plans to become CCUS ready. If industry and government could work together to bring CCUS technology to Saltend Chemicals Park, it would reinforce its status as an international destination for manufacturing and chemical industries and bring new businesses into the Humber.”

Jay Brooks, Site Director of Industrial Parks at px group

Case Study: Decarbonising Jet Fuel Production

Velocys is a sustainable fuels technology company and project developer. Supported by British Airways and Shell, the company has submitted a planning application for Europe’s first waste-to-jet fuel plant in Immingham.

The proposed plant will take hundreds of thousands of tonnes of household and commercial solid “black bag” waste and turn it into cleaner burning sustainable aviation fuel, reducing net greenhouse gases by 70% compared to the fossil fuel equivalent.

Following a recently announced agreement with US oil company Oxy, their US waste-to-fuels facility will capture CO2 emitted from the process and securely store it underground, meaning it will produce negative emission fuels.

“We don’t just want to deal with waste materials and produce cleaner burning fuels – we want the process that produces the clean fuels to be as sustainable as possible as well. Our carbon negative solution could be replicated at our proposed UK facility in Immingham, subject to UK Government support for CCUS deployment and the availability of transportation and storage infrastructure in the Humber region.”

Henrik Wareborn, Chief Executive of Velocys

4.4 The Benefits of a Zero Carbon Humber

Cutting Carbon Emissions

The roadmap outlined by the Zero Carbon Humber partnership will make a major contribution to cutting carbon emissions in the UK’s largest industrial cluster. New research commissioned by the Zero Carbon Humber Partnership has for the first time identified the scale of the emissions reductions that it will deliver.

The analysis by Element Energy is based on:

- The development of new hydrogen production facilities in the Humber, starting with a hydrogen demonstrator in the 2020s and scaling up in subsequent years..

- The installation of CCUS technology on all four of Drax Power Station’s biomass units, turning it into the world’s first carbon negative power station.

- The creation of large-scale CO2 transport and storage infrastructure in the Humber, used by industrial businesses in the region.

- The widespread use of hydrogen in the region in a number of different sectors including power, heating, industry and transport.

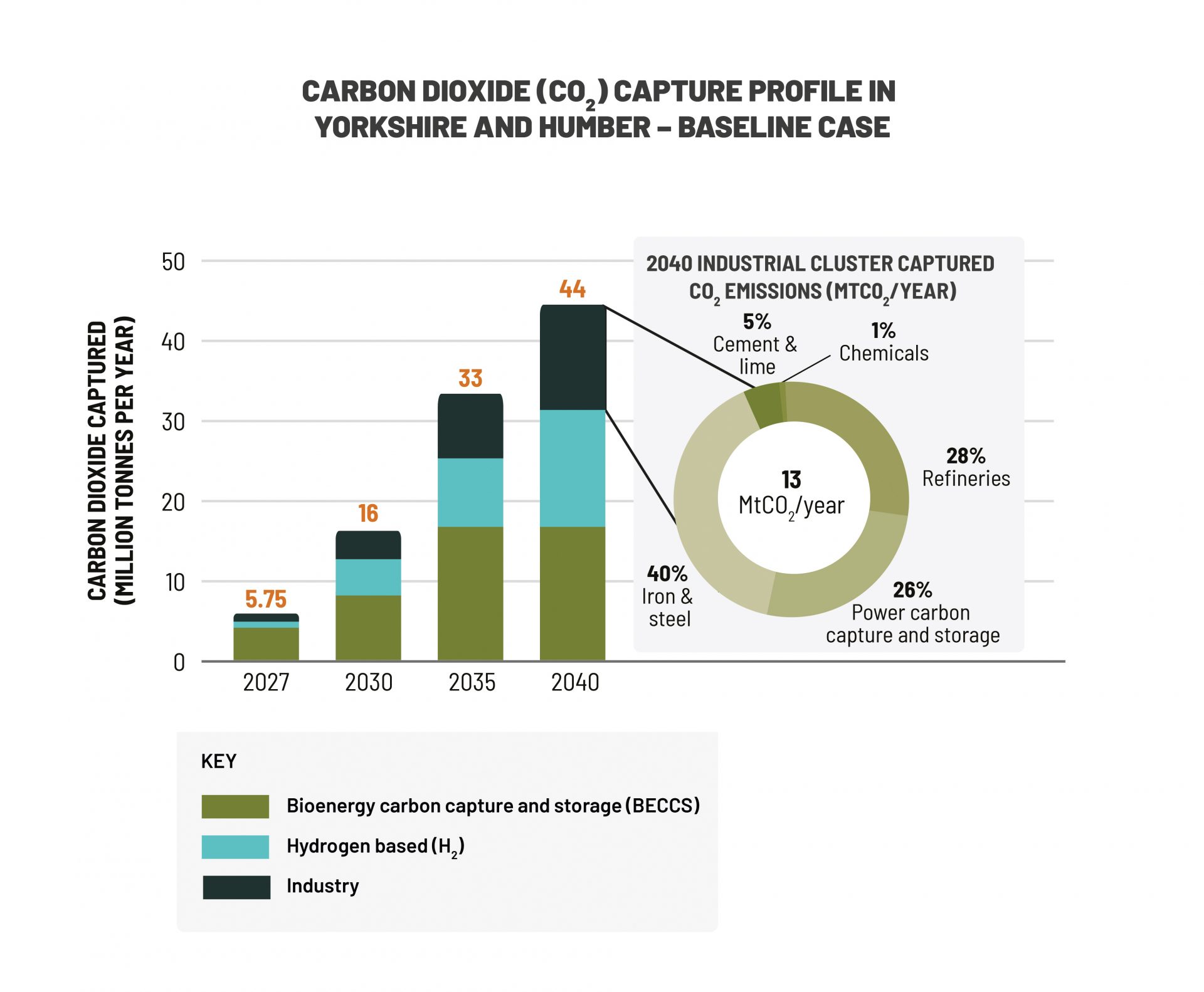

The projections show that by 2040 the project has the potential to capture up to 44 MtCO2 per year. To put that into context, that’s around 15% of the UK’s current annual CO2 emissions.

It’s also 30% of the total CO2 that the Committee on Climate Change says needs to be removed by CCUS by 2050 if the UK is meet the net zero target.

How the emissions stack up

The analysis assumes that between 2027 and 2035 each of Drax’s biomass units will be fitted with CCUS technology. Those four units will provide 2.4GWs of clean electricity capacity on the system, as well as generating up to 16 million tonnes of negative emissions ever year.

It also considers that the availability of infrastructure to transport CO2 offshore will encourage the decarbonisation of other power stations in the region, with at least one gas-fired plant fitted with CCUS technology.

In Element Energy’s analysis at least 10 industries switch to hydrogen as their main fuel supply. But certain industrial sites, due to their large emissions outputs and difficulty to decarbonise, will require direct capturing of emissions by connecting to the CO2 transport and storage infrastructure.

Over 9 MtCO2 from at least four industrial sectors will be captured and stored in 2040, based on scenarios as follows:

- Decarbonising the cement and lime industry in the Yorkshire and Humber region, with a total of 65 MtCO2 per year being captured in 2040.

- CCUS will enable Humber area refineries to abate ~3.6 MtCO2 per year annually by

- Iron and steel sectors from the Humber area are decarbonised using CCUS, with 2 MtCO2 per year being captured in 2040.

- Chemicals are manufactured by various high-heat processes, including the cracking of hydrocarbons, and usually require burning fossil fuels. Due to the difficulty of separating carbon emissions from other gases in the exhaust, CCUS is considered a feasible decarbonisation approach.

The Humber industrial sites will be able to capture ~13 MtCO2 per year in 2040, representing 24.5% of the total 44 MtCO2 per year captured from the whole area in 2040.

Cost Savings

Carbon taxation has played a key role in the decline of fossil fuel power generation and the rise of renewables. But the ‘polluter pays’ principle has also proved challenging for many industries which suffer from low margins and volatile energy prices.

Industry accounts for around a quarter of all UK greenhouse gas emissions, with more than two thirds of these emissions coming from a small number of energy intensive industries.

CCUS technology provides a route to curtailing carbon emissions and avoiding the cost of carbon pricing. There will be billions of pounds worth of savings for the firms who utilise the transport and storage infrastructure – savings which will have major implications for their competitiveness in the decades to come.

Based on HM Treasury’s central forecast for future carbon pricing, we can estimate the additional cost that businesses in the region would be facing without the Zero Carbon Humber roadmap.

By 2040 firms in the region could have saved:

- £2.9bn per annum by capturing and storing rather than releasing their

- A total of £27.5bn since the infrastructure for transporting and storing CO2 came into effect.

That annual figure could reach £4.2bn per year by 2050.*

Those cost savings are just a part of the wider economic benefits that the project will bring to the region. This includes as many as 55,000 manufacturing jobs secured across sectors from cement, steel, refineries and chemicals.

It will also put the region on the global stage and open up opportunities for inward investment and for exports of green technology.

Air Quality

The new hydrogen production facility will be a catalyst for the growth of a new hydrogen economy. A pipeline will transport the carbon emissions from the facility, along with those from Drax’s biomass units, to be stored safely offshore.

Hydrogen is expected to play an important role in decarbonising heat and fuelling flexible power generation. It could also make a significant contribution to improving air quality by shifting consumers from transport using higher- emission fuels to hydrogen and other ultra-low emission alternatives.

The uptake of hydrogen mobility, with over one million hydrogen vehicles deployed by 2050, could lead to a reduction in hazardous emissions, including nitrogen oxides (NOx) and particulate matter (PM) which are linked to several long-term medical conditions and premature deaths. Their impacts are often quantified in terms of social damage costs.

The analysis by Element Energy found that in total £148mn in public health costs could be saved between 2040 and 2050, reducing the burden on public health services.

It also estimates that by 2050:

- 2 MtCO2 emissions would be avoided by the uptake of hydrogen transport in the region.

- 2,100 tonnes of NOx and 11 tonnes of PM (estimated as 34% and 3% respectively of the region’s 2050 road transport emissions) could also be avoided.

*Estimates based on combined avoided carbon taxation payments for industrial and power sectors in the Humber, using central carbon pricing forecast in HM Treasury’s Green Book. Figures do not include payments to CO2 transport and storage operator.

Conclusion

The Government’s 2050 net zero target may seem a long way in the future. But if we are to achieve our climate goals the time to act is now.

Decarbonisation doesn’t have to be a choice between saving our industries and saving the planet. With this plan we can do both.

With the right engagement and support from Government we can ensure that the UK’s most important industrial region continues to thrive.

We can safeguard 55,000 manufacturing jobs.

We can create a new hydrogen-based economy that will clean up the vehicles that we drive and the air that we breath. We can become a world leader in the use of sustainable bioenergy to create negative emissions.

The Humber is uniquely placed to seize this opportunity to become the first zero carbon economy in the world.

It can be a catalyst for other industrial regions too.

And it will help the UK take the lead in exporting the green technologies that will be needed around the world.

Full report including references

Click image to view/download the PDF report.

Learn more about carbon capture, usage and storage in our series:

- Planting, sinking, extracting – some of the ways to absorb carbon from the atmosphere

- From capture methods to storage and use across three continents, these companies are showing promising results for CCUS

- Why experts think bioenergy with carbon capture and storage will be an essential part of the energy system

- The science of safely and permanently putting carbon in the ground

- The numbers must add up to enable negative emissions in a zero carbon future, says Drax Group CEO Will Gardiner.

- The power industry is leading the charge in carbon capture and storage but where else could the technology make a difference to global emissions?

- From NASA to carbon capture, chemical reactions could have a big future in electricity

- Can we tackle two global challenges with one solution: turning captured carbon into fish food?

- How algae, paper and cement could all have a role in a future of negative emissions

- How the UK can achieve net zero

- Transforming emissions from pollutants to products

- Drax CEO addresses Powering Past Coal Alliance event in Madrid, unveiling our ambition to play a major role in fighting the climate crisis by becoming the world’s first carbon negative company

Glossary

BEIS

Business, Energy and Industry Strategy: The UK government department responsible for business, industrial strategy, science, innovation and energy.

BECCS

Bioenergy with Carbon Capture and Storage: The process of extracting energy from biomass and capturing and storing the carbon, removing CO2 emissions from the atmosphere.

CCC

Committee on Climate Change: A non- departmental public body that advises the UK government on emissions targets and reports to Parliament on progress made in reducing greenhouse gas emissions.

CCUS/CCS*

Carbon Capture Usage and Storage: A pioneering technology that can capture up to 90% of the carbon dioxide (CO2) emissions produced from the use of fuels in electricity generation and industrial processes, preventing the carbon

dioxide from entering the atmosphere. The process involves trapping CO2 burnt by fuels, transporting it through pipeline infrastructure to be stored deep under the sea.

* Carbon Capture, Usage, and Storage (CCUS) and Carbon Capture and Storage (CCS) are used almost interchangeably, this report only uses

CCUS, with exceptions when CCS is used directly in the cited sources.

Foundation Industries

The UK’s foundation industries are producers of materials such as basic metals, fabricated metals, wood, non-metallic minerals and basic chemicals used by other manufactures.

GHG

Greenhouse Gases: Any gas in the atmosphere which absorbs and re-emits heat, and thereby keeps the planet’s atmosphere warmer than it otherwise would be.

Global CCS Institute

An international think-tank whose mission is to accelerate the deployment of carbon capture and storage.

IPCC

Intergovernmental Panel on Climate Change: The United Nations intergovernmental body responsible for assessing the science related to climate change.

MtCO2e

Metric tonnes of Carbon Dioxide equivalent.

A metric measurement used to assess the contribution of different greenhouse gases to global warming.

Net Zero

A target of 100% reduction in greenhouse gas emissions. It is referred to as ‘net’ as the expectation is that it would be met with some remaining sources of emissions which would need to be offset by removals of CO2 from the atmosphere.