Could Great Britain go off grid?

We believe investing in our people goes hand-in-hand with enabling the green energy transformation and positive future growth.

We believe investing in our people goes hand-in-hand with enabling the green energy transformation and positive future growth.

We believe investing in our people goes hand-in-hand with enabling the green energy transformation and positive future growth.

Information about our business, partnerships and campaigns, as well as photos, graphics and multimedia assets for journalists, and educational materials for schools.

We’re committed to enabling a zero carbon, lower cost energy future through engineering, technology and innovation.

We’re building for a sustainable future in how we source our biomass, generate energy, remove carbon dioxide and function as a business.

Read our carbon capture, sustainable bioenergy and power generation stories, as well as thinking from Drax’s leaders and business updates.

Explore a comprehensive guide to our business model and investor relations.

Drax Group’s ambition is to become a carbon negative business by 2030, through innovative greenhouse gas removal technology.

Electricity is unlike any other resource. The amount being generated must exactly match demand for it, around the clock.

Managing this delicate balancing act is the job of the National Grid Electricity System Operator (ESO), which works constantly to ensure supply meets demand and the grid remains balanced. One of the ways it does this is by storing energy when there is too much and deploying it when there is too little.

Although there are many different ways of storing energy at a small scale, at grid level it becomes more difficult. One of the few ways it is currently possible is through pumped hydro storage. Cruachan Power Station in the Highlands of Scotland is one of four pumped storage facilities in Great Britain. It uses electrically-driven turbines to pump water up a mountain into a reservoir when there is excess electricity on the grid, and then releases the water stored in the reservoir back down, to spin the same turbines to generate power when it’s needed quickly.

The dual capabilities of these turbines are unique to pumped hydro storage and contribute to the overall grid’s stability. However, what dictates when Cruachan’s turbines switch from pump to generate and vice versa is all a matter of what the grid needs – and when.

While the machine hall of Cruachan Power Station is an awe-inspiring place for its size and location 396 metres beneath Ben Cruachan, it generates electricity much like any other hydropower station: harnessing the flow of water to rotate any number of its four 100+ megawatt (MW) turbines.

This mode – simply called ‘generate mode’ – is usually employed during periods of peak power demand such as mornings and evenings, during a major national televised event, or when wind and solar energy output drops below forecast. As a result, starting up and generating millions of watts of electricity has to be fast.

“It takes just two minutes for a turbine to run up from rest to generate mode,” says Martin McGhie, Operations and Maintenance Manager at the power station. “It takes slightly longer for the turbines to run down from generate to rest, but whatever function the turbines are performing, they can reach it within a matter of minutes.”

The reverse of generate mode is pump mode, which changes the direction of travel for the water, this time using electricity from the grid to pump water from the vast Loch Awe at the foot of Ben Cruachan to the upper reservoir, where it waits ready to be released.

In contrast to generate mode, pump mode typically comes into play at times when demand is low and there is too much power on the system, such as during nights or at weekends, when there is excessive wind generation. However, the grid has evolved since Cruachan first began generating in 1965 and this has changed when it and how it operates.

“In the early days, Cruachan was used in a rather predictable way: pumping overnight to absorb excess generation from coal and nuclear plants and generating during daytime peak periods,” says Martin. “The move to more renewable energy sources, like wind, mean overall power generation is more unpredictable.”

He continues: “There has also been a move from Cruachan being primarily an energy storage plant to one which can also offer a range of ancillary services to the grid system operator.”

In between pumping water and generating power, Cruachan’s turbines can also spin in air while connected to the grid, neither pumping not generating. This is essentially a ‘standby mode’ where the turbines are ready to either quickly switch into generation or pumping at a moment’s notice (they spin one way for ‘spin pump’; the other for ‘spin generate’). These spin modes are requested by the ESO to ensure reserve energy is available to respond rapidly to changes on the grid system.

In spin generate mode, the generator is connected up to the grid but the water is ejected from the space around the turbine by injecting compressed air. The turbine does not generate power but is kept spinning, allowing it to quickly start up again. As soon as the grid has an urgent need for power, the air is released and the water from the upper reservoir flows into the turbine to begin generation in under 30 seconds.

Spin pump works on the same basis as spin generate, but with the turbine rotating in the opposite direction, ready to pump at short notice. This allows Cruachan to absorb excess generation and balance the system as soon as the ESO needs it.

“The use of spin mode by the ESO is highly variable and dependant on a number of factors e.g. weather conditions or the state of the grid system at the time” says Martin. This unpredictability of the increasingly intermittent electricity system makes the flexibility of Cruachan’s multiple turbines all the more important.

It’s not only the types of electricity generation around the system that are changing how Cruachan operates. Martin suggests that the way energy traders and the ESO use Cruachan will continue to evolve as the market requirements and opportunities change.

Technology is also changing the market and Martin predicts this could affect what Cruachan does. “In the future we will face competition from alternative storage technologies, such as batteries, electric vehicles, as well as competition for the other ancillary services we offer.”

However, Cruachan’s flexibility to generate, absorb or spin in readiness means it is prepared to adjust to any future changes.

“Cruachan is always ready to modify or upgrade to meet requirements, as we have done in the past,” says Martin. “The priority is always to be able to deliver the services required by the grid system operator – in characteristic quick time.”

Visit Cruachan — The Hollow Mountain to take the power station tour.

Read our series on the lesser-known electricity markets within the areas of balancing services, system support services and ancillary services. Read more about black start, system inertia, frequency response, reactive power and reserve power. View a summary at The great balancing act: what it takes to keep the power grid stable and find out what lies ahead by reading Balancing for the renewable future.

Demand for electricity might have been 6% lower in the first three months of 2019 than in last year’s first quarter but the demand for lower carbon power is only growing and there’s more pressure than ever for global industries to decarbonise more rapidly.

Aided by a significantly milder winter than last year, Great Britain’s electricity sector continued to make further progress in reducing carbon emissions in the first quarter (Q1) of 2019.

The carbon intensity of Great Britain’s electricity was almost 20% lower in Q1 2019 than in the same period last year. This was driven by a significant decrease in coal usage, with 581 coal-free hours in total over the period – eight times more than in Q1 2018. This trend has only increased, with May seeing the country’s first coal-free week in modern times.

The findings come from Electric Insights, a report commissioned by Drax and written independently by researchers from Imperial College London, that analyses Great Britain’s electricity consumption and looks at what the future might hold.

As public, commercial and political demand for lower carbon emissions mounts, the question for the power system is: can it truly reach zero-emissions?

Quarter after quarter, the carbon intensity of Great Britain’s electricity system has declined. From 545 grams of carbon dioxide (CO2) per kilowatt hour (g/kWh) in Q1 2012, to just over 200 g/kWh last quarter. For a single hour, carbon emissions have fallen as low as just 56 g/kWh. But how soon can that figure reach all the way down to net-zero carbon emissions?

Quarter after quarter, the carbon intensity of Great Britain’s electricity system has declined. From 545 grams of carbon dioxide (CO2) per kilowatt hour (g/kWh) in Q1 2012, to just over 200 g/kWh last quarter. For a single hour, carbon emissions have fallen as low as just 56 g/kWh. But how soon can that figure reach all the way down to net-zero carbon emissions?

The National Grid’s Electricity System Operator (ESO), believes it could be as soon as 2025. But some serious changes are needed to make it possible for the system to operate safely and efficiently, when you have fewer sources offering balancing services like reserve power, inertia, frequency response and voltage control.

The National Grid ESO believes an approach that establishes a marketplace for trading services holds the solution. The hope is that competition will breed new innovation and bring new technologies such as grid-scale storage and AI into the commercial energy markets, offering reserve power and more accurate forecasting for solar and wind power.

For the meantime, weather-dependent technologies are a key source of renewable electricity in Great Britain, with wind making up more than 20% of all generation in Q1 2019. However, with wind capacity only expected to increase, how should the system react when it’s not an option?

Read the full article, co-authored by Julian Leslie, Head of National Control, National Grid ESO: How low can we go?

Today there are around 20 gigawatts (GW) of wind capacity installed around Great Britain, and this is forecast to double to 40 GW in the next seven years. However, average wind output can fluctuate between 2 GW one day and 12 GW the next – as happened twice in January. It highlights the ongoing needs for flexibility and diversity of sources in the electricity system even as it decarbonises.

There are a number of ways to make up for shortfalls in wind generation. The most obvious of which is through other existing sources. There is more solar installed around the county than any source of generation (except gas), at 12.9 GW and sun power helped meet demand during a wind drought last summer. Solar averaged 1.3 GW over the last 12 months, this is more than coal which accounted for 1.1 GW.

However, storage will also be important in delivering low or zero-carbon sources of electricity when there is neither wind nor sufficient sunlight. At present this includes pumped storage and some battery technologies, but in future will include greater use of grid-scale lithium-ion batteries, as well as vehicle-to-grid systems that can take advantage of power stored in idle electric cars.

New fuels, particularly hydrogen, also have the potential to meet demand and help create a wider lower-carbon economy for heating, as well as vehicle fuel, with water as the only emission.

Hydrogen can be produced from natural gas or using excess electricity from renewable sources, or through carbon capture from industrial emissions. It can then be stored for a long time and at scale, before being used to generate electricity rapidly when needed.

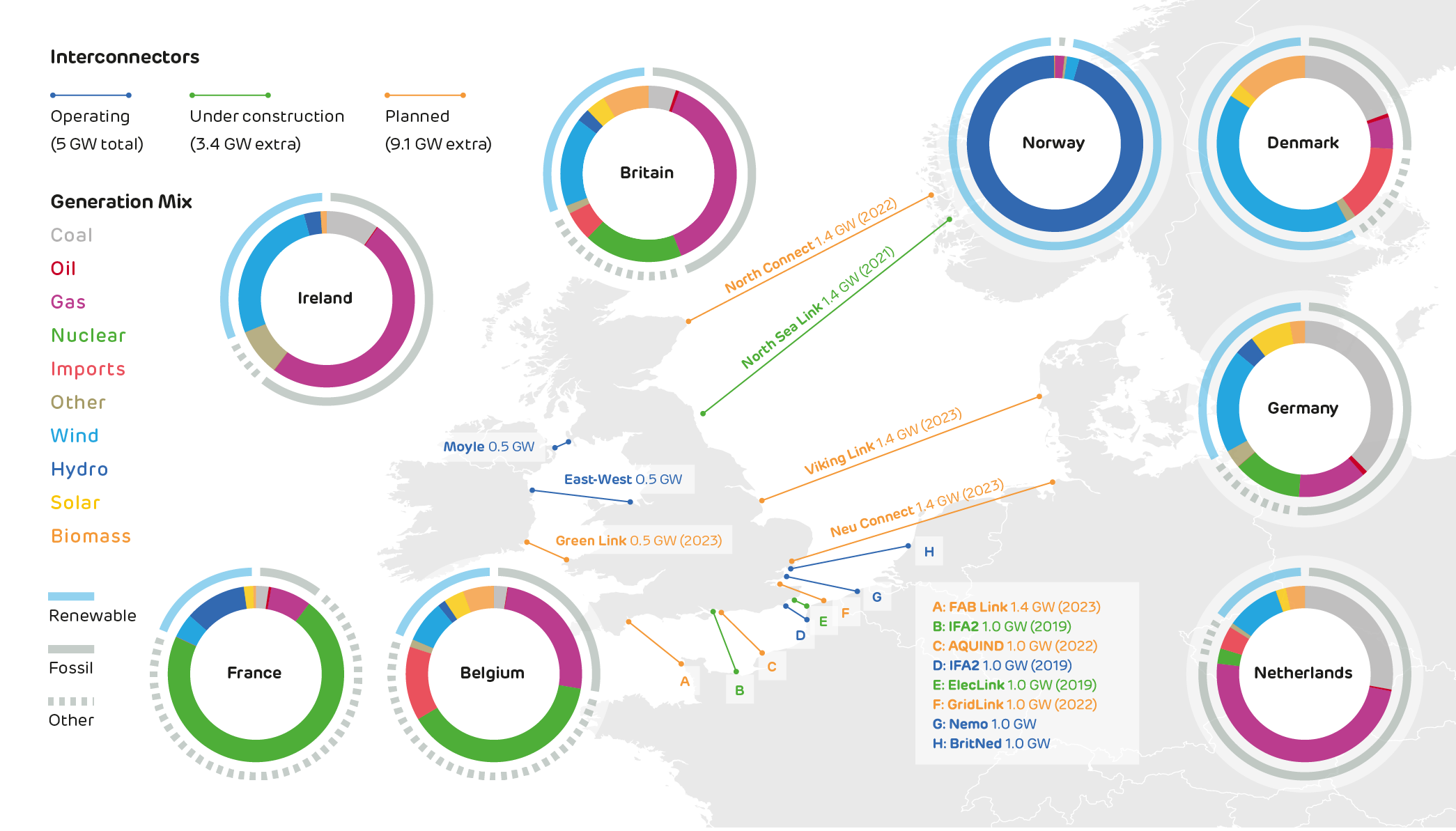

Another increasingly important source of Great Britain’s electricity is interconnectors. However, they are not yet being used in a way that can support gaps in the electricity system, with Northern European countries normally all experiencing the same weather – and wind levels – at the same time.

Read the full article: What to do when the wind doesn’t blow?

Great Britain added a new power source to its electricity system in Q1 2019, in the form of Belgium. The opening of the £600 million NEMO link between Kent and Zeebrugge added another 1 GW of interconnection capacity.

Great Britain added a new power source to its electricity system in Q1 2019, in the form of Belgium. The opening of the £600 million NEMO link between Kent and Zeebrugge added another 1 GW of interconnection capacity.

It joins connections to France, the Netherlands, Northern Ireland and the Republic of Ireland to bring Great Britain’s total interconnection capacity to 5 GW. These links accounted for 7.9% of the 78 terawatt hours (TWh) of electricity consumed over the quarter.

Electricity from imports also set new records for a daily average of 4.3 GW on 24 February, accounting for 12.9% of total consumption, and a monthly average in March when it made up 10.6% of consumption. These records represent the first time Great Britain fell below 90% for electricity self-sufficiency.

With 3.4 GW of new interconnectors under construction coming online by 2022 and 9.1 GW more planned to be completed over the next five years, Great Britain’s neighbours are set to play a growing role in the country’s electricity mix.

However, while interconnectors offer an often cost-effective way for Great Britain to ensure electricity supply meets demand, the carbon intensity of neighbouring countries’ electricity should also be considered.

Read the full article: 10% of electricity now generated abroad

The new link to Belgium has imported, rather than exported, electricity every day since it began operations, as Belgium has the lowest natural gas prices in Europe and its power stations pay £16 per tonne less for carbon emissions than their British counterparts. This makes it cheaper to import, and less carbon intense, than electricity from the more coal-dependant Netherlands and Ireland.

Planned links to Germany and Denmark could allow Great Britain to import more renewable power. However, if there is a wind drought across Northern Europe these countries often turn to their emissions-heavy coal or even dirtier lignite sources.

France is currently Great Britain’s cleanest source of imports, mostly using nuclear and renewable generation. However, when the North Sea Link opens in 2021, it will give Great Britain access to Norway’s abundance of hydro-power to plug gaps in renewable generation.

Considering the carbon intensity of Great Britain’s imports is important because the decarbonisation needed to address the global climate change emergency can’t be solved by one country alone. For electricity emissions to go as low as they can it takes collaboration that goes across borders.

Read the full article: Where do Britain’s imports come from?

What’s the biggest battery you can think of? A car battery? A grid-scale lithium-ion array? What about a battery the size of a mountain?

That’s what you’ll find on the banks of Loch Awe in Argyll, Scotland. Cruachan Power Station is a pumped hydro storage facility comprised of nearly 20 km of tunnels and chambers cutting through the mountain of Ben Cruachan.

Built in the 1960s, the site, known as ‘The Hollow Mountain’ entails a subterranean power station, a reservoir, a dam, and the loch itself. These components all work together to store a huge amount of energy, or enough to power more than 880,000 homes, at a moment’s notice.

This probably doesn’t fit your image of what a battery looks like. But the principle is the same. The purpose of any battery, from the AAs in your remote control to the one in your phone that you charge every night, is to store power for future use.

In an AA battery, that storage takes the form of chemicals within the battery which release electricity under the right conditions. In pumped hydro, the purpose is the same, but instead of being stored in chemicals, that energy is stored in the gravitational potential energy of 10 million cubic meters of water, sitting poised to spin Cruachan’s turbines and generate 440 megawatts (MW) of electricity.

Such a huge amount of water is the equivalent of around seven gigawatt-hours (GWh) of energy. If the reservoir is full, the Hollow Mountain can power a city for more than 15 hours.

Cruachan Power Station is one of only four such storage facilities in the UK. Inside the mountain, 396 metres beneath the surface, is a chamber about the size of a football pitch, and the height of a seven-storey building. Here sit four electricity-generating turbines, each weighing around 650 tonnes.

A series of tunnels and channels connect these turbines to two enormous bodies of a water: Loch Awe at the base and the Ben Cruachan reservoir further up the mountain.

The turbines can function both as pumps and as generators. When there is an excess of power on the grid, and electricity is cheap, the turbines consume electricity and work to pump water up from the loch below to the reservoir 300 metres above.

Then, when electricity demand rises, the turbines reverse direction. Now the water flows down from the reservoir and through the turbines, which switch to generating electricity and supply it to the grid.

This is an extremely quick process. Unlike coal or nuclear stations, which can take hours to get up to full capacity, Cruachan can go from standstill to generating within two minutes – perfect for reacting to variance in grid demand at short notice.

Often National Grid ESO (electricity system operator) keeps one or more of Cruachan’s four units spinning in air. Compressed air is used to evacuate water from around a turbine to allow it to spin. When necessary, it can go from zero megawatts to 100 MW or more in less than 30 seconds.

In any given day, the system operator may call on Cruachan Power Station multiple times as the requirements to manage the grid constantly change.

Cruachan is a net generator of power across the year thanks to the large amount of water flowing into its reservoir from a system of aqueducts. However, pumped hydro is primarily about storing energy – not actively producing it in the way wind, solar, gas, biomass or conventional hydropower facilities might.

In fact, the UK’s four pumped hydro power stations are a combined net consumer of electricity. But this is the case with regular batteries as well, when construction is factored in.

Nevertheless, pumped hydro storage is still efficient – around 70% to 80% of the electricity used in pumping is recovered in generation. Sometimes, the convenience of getting access to power when it’s needed is more valuable than how much power is conserved.

But why store so much energy in such an improbable location to begin with?

There are two key reasons: The first is that the grid doesn’t operate under the same conditions all the time. Great Britain will use more or less electricity owing to its needs. For example, overnight there is a lower demand than at 5pm on a weekday evening. This means sometimes the grid is demanding more electricity than is being supplied, and sometimes vice versa.

Secondly, there’s the increasing level of intermittent energy sources, like wind and solar, supplying low carbon electricity. These sources are highly dependent on the weather and can’t be easily turned up or down in response to grid conditions.

Batteries can address these two issues. In times of higher electricity supply than demand, storage systems can absorb and store electricity from the grid, which helps balance frequency and prevent surges; and in times of high demand, then can quickly deliver electricity where it’s needed.

Pumped hydro is an important part of this equation – in fact, while other types of grid-scale batteries are receiving significant investment, they are still in their infancy. Pumped storage, by contrast, already accounts for 95% of all installed storage capacity in the world, around 130 GW.

One of the challenges in installing more pumped hydro storage is finding suitable geography – places which are both mountainous, with nearby suitably large bodies of water.

However, there have been experiments into river and tidal-based pumped hydro storage projects. Senator Wash Dam on the Colorado River uses pumping to store water upstream from the Imperial Hydropower Dam so it can be released when needed, while the Rance Tidal Power Station in France pumps sea water behind the barrage to allow it to start up faster.

Storage solutions will become more important as electricity systems increasingly move towards renewable and low carbon sources. Pumped storage helps to meet peak-time demand and provide grid stability by making use of the landscape and gravity to deliver electricity when it’s needed.

Guided tours of Cruachan: The Hollow Mountain are available via VisitCruachan.co.uk

Great Britain’s electricity system has had its robustness tested at both ends of the thermometer in 2018. First, the once-in-a-decade low temperatures of the ‘Beast from the East’ saw electricity demand reach its highest peak in three years on 1 March as the country turned on electric heaters and extra lighting.

Following fast on its heels was an unusually hot, dry and still summer that pushed demand up by the equivalent of adding a second Scotland to the system, and required solar generation to make up for a ‘wind drought’. And all of this happened in the first half of the year.

So far the second half of the year has seen fewer instances of freak weather, which has meant fewer peaks in the power system. While uneventful in this sense, the last quarter of Great Britain’s power does go some way towards showing us what we might expect from the system in the future.

The findings come from Electric Insights, an independent report written by researchers at Imperial College London and commissioned by Drax, that analyses the country’s power and hints at what we might expect in the future.

Quarter after quarter Great Britain breaks new renewable records and Q3 2018 was no exception. The three-month period from July through September saw total capacity of renewable sources exceed fossil fuels for the first time. Great Britain now has 40.6 gigawatts (GW) of gas, coal, diesel and oil-fired power generation capacity, compared to 41.9 GW of capacity from wind, solar, biomass, hydro and waste sources. To put this into perspective, at the start of the decade fossil fuel capacity was seven times that of renewables.

Since 2010 renewables have grown six-fold. Wind passed 20 GW of installed capacity in September and is now the country’s largest renewable source. Solar has slowed in growth but remains the second biggest renewable, with 13 GW of capacity.

Biomass is now the third largest source of renewable electricity thanks to the coal-to-biomass conversions of Lynemouth power station and Drax’s Unit 4, which together added 1 GW more renewable electricity to the system. Along with these conversions, a quarter of the country’s coal capacity retired in the last year, leaving just six generators in operation.

While this shift to renewables is helping decarbonise Great Britain’s power system, the increasing intermittency that comes with it means balancing the grid is becoming more complicated.

Read the full article, co-authored by Luke Clark at RenewableUK: Renewables leapfrog fossil capacity

The daily cost of running the transmission system – which manages the flow of electricity from generators to consumers – has doubled over the last four years. This growth has been steady since 2010, but Q3 2018 saw the cost reach one-sixth higher than the previous record in Q3 2017. Over this quarter, balancing the system on average cost £3.8 million per day, with three days seeing costs exceed £10 million, in turn adding 6% to the overall wholesale price of electricity.

Part of the reason for the increased costs is that need for balancing services such as voltage control, reserve power and frequency response spike when there are high levels of intermittent renewables (such as wind and solar) on the system. As this type of generation can’t be perfectly calculated it is important for National Grid to ensure there are flexible reserve sources running to plug gaps and help move electricity around the grid, both of which incur balancing costs. For example, in September balancing costs spiked several times as a result of increases in wind power.

The rising price highlights that for the grid to function it’s not just a matter of generating enough electricity to meet demand. Where and when it is generated is as important to maintain its stability, and with ever-increasing levels of intermittent renewables the need for stabilising services will grow.

Read the full article: The cost of staying in balance

It’s not just balancing costs, however, that are driving up the cost of electricity. Day-ahead market prices have risen by 50% over the last year – from an average of £42/MWh in Q3 2017 to £60/MWh last quarter.

This was not the result of spikes caused by events such as the ‘Beast from the East’ or the summer’s World Cup final, but by a gradual creeping up of prices caused by a combination of increasing gas prices and carbon emissions costs, as well as a weaker pound in the wake of ongoing Brexit negotiations.

Gas power stations are six times more influential on power price than any other generation technology, but with global gas prices rising 50%, the country’s primary source of flexible generation is becoming costlier.

The knock on effect of this 10-year high gas price was not only an impact on consumers’ pockets but also a resurgence in coal, which became cheaper than gas and led to a 15% increase in carbon emissions from electricity generation for a period during the quarter. Adding to this, the European Emissions Trading Scheme (ETS) increased the price of carbon dioxide (CO2) emissions by a factor of four over the past 12 months, pushing up the cost of wholesale electricity even further.

The international nature of the electricity system also makes prices vulnerable to currency fluctuations and a weakening pound made the impact greater. The currency devaluations following the EU referendum are continuing to contribute to this and Ofgem found it caused an 18% increase in electricity prices. This isn’t the referendum’s only effect.

If the UK leaves the EU next year under a no-deal scenario the country would also exit the ETS, removing a component of the current total carbon price. There are plans to replace this with a new tax, adding to the existing UK carbon price support (CPS), but this would only come into effect from April 2019, leaving Q1 with just the CPS – effectively making it cheaper to emit carbon during that three-month period, which in turn adds a risk of more carbon-intensive sources becoming more economically viable than renewable sources.

While there is little Great Britain can do to influence international fuel prices, it can alter domestic policies to influence the price for consumers. Making heavily emitting fuels economically prohibitive and incentivising more lower carbon and renewable sources onto the system, can reduce dependency on imported fuels and cut carbon costs.

Read the full article: Wholesale power prices hit a 10-year high

Will Gardiner, CEO, Drax Group

“I am excited by the opportunity to acquire this unique and complementary portfolio of flexible, low-carbon and renewable generation assets. It’s a critical time in the UK power sector. As the system transitions towards renewable technologies, the demand for flexible, secure energy sources is set to grow. We believe there is a compelling logic in our move to add further flexible sources of power to our offering, accelerating our strategic vision to deliver a lower-carbon, lower-cost energy future for the UK.

“This acquisition makes great financial and strategic sense, delivering material value to our shareholders through long-term earnings and attractive returns.

“We are combining our existing operational expertise with the specialist technical skills of our new colleagues and I am looking forward to what we can achieve together.”

The Portfolio consists of Cruachan pumped storage hydro (440MW), run-of-river hydro locations at Galloway and Lanark (126MW), four CCGT(2) stations: Damhead Creek (805MW), Rye House (715MW), Shoreham (420MW) and Blackburn Mill (60MW), and a biomass-from-waste facility (Daldowie).

Clatteringshaws Loch and dam, part of the Galloway Hydro Scheme

The Portfolio is expected, based on recent power and commodity prices, to generate EBITDA in a range of £90-110 million, from gross profits of £155 million to £175 million, of which around two thirds is expected to come from non-commodity market sources, including system support services, capacity payments, Daldowie and ROCs(3). Pumped storage and hydro activities represent a significant proportion of the earnings associated with the portfolio. Further information is set out in Appendix 2 of this Announcement.

Capital expenditure in 2019 is expected to be in the region of £30-35 million.

For the year ended 31 December 2017, the Portfolio generated EBITDA of £36 million(4). EBITDA in 2019 is expected to be higher due to incremental contracted capacity payments (c.£42 million), no availability restrictions (Cruachan’s access to the UK grid during 2017 was limited by network transformer works) (c.£8 million), a lower level of corporate cost charged to the portfolio (c.£9 million) and revenues from system support services and current power prices. Gross assets as at 31 December 2017 were £419 million(5).

The Acquisition represents an attractive opportunity to create significant value for shareholders and is expected to deliver returns significantly in excess of the Group’s WACC and to be highly accretive to underlying earnings in 2019.

The Acquisition strengthens the Group’s ability to pay a growing and sustainable dividend. Drax remains committed to its capital allocation policy and to its current £50 million share buy-back programme, with £32 million of shares purchased to date.

Drax has entered into a fully underwritten £725 million secured acquisition bridge facility agreement to finance the Acquisition. Assuming performance in line with current expectations, net debt to EBITDA is expected to fall to Drax’s long-term target of around 2x by the end of 2019.

Drax expects its credit rating agencies to view the Acquisition as contributing to a reduced risk profile for the Group and to reaffirm their ratings.

The Acquisition is expected to complete on 31 December 2018 and is conditional upon the approval of the Acquisition by Drax’s shareholders and clearance by UK Competition and Markets Authority (the “CMA”). A summary of the terms of the Acquisition agreement (the “Acquisition Agreement”) is set out in Appendix 1 to this announcement.

Since publishing its half year results on 24 July 2018 Drax has commenced operation of a fourth biomass unit at Drax Power Station, which is performing in line with plan, and availability across biomass units has been good.

Biomass storage domes at Drax Power Station

Taking these factors into account, alongside a strong 2018 hedged position and assuming good operational availability for the remainder of the year, Drax’s EBITDA expectations for the full year remain unchanged, with net debt to EBITDA now expected to be around 1.5x for the full year, excluding the impact of the Acquisition.

Biomass generation is now fully contracted for 2019.

| 2018 | 2019 | 2020 | |

|---|---|---|---|

| Power sales (TWh) comprising: | 18.6 | 11.5 | 5.7 |

| TWh including expected CfD sales | 18.6 | 15.6 | 11.2 |

| – Fixed price power sales (TWh) | 18.6 | 11.0 | 5.1 |

| At an average achieved price (per MWh) | at £46.8 | at £50.4 | at £48.3 |

| – Gas hedges (TWh) | - | 0.5 | 0.6 |

| At an achieved price per therm | - | 43.5p | 47.4p |

Drax intends to hedge up to 1TWh of the commodity exposures in the Portfolio ahead of completion in line with the Group’s existing hedging strategy.

In light of the Acquisition and the expected timing of the general meeting to approve it, Drax will postpone the planned Capital Markets Day on 13 November 2018.

Drax expects to announce its full year results for the year ending 31 December 2018 on 26 February 2019.

Enquiries:

Drax Investor Relations: Mark Strafford

+44 (0) 1757 612 491

+44 (0) 7730 763949

Media:

Drax External Communications:

Matt Willey

+44 (0) 7711 376087

Ali Lewis

+44 (0) 77126 70888

J.P. Morgan Cazenove (Financial Adviser and Joint Corporate Broker):

+44 (0) 207 742 6000

Robert Constant

Jeanette Smits van Oyen

Carsten Woehrn

Royal Bank of Canada (Joint Corporate Broker):

+44 (0) 20 7653 4000

James Agnew

Jonathan Hardy

Management will host a presentation for analysts and media at 9:00am (UK Time), Tuesday 16 October 2018, at FTI Consulting, 200 Aldersgate, Aldersgate Street, London EC1A 4HD.

Would anyone wishing to attend please confirm by e-mailing [email protected] or calling Christopher Laing at FTI Consulting on +44 (0) 20 3727 1355 / 07809 234 126.

The meeting can also be accessed remotely via a live webcast, as detailed below. After the meeting, the webcast will be made available and access details of this recording are also set out below.

A copy of the presentation will be made available from 9am (UK time) on Tuesday 16 October 2018 for download at: www.drax.com>>investors>>results-reports-agm>> #investor-relations-presentations or use the link below.

| Event Title: | Drax Group plc: Acquisition of flexible, low-carbon and renewable UK power generation from Iberdrola |

| Event Date: | Tuesday 16 October 2018 |

| Event Time | 9:00am (UK time) |

| Webcast Live Event Link | https://www.drax.com/investors/16-oct-2018-webcast |

| 020 3059 5868 (UK) | |

| +44 20 3059 5868 (from all other locations) | |

| Start Date: | Tuesday 16 October 2018 |

| Delete Date: | Monday 14 October 2019 |

| Archive Link: | https://www.drax.com/investors/16-oct-2018-webcast |

For further information please contact Christopher Laing on +44 (0) 20 3727 1355 / 07809 234 126.

Website: www.drax.com

Drax Smart Generation Holdco Limited (“Drax Smart Generation”), a wholly owned subsidiary of Drax, has entered into the Acquisition Agreement with Scottish Power Generation Holdings Limited (the “Seller”), a wholly-owned subsidiary of Iberdrola S.A., for the acquisition of ScottishPower Generation Limited (“SPGEN”), for £702 million in cash.

Loch Awe and Cruachan Reservoir from Ben Cruachan, Argyle and Bute

The Portfolio principally consists of 2.6GW of assets which are highly complementary to Drax’s existing generation portfolio and play an important role in the UK energy system. The assets include:

Turbine hall at Cruachan Power Station

440MW of large-scale storage and flexible low-carbon generation situated in Argyll and Bute, Scotland.

Cruachan provides a wide range of system support services to the UK energy market, in addition to providing merchant power generation. Cruachan has £35 million of contracted capacity payments for the period 2019 to 2022.

Cruachan, which provides over 35% of the UK’s pumped storage by volume, can provide long-duration storage with the ability to achieve full load in 30 seconds, which it can maintain for over 16 hours, making it a strategically important asset remunerated by a broad range of non-commodity based revenues.

Galloway Hydro Scheme, River Dee

126MW of stable and reliable renewable generation situated in South-west Scotland.

Both locations benefit from index-linked ROC revenues extending to 2027 and Galloway, in addition to renewable power generation, operates a reservoir and dam system providing storage capabilities and opportunities for peaking generation and system support services. It also has £4 million of contracted capacity payments for the period 2019 to 2022.

1,940MW of capacity at Damhead Creek (805MW), Rye House (715MW) and Shoreham (420MW) all strategically located in South-east England.

Shoreham Power Station, West Sussex

These assets provide baseload and/or peak power generation in addition to other system support services and benefit from attractive grid access income associated with their location. The three plants have contracted capacity payments of £127 million for the period 2019 to 2022.

Damhead Creek Power Station, Isle Of Grain, Kent

Damhead Creek also benefits from an attractive option for the development of a second CCGT asset, Damhead Creek II, which provides additional gas generation optionality alongside Drax’s existing coal-to-gas repowering and OCGT(6) projects. All options could be developed subject to an appropriate level of support. Damhead Creek II is eligible for the 2019 capacity market auction along with two of Drax’s existing OCGT projects.

The portfolio also includes a small CCGT in Blackburn (60MW) and a 50K tonne biomass-from-waste facility in Daldowie, which benefits from a firm offtake contract agreement with Scottish Water until 2026.

The UK has a target to reduce carbon emissions by 80% by 2050. The transition to a low-carbon economy requires decarbonisation of heating, transport and generation. This will in turn require additional low-carbon sources of generation to be developed in the UK. As much as 85%(7) of future generation could come from renewables – predominantly wind and solar. This will lead, at times, to high levels of power price volatility and increasing demand for system support services. Managing an energy system with these characteristics will only be possible if it is supported by the right mix of flexible assets to manage volatility, balance the system and provide crucial non-generation services which a stable energy system requires.

Pylon and electricity transmission lines from Cruachan Power Station above Loch Awe

The Acquisition is closely aligned with this structural need and the operation of Drax’s existing biomass and gas options which provide the flexibility required to enable higher levels of intermittent renewable generation.

The Acquisition is in line with these system needs and when combined with Drax’s existing flexible, biomass generation and gas options offers the Group increased exposure to the growing need for system support and power price volatility.

The Acquisition is closely aligned with this structural need and the operation of Drax’s existing biomass and gas options which provide the flexibility required to enable higher levels of intermittent renewable generation.

The Acquisition is in line with these system needs and when combined with Drax’s existing flexible, biomass generation and gas options offers the Group increased exposure to the growing need for system support and power price volatility.

Two thirds of the gross profits of the Portfolio is expected to come from non-commodity market sources, including system support services, capacity payments, Daldowie and ROCs, in addition to power generation activities. Due to the expected growing demand for these assets and the contract-based nature of many of these services Drax expects to improve long-term earnings visibility through structured non-commodity earnings streams, whilst retaining significant opportunity to benefit from power price volatility.

When combined with renewable earnings and system support from existing biomass generation, the Acquisition is expected to lead to an increase in the quality of earnings.

Wood pellet storage domes at Drax Power Station, Selby, North Yorkshire

The Acquisition accelerates Drax’s development from a single-site generation business into a multi-site, multi-technology operator.

With the acquisition of this portfolio, a fall in gas prices could be mitigated by an increase in gas-fired generation reflecting the relative dispatch economics of the different technologies.

Drax expects to benefit from the management of generation across a broader asset base, leveraging the Group’s expertise in the operation, trading and optimisation of large rotating mass generation.

Drax believes that the team operating the Portfolio has a strong engineering culture which is closely aligned with the Drax model and will enhance the Group’s strong capabilities across engineering disciplines.

Around 260 operational roles will transfer to Drax as part of the Acquisition, complementing and reinforcing Drax’s existing engineering and operational capabilities.

Drax has entered into a fully underwritten £725 million secured acquisition bridge facility to finance the Acquisition, with a term of 12 months from the first date of utilisation of the facility (with a seven-month extension option) and interest payable at a rate of LIBOR plus the applicable margin (the “Acquisition Facility Agreement”). The facility is competitively priced and below Drax’s current cost of debt.

Drax will consider its options for its long-term financing strategy in 2019.

Assuming performance in line with current expectations, net debt to EBITDA is expected to return to Drax’s long-term target of around 2x by the end of 2019.

Drax expects credit rating agencies to view the Acquisition as supportive of the rating and contributing to a reduced risk profile for the Group.

Drax is progressing a detailed integration plan to combine the Acquisition as part of the existing Power Generation business.

The transaction is subject to shareholder approval. A combined Shareholder Circular and notice of General Meeting will be posted as soon as practicable.

The transaction is expected to complete on 31 December 2018.

(1) EBITDA is defined as earnings before interest, tax, depreciation, amortisation and material one-off items that do not reflect the underlying trading performance of the business. 2019 EBITDA is stated before any allocation of Group overheads.

(2) Combined Cycle Gas Turbine.

(3) Renewable Obligation Certificates.

(4) 2017 EBITDA is unaudited and based on the audited financial statements of Scottish Power Generation Limited and SMW Limited, adjusted to exclude results of assets that do not form part of the Portfolio and restated in accordance with Drax accounting policies.

(5) On an unaudited historic cost basis, inclusive of an historic write down and other changes arising from the application of Drax’s accounting policies, and incorporating intercompany debtors which will be replaced by Drax going forward.

(6) Open Cycle Gas Turbines.

(7) Intergovernmental Panel on Climate Change. In a 1.5c pathway renewables are projected to be 70-85% of global electricity in 2050.

The contents of this announcement have been prepared by and are the sole responsibility of Drax Group plc (the “Company”).

J.P. Morgan Limited (which conducts its UK investment banking business as J.P. Morgan Cazenove) (“J.P. Morgan Cazenove”) and RBC Europe Limited (“RBC”), which are both authorised by the Prudential Regulation Authority (the “PRA”) and regulated in the United Kingdom by the FCA and the PRA, are each acting exclusively for the Company and for no one else in connection with the Acquisition, the content of this announcement and other matters described in this announcement and will not regard any other person as their respective clients in relation to the Acquisition, the content of this announcement and other matters described in this announcement and will not be responsible to anyone other than the Company for providing the protections afforded to their respective clients nor for providing advice to any other person in relation to the Acquisition, the content of this announcement or any other matters referred to in this announcement.

J.P. Morgan Cazenove, RBC and their respective affiliates do not accept any responsibility or liability whatsoever and make no representations or warranties, express or implied, in relation to the contents of this announcement, including its accuracy, fairness, sufficient, completeness or verification or for any other statement made or purported to be made by it, or on its behalf, in connection with the Acquisition and nothing in this announcement is, or shall be relied upon as, a promise or representation in this respect, whether as to the past or the future. Each of J.P. Morgan Cazenove, RBC and their respective affiliates accordingly disclaims to the fullest extent permitted by law all and any responsibility and liability whether arising in tort, contract or otherwise which it might otherwise be found to have in respect of this announcement or any such statement.

Certain statements in this announcement may be forward-looking. Any forward-looking statements reflect the Company’s current view with respect to future events and are subject to risks relating to future events and other risks, uncertainties and assumptions relating to the Company and its group’s, the Portfolio’s and/or, following completion, the enlarged group’s business, results of operations, financial position, liquidity, prospects, growth, strategies, integration of the business organisations and achievement of anticipated combination benefits in a timely manner. Forward-looking statements speak only as of the date they are made. Although the Company believes that the expectations reflected in these forward looking statements are reasonable, it can give no assurance or guarantee that these expectations will prove to have been correct. Because these statements involve risks and uncertainties, actual results may differ materially from those expressed or implied by these forward looking statements.

Each of the Company, J.P. Morgan Cazenove, RBC and their respective affiliates expressly disclaim any obligation or undertaking to supplement, amend, update, review or revise any of the forward looking statements made herein, except as required by law.

You are advised to read this announcement and any circular (if and when published) in their entirety for a further discussion of the factors that could affect the Company and its group, the Portfolio and/or, following completion, the enlarged group’s future performance. In light of these risks, uncertainties and assumptions, the events described in the forward-looking statements in this announcement may not occur.

Neither the content of the Company’s website (or any other website) nor any website accessible by hyperlinks on the Company’s website (or any other website) is incorporated in, or forms part of, this announcement.

The following is a summary of the principal terms of the Acquisition Agreement.

The Acquisition Agreement was entered into on 16 October 2018 between Drax Smart Generation and the Seller. Pursuant to the Acquisition Agreement, the Seller has agreed to sell, and Drax Smart Generation has agreed to acquire, the whole of the issued share capital of SPGEN for £702 million, subject to certain customary adjustments in respect of cash, debt and working capital.

Drax Group Holdings Limited has agreed to guarantee the payment obligations of Drax Smart Generation under the Acquisition Agreement. Scottish Power UK plc has agreed to guarantee the payment obligations of the Seller under the Acquisition Agreement.

The Acquisition is conditional on:

Completion is currently expected to occur on 31 December 2018 assuming that the conditions are satisfied by that date.

Drax Smart Generation has the right to terminate the Acquisition Agreement upon the occurrence of a material reduction in available generation capacity at any of the Cruachan, Galloway and Lanark or Damhead Creek facilities which subsists, or is reasonably likely to subsist, for a continuous period of three months. The right of Drax Smart Generation to terminate in these circumstances is subject to the Seller’s right to defer Completion if the relevant material reduction in available generation capacity can be resolved by end of the month following the anticipated date of Completion.

A break fee of £14.6 million (equal to 1% of Drax’s market capitalisation at close of business on the day before announcement) is payable if the Shareholder Approval Condition is not met, save where this is as a result of a material reduction in available generation capacity as described above.

The Seller has given certain customary covenants in relation to the period between signing of the Acquisition Agreement and completion, including to carry on the SPGEN business in the ordinary and usual course. The Seller will carry out certain reorganisation steps prior to completion.

Drax Smart Generation has agreed to assume the accrued defined benefit pension liabilities associated with the employees of the SPGEN group as at the date of signing the Acquisition Agreement. Following Completion, the SPGEN group will continue to participate in the Seller’s group defined benefit pension scheme, known as the ScottishPower Pension Scheme (“SPPS”) for an interim period of 12 months unless agreed otherwise (the “Interim Period”) while a new pension scheme is set up by the SPGEN group for the benefit of its employees (the “New Scheme”).

At the end of the Interim Period, the SPPS trustees will be requested to transfer from the SPPS to the New Scheme an amount of liabilities (and corresponding share of assets) agreed between the Seller and Drax Smart Generation (or failing agreement, an amount determined by an independent actuary) in respect of the past service liabilities relating to the SPGEN group employees. If the amount of assets transferred to the New Scheme does not match the amount agreed (or independently determined), there will be a true-up between the Seller and Drax Smart Generation.

If the SPPS trustees do not make any transfer to the New Scheme within the period of 18 months following the Interim Period (unless this was caused by a breach of the Acquisition Agreement by the Seller), Drax Smart Generation has agreed to pay £16 million (plus base rate interest) to the Seller as compensation for the SPPS liabilities not taken on by the New Scheme.

The Seller has provided customary warranties in the Acquisition Agreement. The Seller also has provided Drax Smart Generation with indemnities in respect of certain specific matters, including for any losses associated with the reorganisation referred to above. A customary tax covenant is also provided in the Acquisition Agreement.

The Seller and SPGEN will enter into a transitional services agreement effective at Completion. The specific nature, terms and charges relating to the services to be provided will be agreed between the Seller and SPGEN prior to Completion. The Seller will also provide assistance in relation to the extraction and separation of the SPGEN group from the systems of the Seller and integration of the SPGEN group onto the systems of the Drax Group.

The Portfolio is expected, based on recent power and commodity prices, to generate EBITDA in a range of £90-110 million (“Profit Forecast”), and gross profits of £155 million to £175 million, of which around two thirds is expected to come from non-commodity market sources, including system support services, capacity payments, Daldowie and ROCs. Pumped storage and hydro activities represent a significant proportion of the earnings associated with the portfolio.

For the purpose of the Profit Forecast, EBITDA is stated before any allocation of Group overheads (as these will be an allocation of the existing Drax Group cost base which is not expected to increase as a result of the acquisition of the Portfolio).

The Profit Forecast has been compiled on the basis of the assumptions stated below, and on the basis of the accounting policies of the Drax Group adopted in its financial statements for the year ended 31 December 2017. Subsequent accounting policy changes include the application of IFRS15 and IFRS9 which are not initially expected to change the EBITDA results of the Portfolio. It also does not reflect the impact of IFRS16 which would apply in respect of the 2019 Annual Report and Accounts.

The Profit Forecast has been prepared with reference to:

The Profit Forecast is a best estimate of the EBITDA that the Portfolio will generate for a future period of a year in respect of assets and operations that are not yet under the control of Drax. Accordingly the degree of uncertainty relating to the assumptions underpinning the Profit Forecast is inherently greater than would be the case for a profit forecast based on assets and operation under the control of Drax and/or which covered a shorter future period. The Profit Forecast has been prepared as at today and will be updated in the shareholder circular.

The forecast cost base reflects the expectations of the Drax Directors of the operating regime of the Portfolio under Drax’s ownership and the central support it will require.

The Profit Forecast has been prepared on the basis of the following principal assumptions:

END

1 October 2018

The UK has come a long way in its efforts to decarbonise. Greenhouse gas emissions last year were 43% below 1990 levels, while increasing renewable electricity generation and a strengthening carbon price means the country could soon go coal-free for an entire summer.

There is still, however, much work needed to reach the UK target of reducing emissions to 20% of 1990 levels by 2050 and meeting the Paris Agreement’s aim of keeping temperature increases below two degrees Celsius. As ambitious as these goals may be, recent research by the Energy Transitions Commission (ETC) believes they can be met by 2050, with the right government policies and action from businesses.

To help to mitigate man made climate change, all industries, across all sectors must cut carbon emissions. It’s a big challenge but a clear first step must be the decarbonisation of electricity generation. This step will enable other industries to reduce their emissions in turn through electrification.

Since 2000 we have been building our experience in decarbonising electrical generation, transforming what was once Western Europe’s largest coal-fired power station into the UK’s biggest decarbonisation project. This puts us in a unique position to offer the leadership and innovation needed – across the electricity industry and other sectors – to reach a zero-carbon world.

The electrification of carbon-intensive sectors, such as transport and heating, will only contribute to reducing overall emissions if the electricity comes from mostly low or zero-carbon sources.

The ETC’s research suggests wind and solar will be capable of providing 85% of the world’s electricity generation by 2050. When these intermittent sources are unable to generate electricity the remaining 15% will come from a combination of nuclear, hydro, biomass and storage (including batteries, pumped storage and new technologies).

In fact, biomass alone could provide as much as half of that 15% but it is critical that this flexible, renewable, low carbon fuel must be sustainably sourced. For the wood biomass we use at Drax Power Station, its sourcing should contribute to growing and healthy forests, which will be another key part of the climate change solution.

Will Gardiner, CEO, Drax Group

At Drax, we have a long history of finding ways to cut emissions and improve the efficiency of our own biomass pellet supply chain, from bigger ships to more efficient rail freight loading and unloading.

The skills and experiences gained from these efforts serve not only to decarbonise our business but will benefit other supply chain-based industries along the path to lower-carbon emissions. More than this, it is far from the only way we are working towards doing this.

One of the biggest hopes for removing carbon from industry lies in carbon capture and storage. We’re leading the charge on bringing this technology to the fore by running a six-month pilot of a Bioenergy Carbon Capture and Storage (BECCS) system, which will capture a tonne of carbon every day from one of our four, 600+ megawatt (MW) biomass units.

Capturing emissions not only further reduces the carbon intensiveness of electricity generators of all kinds, but also opens new revenue streams for businesses through utilising captured carbon. For Drax, BECCS takes us another step towards becoming a carbon negative operation, where we remove more carbon from the atmosphere than we emit. It is also an opportunity to further expand the knowledge and experience of our team and become leading experts in a field which will be essential in meeting climate change goals.

Alongside this, our plans to repower the last of our coal-fired units to highly-efficient combined cycle gas turbines (CCGT) and build four, rapid-response open cycle gas turbines (OCGT) will give the electricity system the flexibility needed to support more intermittent renewable sources. The abilities of gas plant in balancing and system services can help to complete the journey away from coal before 2025. In subsequent decades, gas can play a pivotal role assisting the transition to a zero-carbon power system.

Alongside this, our plans to repower the last of our coal-fired units to highly-efficient combined cycle gas turbines (CCGT) and build four, rapid-response open cycle gas turbines (OCGT) will give the electricity system the flexibility needed to support more intermittent renewable sources. The abilities of gas plant in balancing and system services can help to complete the journey away from coal before 2025. In subsequent decades, gas can play a pivotal role assisting the transition to a zero-carbon power system.

Our retail businesses, Haven Power and Opus Energy, also allow us to help companies and the public sector outside of electricity generation to reduce their carbon footprint. Beyond just supplying renewable electricity, we’re also looking at ways through closer customer partnerships to help businesses leverage new technologies to use electricity more efficiently and in turn lower their costs.

Reaching a zero-carbon future is a monumental task for electricity producers that depends on innovative thinking and new technologies. We have the experience in developing transformative ideas and making them a reality – all of which will be essential in guiding us into a brighter, more stable, decarbonised future.

It’s not news to say Great Britain’s electricity system is changing. Low carbon electricity sources are on course to go from 22% of national generation in 2010 to 58% by 2020 as installation of wind and solar systems continue to grow.

But while there has been much change in the sources fuelling electricity generation, the system itself is still adapting to this transformation.

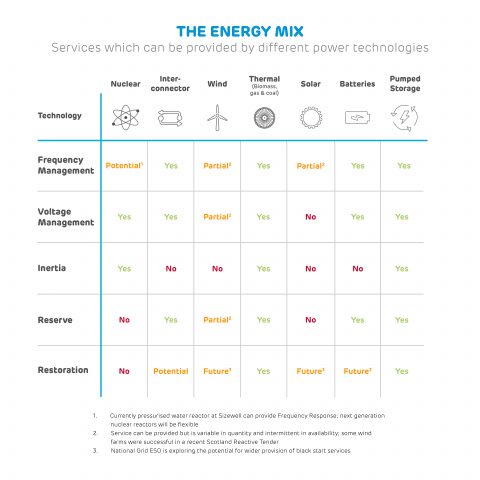

When the national grid was first established in the 1920s, it was designed with coal and big spinning turbines in mind. It meant that just about every megawatt coming onto the system was generated by thermal power plants. As a result, the mechanisms keeping the entire system stable – from the way frequency and voltage is managed to how to start up the country after a mass black out – relied on the same technology. These ‘ancillary services’ – those that stabilise the system – are crucial to maintaining a balanced electricity system.

“Ancillary services are needed to make sure demand is met by generation, and that generation gets from one place to the next with no interruptions,” explains Ian Foy, Head of Ancillary Services at Drax. “Because what’s important is that all demand must be met instantaneously.”

In today’s power system, however, weather dependent technology like offshore wind and home solar panels are increasingly making up the country’s electricity generation. Their intermittency or variability is, in turn, impacting both the stability of the grid and how ancillary services are provided.

Running a large power system with as much as 85% intermittent generation – for example on a very windy, clear, sunny day – is thought to be achievable. It isn’t a scenario anticipated for the large island of Great Britain. But to deal with the fast-pace of change on its power system which recently managed to briefly achieve 47% wind in its fuel mix, there is a need to develop new techniques, technologies and ways of working to change how the country’s grid is balanced.

One of the technologies that’s expected to provide an increasing amount of balancing services is grid-scale batteries. One stabilisation function offered by batteries (and other electricity storage options) is to provide reserve at times when demand peaks or troughs. This matches electricity demand and generation.

Combined with their ability to respond quickly to changes in frequency, batteries can be a significant source of frequency response.

Batteries can also absorb and generate reactive power, which can then be deployed to push voltage up or down when it starts to creep too far from the 400kV or 275kV target (depending on the powerlines the electricity is travelling along) needed to safely move electricity around the grid.

The challenge with batteries is that the quantity of megawatt hours (MWh) required to compensate for intermittency is very large. The difference between the peak and trough on any day may be more than 20 GW for several hours (see for yourself at Electric Insights).

The significant price reductions in battery storage apply to technologies with short duration (or low volume MWhs). These are the technologies which have been developed at scale recently but will probably struggle to make up in any large quantity any shortfalls in generation resulting from prolonged periods of low intermittent generation.

A challenge currently being addressed relates to maintenance of battery state of charge. This is a consequence of battery storage having a cycle efficiency of less than 100%. This means that losses from continuous charging and recharging will have to be replenished from the available generation to avoid batteries going empty and being unavailable for grid services.

Rather than relying on batteries to provide ancillary services to support intermittent generation, technical advancements are allowing the wind and solar facilities – which are generating more and more of the country’s electricity – to do so themselves.

The traditional photovoltaic (PV) inverters found on solar arrays were initially designed to push out as much active, or real, power as possible. However, new smart PV inverters are capable of providing or absorbing reactive power when it is needed to help control voltage, as well as continuing to provide active power.

The major advantage of smart inverters is the limited equipment update required to existing solar farms to allow them to offer reactive power control. The challenge here is that PV is embedded in distribution systems and therefore reactive services they provide may not cure all the problems on the transmission system.

Similarly, existing wind installations have traditionally focused on getting the greatest amount of megawatts from the available resources, but with fewer thermal power stations on the grid, ways of balancing the system with wind turbines are also being developed.

Inertia is the force that comes from heavy spinning generators and acts as a damper on the system to limit the rate of change of frequency fluctuations. While wind turbines have massive rotating equipment, they are not connected to the grid in a way that they automatically provide inertia, however, research is exploring what’s known as ‘inertial response emulation’ that may allow wind turbines to offer faster frequency response.

This works through an algorithm that measures grid frequency and controls the power output of a wind turbine or whole farm to compensate for frequency deviations or quickly provide increases or decreases in power on the system. Inertial response emulation cannot be a complete substitute for inertia but can reduce the minimum required inertia on the system.

Even in a future where the majority of the country’s electricity comes from renewable sources, thermal generators may still be able to provide benefits to the system by running in ‘synchronous compensation’ mode i.e. producing or consuming reactive power without real power.

However, what is vitally important for the future of balancing services in Great Britain is a healthy, transparent and investable market for generators, demand side response and storage, whether connected on the transmission or distribution networks.

One of the primary needs of balancing service providers is greater transparency into how National Grid procures and pays for services. Currently, National Grid does not pay for inertia. With it becoming more important to grid stability, incentive is needed to encourage generators with the capability to provide it. Those technologies that can’t provide inertia, could be encouraged to research and develop ways they could do so in the future.

Standardising the services needed will help ensure providers deliver balancing products to the same level needed to support the grid. It would also benefit from fixed requirements and timings for such services. Bundling related products, such as reserve and frequency control, and active power and voltage management, will also offer operational and cost efficiencies to the providers.

Driving investment in balancing services for the future, ultimately, requires the availability of longer-term contracts to offer financial certainty for the providers and their investors.

Click to view larger graphic.

For the challenges of decarbonisation to be met in a socially responsible way, Great Britain’s power system must be operated at as low a cost as possible to consumers.

With new technologies, almost anything could be possible. But operating them has to be affordable. In many cases, it may take time for costs of long duration batteries to come down – as it has with the most recent offshore wind projects to take Contracts for Difference (CfDs) and Drax’s Unit 4 coal-to-biomass conversion under the Renewables Obligation (RO) scheme.

Thermal power technologies such as gas that has proven capabilities in ancillary services markets can at least be used in a transitional period over the coming decades until a low carbon solution is developed.

Biomass will continue to be an important source of flexible power. This summer, at Drax, biomass units are helping to balance the system. It is the only low carbon option which can displace the services provided by coal or gas entirely.

In the past the race to decarbonisation was largely based around building as great a renewable capacity as possible. This approach has succeeded in significantly scaling up carbon-free electricity’s role on Great Britain’s electricity network. However, for the grid to remain stable in the wake of this influx, all parties must adapt to provide the balancing services needed.

This story is part of a series on the lesser-known electricity markets within the areas of balancing services, system support services and ancillary services. Read more about black start, system inertia, frequency response, reactive power and reserve power. View a summary at The great balancing act: what it takes to keep the power grid stable and find out what lies ahead by reading Maintaining electricity grid stability during rapid decarbonisation.

For more than 50 years Great Britain has been electrically connected to Europe. The first under-sea interconnector between British shores and the continent was installed in 1961 and could transmit 160 megawatts (MW) of power. Today there is 4 gigawatts (GW) in interconnector capacity between Great Britain, France, Ireland and the Netherlands – and there’s more on the way.

By the mid-2020s some estimates suggest interconnector capacity will reach 18 GW thanks to new connections with Germany, Denmark and Norway. The government expects imports to account for 22% of electricity supply by 2025, up from 6% in 2017.

This increased connectivity is often held up as a means of securing electricity supply and while this is largely true, it doesn’t tell the full story.

In fact, this plan could risk creating a dependency on imported electricity at a time when flexibility and diversity of power sources are key to meeting demand in an increasingly decentralised, decarbonising system.

Great Britain needs to be connected and have a close relationship with its European neighbours, but this should not come at the expense of its power supply, power price or ongoing decarbonisation efforts. Yet these are all at risk with too great a reliance on interconnection.

To secure a long term, stable power system tomorrow, these issues need to be addressed today.

At their simplest, interconnectors are good for the power system. They connect the relatively small British Isles to a significant network of electricity generators and consumers. This is good for both helping secure supply and for broadening the market for domestic power, but the system in which interconnectors operate isn’t working.

Since 2015 interconnectors have had the right to bid against domestic generators in the government’s capacity market auctions.

The government uses these auctions to award contracts to generators that can provide electricity to the grid through existing or proposed facilities. The original intention was also to allow foreign generators to participate. As an interim step, the transmission equipment used to supply foreign generators’ power into the GB market – interconnectors – have been allowed to take part. In practice, interconnectors end up with an economic advantage over other electricity producers.

Firstly, interconnectors are not required to pay to use the national transmission system like domestic generators are. This charge is paid to National Grid to cover the cost of installation and maintenance of the substations, pylons, poles and cables that make up the transmission network. Plus the cost of system support services keeping the grid stable. Interconnectors are exempt from paying these despite the fact imported electricity must be transported and balanced within England, Scotland and Wales in the same way as domestic electricity.

Secondly, interconnectors don’t pay carbon tax in the GB energy market. The Carbon Price Floor is one of the cornerstones of Great Britain’s decarbonisation efforts and has enabled the country’s electricity system to become the seventh least carbon-intense of the world’s most power intensive systems in 2016, up from 20th in 2012.

Interconnectors themselves do not emit carbon dioxide (CO2) in Great Britain, but this does not mean they are emission-free. France’s baseload electricity comes largely from its low-carbon nuclear fleet, but the Netherlands and Ireland are still largely dependent on fossil fuels for power. Because the European grid is so interconnected even countries which don’t yet have a direct link to Great Britain, such as Germany with its high carbon lignite power stations, also contribute to the European grid’s supply. The Neuconnect link is planned to connect Germany and GB in the late 2020s.

Not being subject to the UK’s carbon tax – only to the European Union’s Emissions Trading System (EU ETS) which puts a much lower price on CO2 – imported power can be offered cheaper than domestic, lower-carbon power. This not only puts Great Britain at risk of importing higher carbon electricity in some cases, but also exporting carbon emissions to our neighbours when their power price is higher to that in the GB market..

This prevents domestic generators from winning contracts to add capacity or develop new projects that would secure a longer-term, stable future for Great Britain. In fact, introducing more interconnectivity could in some cases end up leading to supply shortages, be they natural or market induced.

The contracts awarded to interconnectors in the capacity market auctions treat purchased electricity as guaranteed. But, any power station can break down – any intermittent renewable can stop generating at short notice. Supply from neighbouring countries is just the same.

Research by Aurora found that historically, interconnectors have often delivered less power than the system operator assumed they would and on occasion exported power at times of peak demand. This happened recently during the Beast of the East, when low temperatures across the continent drove electricity demand soaring.

This European-wide cold spell meant Ireland and France (which has a largely electrified heating system) experienced huge electricity demand spikes, driving power prices up.

As a result, for much of the time between 27 and 28 February Great Britain exported electricity to France to capitalise on its high prices. This not only led to more fossil fuels being burned domestically, but it meant less power was available domestically at a time when our own demand was exceptionally high. Even when the interconnectors do flow in our direction they cannot provide crucial grid services like inertia so our large thermal power stations are often still needed.

It is difficult to say for certain how interconnectors will function during times of high demand in the future due to a lack of long-term data, but that which we do know and have seen suggests they don’t always play to the country’s best interests.

There is still an important role for interconnectors on the Great Britain grid, but to deliver genuine value the system needs to be fairer so they don’t skew the market.

Interconnectors bring multiple benefits to our power system. They can help with security of supply by bringing in more power at times of systems stress, with the right system in place they can help reduce the need to rely on domestic fossil fuels and enable more renewable installation, and if electricity is being generated cheaper abroad, they can also create opportunities to reduce costs for consumers.

However, the correct framework must be put in place for interconnectors to bring such benefits while allowing for domestic projects that can help secure the country’s electricity supply.

As a start, interconnectors should be reclassified – known as de-rating – to compete with technologies on an equal footing.

Drax’s proposed OCGT plants, which can very quickly start up and provide the grid with the power and balancing services it needs, before switching off again, could offer a more reliable route to grid stability than such overwhelming dependence on interconnectors will. In addition, the coal-to-gas and battery plans at Drax Power Station, would prove to be a highly flexible national asset.

New gas and interconnectors should be able to compete fairly with one another. Policymakers should facilitate a system that allows competing technologies to exist in a cost beneficial way. Both interconnectors and domestic thermal power generators can play their part in creating stability, transitioning towards a decarbonised economy and fitting within the UK’s industrial strategy.

In 1961, when the first interconnector was switched on it marked a new age of continental co-operation. Five decades on we should not forget this goal. In an ever more complex grid, what we need is different technologies, systems and countries working together to achieve a flexible, stable and cleaner power system for everyone.