Click to view/download the report PDF.

Drax Power Station is currently exploring the option of adding carbon capture and storage equipment to its biomass-fired generating units. The resulting plant could produce at least 8 million tonnes (Mt) of negative CO2 emissions each year, as well as generating renewable electricity. Drax is planning to make a final investment decision (FID) on its bioenergy with carbon capture and storage (‘BECCS in power’1) investment in Q1 2024, with the first BECCS unit to be operating by 2027.

The potential of BECCS as part of the path to Net Zero has been widely recognised.

- BECCS in power is an important part of all of the Climate Change Committee (CCC)’s Net Zero scenarios, contributing to negative emissions of between 16- 39Mt CO2e per year by 20502. Investment needs to occur early: by 2035, the CCC sees a role for 3-4GW of BECCS, as part of a mix of low carbon generation3.

- The Government’s Energy White Paper commits, by 2022, to establishing the role which BECCS can play in reducing carbon emissions across the economy and setting out how the technology could be deployed. The Government has also committed to invest up to £1 billion to support the establishment of carbon capture, usage and storage (CCUS) in four industrial clusters4.

- National Grid’s 2020 Future Energy Scenarios (FES) indicate that it is not possible to achieve Net Zero without BECCS5.

However, at present, a business model6 which could enable this investment is not in place. A business model is required because a number of barriers and market failures otherwise make economic investment impossible.

- There is no market for negative emissions. There is currently no source of remuneration for the value delivered by negative emissions, and therefore no return for the investment needed to achieve them.

- Positive spillovers are not remunerated. Positive spillovers that would be delivered by a first-of-a-kind BECCS power plant, but which are not remunerated include:

- providing an anchor load for carbon dioxide (CO2) transport and storage (T&S) infrastructure that can be used by subsequent CCS projects;

- delivering learning that will help lower the costs of subsequent BECCS power plants; and

- delivering learning and shared skills that can be used across a range of CCS projects, including hydrogen production with CCS.

- BECCS relies on the presence of CO2 transport and storage infrastructure. Where this infrastructure doesn’t already exist, or where the availability or costs are highly uncertain, this presents a significant risk to investors in BECCS in power.

CCUS incubation area, Drax Power Station; click image to view/download

Frontier Economics has been commissioned by Drax to develop and evaluate business model options for BECCS in power that could overcome these barriers, and help deliver timely investment in BECCS.

Business model options

We started with a long list of business model options. After eliminating options that are unsuitable for BECCS in power, we considered the following three options in detail.

- Power Contract for Difference (CfD): the strike price of the CfD would be set to include remuneration for negative emissions, low carbon power and for learnings and spillover benefits.

- Carbon payment: a contractual carbon payment would provide a fixed payment per tonne of negative emissions. The payment level would be set to include remuneration for negative emissions, low carbon power and for learnings and spillovers.

- Carbon payment + power CfD: this option combines the two options above. The carbon payment would provide remuneration for negative emissions and learnings and spillovers while the power CfD would support power market revenues for the plant’s renewable power output.

We first considered if committing to any of these business model options for BECCS in power now might restrict future policy options for a broader GGR support scheme. We assessed whether these options could, over time, be transitioned into a broader GGR support scheme (i.e. one not just focused on BECCS in power), and concluded that this would be possible for all of them.

We then considered how these business model options could be funded, and whether the choice of a business model option is linked to a particular source of funds (for example, power CfDs are currently funded by a levy paid by electricity suppliers to the Low Carbon Contracts Company [LCCC]). We concluded that business models do not need to be attached to specific funding sources; all of the options can be designed to fit with numerous different funding options, so the two decisions can be made independently. This means that the business model options can be considered on their own terms, with thinking about funding sources being progressed in parallel.

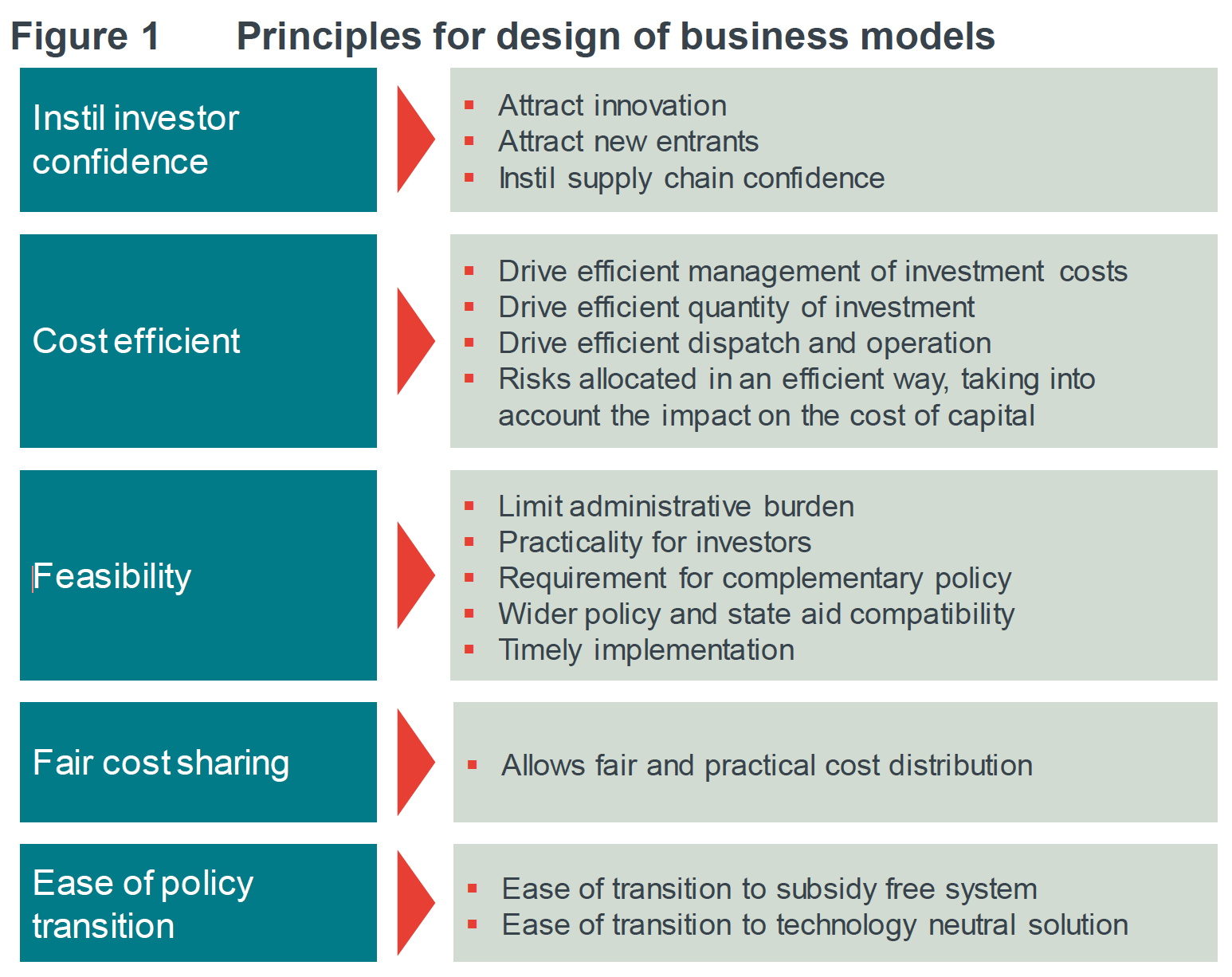

We then evaluated the three business model options against a set of criteria developed from principles set out in the BEIS consultation on business models for CCS, summarised in the figure below.

Figure 1: Principles for design of business models

| Instil investor confidence | ▪ Attract innovation ▪ Attract new entrants ▪ Instil supply chain confidence |

| Cost efficiency | ▪ Drive efficient management of investment costs ▪ Drive efficient quantity of investment ▪ Drive efficient dispatch and operation ▪ Risks allocated in an efficient way, taking into account the impact on the cost of capital |

| Feasibility | ▪ Limit administrative burden ▪ Practicality for investors ▪ Requirement for complementary policy ▪ Wider policy and state aid compatibility ▪ Timely implementation |

| Fair cost sharing | ▪ Allows fair and practical cost distribution |

| Ease of policy transition | ▪ Ease of transition to subsidy free system ▪ Ease of transition to technology neutral solution |

Source: Frontier Economics. Click to view/download graphic.

All three business model options performed well across most criteria. However, our evaluation highlighted some key trade-offs to consider when choosing a business model:

- investor confidence: the power CfD and the two-part model with a CfD performed better than the carbon payment on this measure, as they shield investors from wholesale power market fluctuations;

- feasibility: the power CfD performed best on this measure. Because it is already established in existing legislation and is well understood, it will be quick to implement. Introducing a mechanism to provide carbon payments may require new legislation. However, this will be needed in any case to support other CCUS technologies7, and could be introduced in time before projects come online; and

- potential to become technology neutral and subsidy free: all three options could transition to a mid-term regime which could be technology neutral. However, the stand-alone power CfD performed least well as it does not deliver any learnings around remunerating negative emissions.

Overall, the two-part model performed well across the criteria and would offer a clear path to a technology neutral and subsidy free world, delivering learnings that will be relevant for other GGRs as well.

Conclusions

The UK’s Net Zero target will be challenging to achieve, and will require investment in negative emissions technologies to offset residual emissions from hard-to-abate sectors, as highlighted by the CCC8. BECCS in power is a particularly important part of this picture, and represents a cost-effective means of delivering the scale of negative emissions needed. Early investment in BECCS is also important in insuring against the risk and cost of ”back ending” significant abatement effort.

However, market failures, most notably the lack of a market for negative emissions, lack of remuneration for positive spillovers and learnings, and reliance on availability of T&S infrastructure, mean that without policy intervention, the required level of BECCS in power is unlikely to be delivered in time to contribute to Net Zero.

There are a number of business options available in the near term to overcome these barriers. In our view, a two-part model combining a power CfD and a carbon payment is preferable.

This measure:

- addresses identified market failures;

- can be implemented relatively easily and in time to capture benefits of early BECCS in power investment; and

- can be structured to ensure an efficient outcome for customers (including with reference to investors’ likely cost of capital) and in a way that allocates risks appropriately.

View/download the full report (PDF).

1: Biomass can be combusted to generate energy (typically in the form of power, but this could also be in the form of heat or liquid fuel), or gasified to produce hydrogen. The resulting emissions can then be captured and stored using CCS technology. The focus of this report is on biomass combustion to generate power, with CCS, which we refer to as ‘BECCS in power’. We refer to biomass gasification with CCS as ‘BECCS for hydrogen’.

2: CCC (2020) , The Sixth Carbon Budget, Greenhouse Gas Removals, https://www.theccc.org.uk/wp-content/uploads/2020/12/Sector-summary-GHG-removals.pdf The CCC’s 2019 Net Zero report also saw a role for BECCS, with 51Mt of emissions removals included in the Further Ambition scenario by 2050. CCC (2019), Net Zero: The UK’s Contribution to Stopping Global Warming. https://www.theccc.org.uk/publication/net-zero-the-uks-contribution-to-stopping-global-warming/

3: CCC (2020), Policies for the Sixth Carbon Budget, https://www.theccc.org.uk/wp-content/uploads/2020/12/Policies-for-the-Sixth-Carbon-Budget-and-Net-Zero.pdf

4: BEIS (2020), Powering our Net Zero Future, https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/945899/201216_BEIS_EWP_Command_Paper_Accessible.pdf

5: National Grid (2020), Future Energy Scenarios 2020, https://www.nationalgrideso.com/future-energy/future-energy-scenarios/fes-2020-documents

6: In this report, we use “business model” to describe Government market-based incentives for investment and operation. This is in line with the use of this term by BEIS, for example in BEIS (2019), Business Models For Carbon Capture, Usage And Storage, https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/819648/ccus-business-models-consultation.pdf

7: BEIS (2020), CCUS: An update on business models for Carbon Capture, Usage and Storage https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/946561/ccus-business-models-commercial-update.pdf

8: CCC (2020) , The Sixth Carbon Budget, Greenhouse Gas Removals, https://www.theccc.org.uk/wp-content/uploads/2020/12/Sector-summary-GHG-removals.pdf

{kind=link}